Succession Planning in the Netherlands: A Framework for Dutch Business Owners and Family Companies

A large cohort of Dutch owners is reaching the succession window with a company still structurally bound to them personally - the founder's customer relationships, the founder's pricing instincts, the founder's holding architecture, sitting where they have always sat. Succession planning in the Netherlands now intersects with three pressures that have shifted at the same time: a multi-year recalibration of the bedrijfsopvolgingsregeling, an active but more disciplined Dutch mid-market M&A environment, and the DGA structure, which entangles personal and corporate finance in ways buyers price into a discount. This article sets out an operating framework for Dutch business owners and family companies preparing for ownership transition in the Netherlands — and explains why the harder problems are operational rather than fiscal.

Why succession planning in the Netherlands has become structurally harder

The Dutch economy runs on family ownership. CBS, the national statistical authority, has recorded close to 300,000 family businesses, employing several million people and accounting for a meaningful share of national value added. A material portion of that ownership base is now over fifty-five. The OECD has documented the same demographic pattern across advanced European economies: over the coming decade, the volume of transfers will not be the constraint. The readiness of the underlying companies will.

The harder problem is structural. The directeur-grootaandeelhouder (DGA) model places the owner inside the company in a way that does not exist in publicly held businesses. Salary, dividend, retained earnings, holding-company loans and pension provision are interlocked. Since the abolition of pension accrual in own management (pensioen in eigen beheer) in 2017, many DGAs still carry legacy pension liabilities on the balance sheet that complicate any exit calculation: a buyer will treat them as debt-like, a successor will inherit them, and a tax adviser will want them settled before either path proceeds. The Dutch family business reaching the succession window is rarely transfer-ready in its current legal and financial form. That is not a tax problem. It is an operating-model problem with tax consequences.

Several Dutch features compound the difficulty. The typical mid-market structure is a stack of holding BVs accumulated over years, often a personal holding, a management BV and one or two operating BVs, none of them designed for a transaction. The accountant who has served the family for two decades may be right for the annual statutory accounts and wrong for a transaction-grade quality-of-earnings exercise. The fiscalist owns the BOR timing logic and sometimes overrides the operational case. Banking is relationship-led: the local manager at Rabobank, ABN AMRO or ING has known the DGA for years, and that manager's view on continuity shapes the MBO financing and acquisition leverage realistically available. Every transfer of BV shares passes through a notary, who is a procedural gate rather than a strategic actor.

The bedrijfsopvolgingsregeling reform and what it actually changes

The bedrijfsopvolgingsregeling in the Netherlands has not been abolished. It is being recalibrated across a multi-year sequence. Measures took effect on 1 January 2025 and 1 January 2026, with further evaluation scheduled later in the decade. Owners who recall the BOR from a decade ago should expect a narrower regime.

The substantive changes now in force include the reduction of the continuation requirement (voortzettingseis) from five to three years for transfers from 1 January 2025, a tighter statutory definition of preferred shares from 1 January 2026 that affects family transfers using letter-share constructions, and an extended holding period for testators who have passed the AOW age plus three years. A separate set of restrictions announced in earlier Belastingplan packages was not enacted, owing to state aid concerns identified during legislative review. The current position should be verified against the Belastingdienst and the Ondernemersplein guidance at the point of any specific transaction.

Two conclusions follow. First, the bedrijfsopvolgingsregeling in the Netherlands now requires earlier, more deliberate fiscal structuring: staged transfers, hybrid share classes and gift-and-loan combinations that worked five years ago no longer transpose without review. Second, less obviously, the BOR cannot rescue an unprepared transfer. A tax-relieved transmission of a personally dependent business is still a transmission of a personally dependent business. The fiscal saving is real; the operational risk it leaves behind is real as well.

The four succession routes and how they behave

Each route looks workable in a pitch. Each fails in a different operational place.

Route | Typical fit | Tax treatment headline | Financing structure | Governance prerequisite | Where it usually fails |

|---|---|---|---|---|---|

Family continuation | Capable, willing next-generation successor | BOR and DSR — narrower from 2025 and 2026 | Gift-and-loan combination | Family governance; formalised role separation | Successor capability or appetite over-estimated |

Management buyout | Strong internal team; mid-market valuation | Standard corporate and personal income tax | Vendor loan, bank debt, occasionally mid-market private credit | Management operating independently of the owner | Price expectation gap; financing stretch |

Strategic sale | Defensible niche; clean reporting | Standard M&A tax treatment | Buyer financed | Documented commercial model; reduced concentration | Personally dependent revenue; weak reporting |

Private equity | Scalable platform; relevant EBITDA band | Standard M&A tax treatment | LBO structure | Audit-grade MIS; non-owner-led management | Quality of earnings; key-person risk |

Family continuation rests on operational capability, not tax structuring. Dutch family business succession assisted by BOR but unsupported by successor readiness is value destruction with a tax discount attached. The honest pre-test is whether the prospective successor has run a meaningful operating mandate inside the business, with budget authority and direct accountability, before equity moves.

The management buyout route has to clear three hurdles: a vendor willing to defer, a lender willing to underwrite, and a price the team can service. De Nederlandsche Bank has documented the gradual normalisation of the Dutch financing environment, reopening acquisition leverage in the mid-market. Even so, MBOs more often fail on price expectation than on management capability. The DGA's headline valuation, anchored on past EBITDA and personal effort, rarely matches what an internal team can finance from operating cash flow.

Selling a business in the Netherlands to a strategic acquirer is most active in fragmented industries, including professional services, testing and inspection, specialist manufacturing and health-adjacent services. Buyers expect audit-grade reporting, a management team that operates without the owner, and customer concentration below a defensible threshold. The discount points show up at specific stages of a process. Quality-of-earnings adjustments strip out owner-driven margin and one-off items. Working capital normalisation consumes the last weeks of negotiation, because the company has never tracked a defensible target. Earn-outs attach themselves to revenue retention with customers the buyer suspects are personality-led. Management retention clauses, indemnity baskets and warranty caps in the SPA all reflect what diligence has concluded about documentation and key-person risk. Our M&A advisory and post-merger integration practice sets out how these workstreams sequence.

Private equity reads a Dutch family business through three lenses. The first is whether the company qualifies as a platform or only as an add-on. A personally entangled business rarely justifies platform pricing, because the management team a sponsor would build the strategy around does not yet exist. The second is the quality of EBITDA once the owner's compensation is normalised, related-party transactions are unwound and customer concentration is exposed in the quality-of-earnings work. The third is reporting cadence. Post-LBO debt service requires a monthly board pack and a covenant compliance pack the company has often never produced, and bridging that gap inside a hundred-day plan is harder than it looks. Owners who present a clean carve-out narrative attract multiple expansion. Owners who present a personally entangled holding accept a structural discount as the cost of selling at all.

Why most succession failures are operational, not fiscal

Most failures of succession planning in the Netherlands cluster in five places, none of them a tax issue. Undocumented commercial knowledge sits in the owner's head. The supplier rebate agreement that lives in a WhatsApp thread. The pricing exception for the third-largest customer, applied manually in the ERP each month because the rule was never coded. The margin floor the founder overrides for strategic accounts. The treasury sweep that happens because the controller knows what the owner prefers, not because a policy exists.

Customer relationships exist with the owner personally rather than with the firm, and diligence finds this within an afternoon of interviews. Authority has never been delegated in documented form, because the owner has always been available. The second-line management layer is thinner than the organisation chart suggests, often because family trust has obscured the underperformance of a relative in an operating role. Decision rights have never been made explicit, because the owner has been the decision.

The commercial consequence is paid at three points. The valuation a buyer is willing to support contracts, because every personal dependency is a risk premium. The leverage the seller carries into negotiation evaporates, because the alternative routes are weaker than they appeared on paper. The acquirer's confidence in the first ninety days after closing is fragile, which feeds into earn-out structures, escrow ratios and management retention terms, each moving value away from the seller.

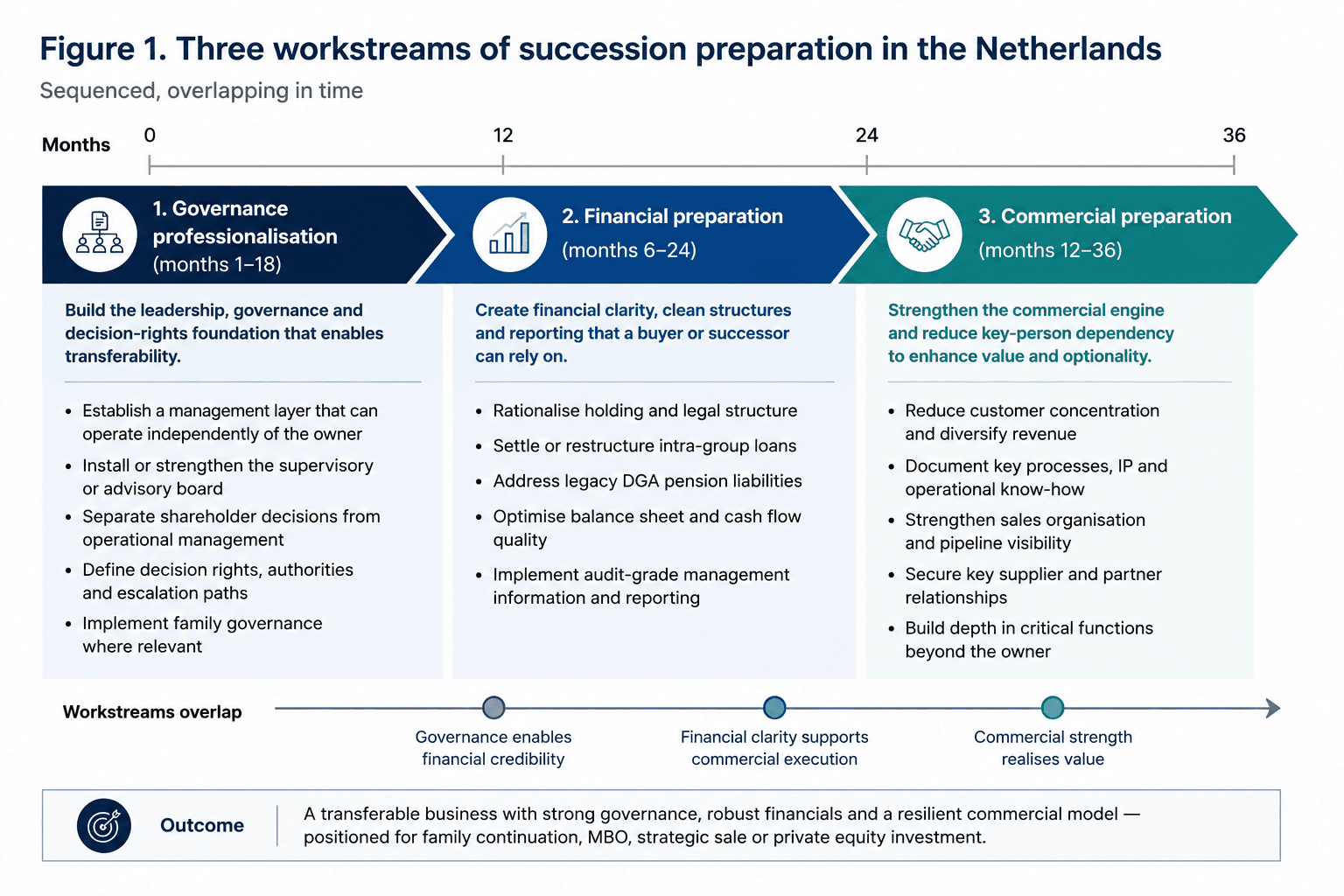

The remedy is three workstreams, sequenced.

Governance professionalisation. A management layer that can run the business without the owner, a working supervisory or advisory board, and an explicit separation of shareholder decisions from operating decisions. Without this, neither family continuation nor selling a business in the Netherlands is executable. Our work on board advisory and governance support and on business transformation and operating model redesign sets out what governance professionalisation before a Dutch business sale typically involves.

Financial preparation. The holding structure built up over years rarely survives diligence in its current form. Intra-group loans, the legacy pension liability, real estate sitting inside the operating company, and reporting that no third party can rely on, each a discount point. The aim is numbers a buyer can underwrite without rebuilding them.

Commercial preparation. Customer concentration ratios, codified key supplier relationships, a sales organisation that is not personality-led, and an explicit transfer of the owner's tacit knowledge to named individuals. The hardest workstream, started last and finished last.

Sequencing, timeline and the owner's own transition

The European Commission's work on SME transfer has been consistent across editions: preparation that meaningfully changes the outcome takes years, not quarters. The workable window for preparing a Dutch business for succession or sale is twenty-four to sixty months. Compressed processes - forced by a health event, a partnership breakdown, or an unsolicited offer the owner accepts — almost always close at a discount, because the operational dependencies above cannot be unwound in twelve months.

Any ownership transition in the Netherlands also carries a personal dimension framed in psychological terms when it is in fact commercial. DGA succession and exit planning in the Netherlands frequently stalls because owners renegotiate their own future role, staying on as managing director, then as chair, then as adviser, then leaving. Each step introduces execution risk that buyers price in. Where the owner has decided to step out but the management layer is not yet ready, interim management and operational leadership can bridge the gap.

The same logic applies to Dutch family business succession. Transferring legal ownership is the easy part. Transferring operational authority, supplier credibility, customer trust and the right to overrule a senior manager all take time, and each must be visible inside the organisation before the equity moves.

What this means for Dutch owners

Succession planning in the Netherlands is now an operating model exercise with fiscal and transactional consequences, not the reverse. Owners who treat it as a deal to run later, or a tax structure to optimise closer to retirement, find at diligence that the discount has already been priced in by every operational dependency they have not addressed. Done properly, succession planning for Dutch business owners and family companies converts a personally dependent business into a transferable one, which protects valuation, optionality and timing when the moment arrives.

For owners working through these decisions, our team supports succession sequencing across governance, transaction structuring and post-merger integration in the Netherlands.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.