Textile and Agriculture Processing Investment in Uzbekistan

Uzbekistan's processing opportunity is not defined by the volume of cotton, fruit, vegetables or dairy the country produces. It is defined by the ability to convert those inputs into reliable, certified and export-ready processed products, and the distance between the two defines where investment value is created or destroyed.

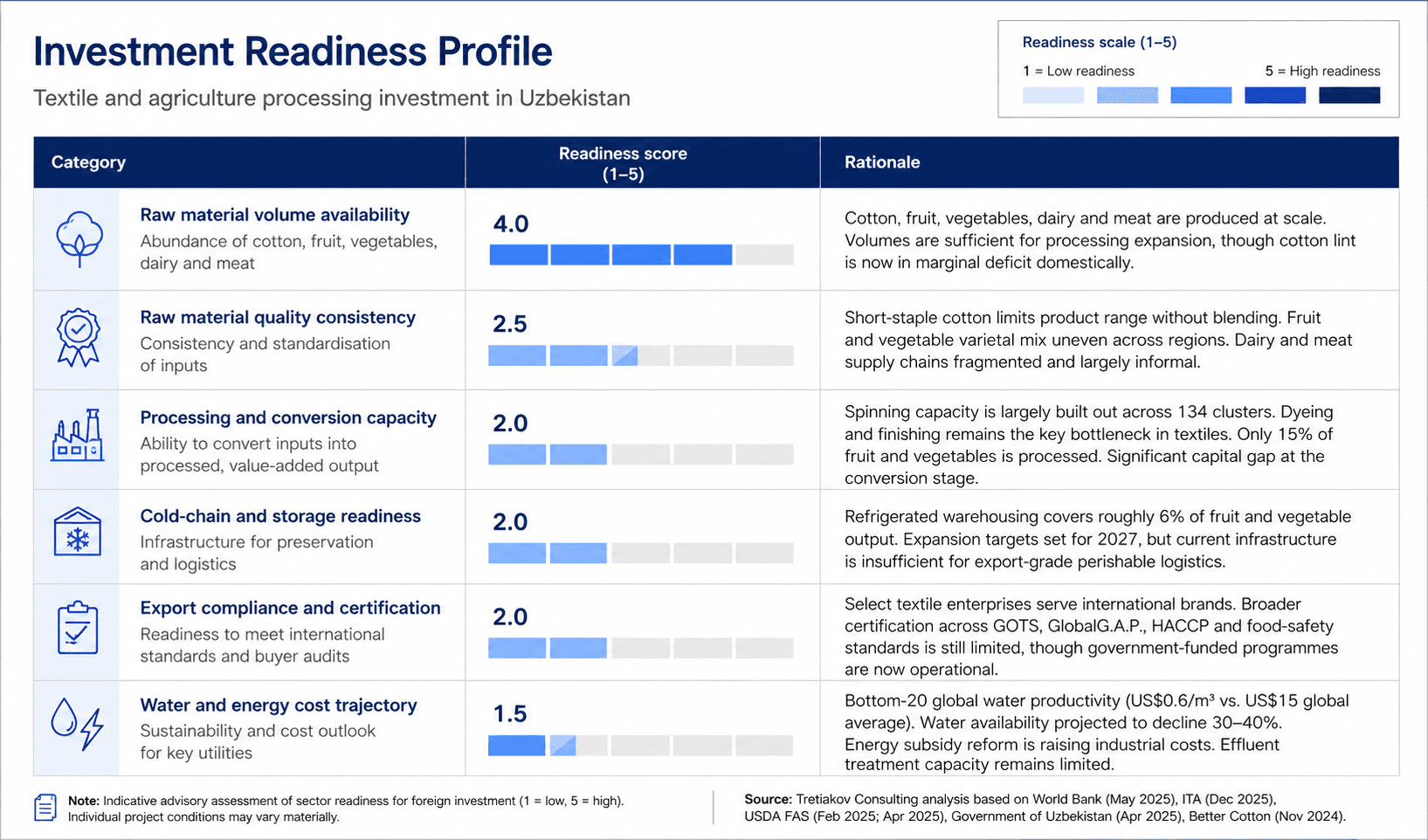

The volumes are substantial. Yet only 15% of the roughly 20 million tonnes of fruits and vegetables grown each year is processed, while 30% is lost due to insufficient storage and handling capacity, and only 16% of meat and milk enters a formal processing chain (ITA, December 2025). In textiles, domestic cotton lint consumption has been approaching and in some forecasts exceeding domestic production as spinning capacity expands. This changes the textile investment case: cotton supply can no longer be treated as a static domestic advantage, but must be managed through procurement strategy, blending capability and working-capital planning.

This is the central paradox of textile and agriculture processing investment in Uzbekistan as raw material abundance is visible across every metric that matters, but the infrastructure, operating systems and certification pathways required to convert that abundance into exportable, margin-bearing processed products remain fundamentally undersized. The investment logic across both sectors is identical: raw material availability leads to processing conversion, which leads to value capture. The question for foreign investors is not whether supply exists, but whether the conversion step is investable at the project level, and where exactly along each chain the margin is captured or lost.

Why Raw Material Abundance Does Not Equal Investable Processing Capacity

Each of these headline figures carries a direct investment implication, and understanding the distinction separates a credible thesis from a location-based assumption.

The 15% fruit and vegetable processing rate means 85% of output either leaves the country unprocessed at commoditised margins or never reaches a buyer at all. This is simultaneously an opportunity and evidence that the conversion infrastructure does not yet exist at scale. The 30% post-harvest loss is margin leakage that a properly designed cold-chain and sorting operation can partially recover. More rapid growth in the horticulture sector is constrained by farmers' limited knowledge of modern farming practices, a lack of mechanisms to effectively link farmers to markets, bottlenecks in the value chain, and a significant investment gap estimated at over $1 billion (World Bank, April 2025). The 16% dairy and meat processing rate signals fragmented and largely informal upstream supply chains where the input-quality consistency that any processing operation depends upon is difficult to assure.

On the cotton side, the fibre base that once underpinned a raw-export economy is now balanced-to-deficit as the textile sector's installed spinning capacity continues to grow. Domestic consumption is projected to rise further, meaning procurement strategy, blending capability and import logistics have become as important to the textile investment case as factory equipment selection. For investors evaluating industrial investment and capital projects in Central Asia, these figures collectively describe a market where the constraint is not demand or raw-material volume but the conversion infrastructure and operating capability between input and export-ready output.

Scores reflect structural readiness for scalable, export-oriented processing investment. Individual projects may perform materially above or below the sector profile.

Where the Textile Value Chain Breaks

Uzbekistan's textile industry has scaled rapidly. Official 2025 reporting places textile exports at approximately $2.5 to $2.6 billion, with employment above 620,000 and further investment targeted for 2026 (Government of Uzbekistan, December 2025). Dozens of local enterprises produce garments for international brands including LC Waikiki, The North Face and Inditex under CMT and FOB arrangements (Government of Uzbekistan). These figures confirm momentum, but they do not show where the bottleneck sits or where margin is actually captured.

The textile chain decomposes into distinct stages: farming, ginning, spinning, weaving or knitting, dyeing and finishing, garment assembly, brand compliance and export logistics. Uzbekistan has built substantial spinning capacity across 134 cotton-textile clusters. Government plans for 2026 include creating additional capacity for 207,000 tonnes of synthetic and blended yarn, 397 million square metres of fabrics, 224 million units of garment and knitwear products, and critically, dyeing capacity for 108 million square metres of textiles (Government of Uzbekistan, December 2025). The fact that the government specifically targets dyeing capacity signals recognition that this mid-chain conversion step remains undersized relative to upstream supply.

The critical conversion point, where the chain moves from "cotton producer" to "export-grade textile supplier", is dyeing and finishing. This is where fabric acquires the colour, hand-feel, dimensional stability and chemical profile that international buyers specify. It requires process water for dyeing and washing, steam and heat for setting, chemical management systems for restricted substance compliance, effluent treatment for discharge licensing, colour consistency across production batches, and traceability documentation for buyer audits. Every one of these requirements intersects with Uzbekistan's most binding constraints: water scarcity, energy cost trajectory and institutional compliance capability.

The cotton quality profile compounds the finishing challenge. Uzbekistan primarily produces short-staple cotton due to limited mechanisation, which restricts the product range achievable without blending or importing longer-staple fibre. Converting a short-staple, hand-picked cotton base into fabric that passes EU or US buyer specification demands more from finishing and quality-assurance stages, not less. Challenges identified at the sector level include partial dependence on imported cotton fibre, high financial resource costs, rising logistics expenses on external markets, and a shortage of qualified personnel.

One development that signals the direction of the sector is the government's partnership with the Better Cotton Initiative. The Light Industry Agency will manage a new fund to reimburse the cost of farm and supply chain-level certification against Better Cotton standards (Better Cotton, November 2024). This represents institutional acknowledgement that certification is a barrier to market access, not a voluntary enhancement, and that the state needs to underwrite the cost of meeting international standards to make the textile industry in Uzbekistan competitive at the export level.

Foreign investors entering this sector should evaluate not whether spinning or garment capacity exists but whether the dyeing, finishing and compliance segment can operate at export quality under rising water and energy costs. Projects that solve this conversion step hold the defensible margin position.

Agriculture Processing: Three Investment Models, Three Risk Profiles

Uzbekistan's arid climate makes irrigation essential for agriculture, which contributes approximately 25% of national GDP and total employment (ITA, December 2025). In 2024, the country exported 2 million tonnes of fruits and vegetables, generating $1.5 billion in revenue. In January to November 2025, export volumes increased by 6.3% while revenue rose by 36.8%, suggesting that value per tonne shipped is rising as more product moves through at least basic processing and packaging before export (FreshPlaza, December 2025).

Presidential Resolution PP-136 issued in April 2025 set targets to increase fruit and vegetable processing capacity from 3,488 thousand tonnes in 2024 to 4,480 thousand tonnes in 2027, and expand refrigerated warehousing from 1,306 thousand tonnes to 1,930 thousand tonnes. The resolution also targets increasing the processing of milk to 32%, meat to 25%, and fruits and vegetables to 28% by 2026.

The investment opportunity in agriculture processing in Uzbekistan divides into three distinct models, each with a different capital profile, margin driver and risk structure.

Fresh produce: sorting, packing, cold chain, controlled-atmosphere storage, phytosanitary certification. The margin in this segment depends on loss reduction and logistics speed. The binding constraint is not the sorting or packing equipment but unbroken cold-chain reliability from farm gate to export border. When 30% of output is lost before reaching a buyer, the investment thesis is fundamentally about recovering margin that currently leaks through infrastructure gaps. Participating fruit and vegetable producers who adopted improved practices benefited from a 25 to 30% increase in crop yields and a 35% increase in gross sales (World Bank, April 2025), confirming that where conversion infrastructure exists, the economics are real.

Food processing: canning, juice, dried fruit, freezing, dairy, meat. The margin here depends on processing yield, input standardisation and plant utilisation rates. Dairy and meat processing at 16% penetration represents significant volume upside, but also fragmented and informal supply chains that make raw-material quality consistency difficult to achieve. Juice and dried-fruit operations can access export markets more readily if they meet EU residue limits and traceability requirements, but yields depend on varietal selection, harvest timing and grading discipline that remain uneven across growing regions.

High-value export processing: organic certification, full traceability, EU residue compliance, branded packaging, buyer audit readiness. This is the highest-margin model and the most demanding to execute. It requires governance systems beyond the factory floor: traceability from farm to container, internal audit capability, document management that satisfies European retailer due diligence, and packaging that meets destination-market labelling regulations.

Companies considering market entry and business expansion into these segments will find that the government's capacity-expansion targets create a genuine policy tailwind, but that execution risk sits in cold-chain reliability, water access, certification timelines and workforce capability rather than in demand or raw-material supply.

Water, Cold Chain and Compliance as Feasibility Constraints

Water scarcity in Uzbekistan is not a background environmental concern. It is a binding constraint on processing investment in both textiles and food, and in practical terms, water determines whether a site is financeable, licensable and auditable by export buyers.

Uzbekistan ranks among the bottom 20 countries globally in water productivity, producing only $0.6 per cubic metre compared with a global average of $15. Water availability is projected to decrease 30 to 40% while irrigation demand increases by 25%, and agriculture already consumes nearly 90% of water withdrawals. The World Bank approved a $200 million concessional credit to support modernisation of irrigation and drainage infrastructure (World Bank, May 2025), but the investment required to bring water management to the level that processing industries need extends well beyond a single programme.

For textile finishing, water enters the investment model at every stage: process water for dyeing and washing, cooling water for energy systems, and effluent treatment for discharge compliance. For agriculture processing, water determines site selection, processing throughput, cleaning and sanitation compliance and the upstream quality of raw material supply for irrigated horticulture. Cold-chain infrastructure compounds the constraint, with refrigerated warehousing capacity currently covering roughly 6% of annual fruit and vegetable output.

Certification and compliance readiness is the third feasibility variable. GOTS, OEKO-TEX, Better Cotton, HACCP, ISO 22000, GlobalG.A.P. and EU residue limits are market-access requirements, not optional enhancements. Government plans include implementing programmes such as Better Work, BCI, FWF and Organic EU at 60 enterprises, while 15 companies will adopt international financial reporting standards (Government of Uzbekistan, December 2025). The decision to programme these certifications across dozens of enterprises at once reflects recognition that individual companies cannot easily reach audit-readiness alone.

Investors evaluating operational involvement and performance improvement in either sector should treat these three constraints not as items on a risk register but as first-order determinants of project viability.

What Changes the Economics of a Processing Project

The difference between a processing project that generates returns and one that consumes capital over several years without reaching sustainable margin comes down to a handful of operating variables that are routinely underestimated in feasibility studies.

Processing yield determines how much saleable output each tonne of input produces. In textiles, yield losses occur at dyeing and finishing through colour rejects, dimensional failures and chemical non-compliance. In food processing, yield depends on varietal quality, harvest timing, sorting accuracy and the speed of transfer from field to facility. A 5% improvement in processing yield in a mid-scale operation can shift the project from marginal to viable.

Plant utilisation is the second critical variable. Processing equipment in seasonal industries runs at full capacity for a limited number of months per year. The financial model must account for the months when the plant is underutilised or idle, and the fixed costs that continue to accrue during those periods. Projects that can extend the processing season through controlled-atmosphere storage, diversified input sourcing or multi-product capability have structurally stronger economics.

Input standardisation determines whether the processing line runs efficiently or spends time adjusting to variable raw material. Where upstream supply chains are informal and quality grading underdeveloped, as is the case across much of Uzbekistan's dairy, meat and horticulture supply base, the processing operation absorbs the cost of that variability through lower throughput, higher defect rates and increased waste.

Energy and water cost per unit of output is rising as subsidy reform progresses. A project modelled on today's energy tariffs without accounting for the trajectory of subsidy removal may show viable margins at commissioning but eroding margins within three to five years.

Certification timeline determines when export revenue begins. The period from project start to passing a buyer audit for GOTS, GlobalG.A.P. or HACCP can take 12 to 24 months, depending on the starting point and the complexity of the supply chain that needs to be documented and controlled. This delay must be capitalised.

Working capital cycle is sharply seasonal. Cotton harvest, fruit harvest and dairy production create peaks and troughs in input purchasing, processing activity and cash outflow, while export payment terms commonly run 60 to 90 days. In 2026, textile enterprises will be provided with $200 million in concessional loans to replenish working capital, and financial rehabilitation will be carried out for 138 companies (Government of Uzbekistan, December 2025). The fact that the government is deploying concessional lending specifically for working-capital replenishment illustrates how real this constraint is at the sector level.

The World Bank collaborated with local financial institutions to introduce a dedicated credit line for horticulture investments, enabling producers to access concessional financing for modern greenhouses, processing, cold storage and export facilities (World Bank, April 2025). These financing instruments improve the capital structure available to investors, but they do not substitute for the operating disciplines described above.

Where Investors Usually Miscalculate

Five assumptions consistently undermine processing investments in markets like Uzbekistan, and recognising them before commitment is significantly more valuable than discovering them during ramp-up.

They treat raw material proximity as supply security. Being located near cotton fields or orchards does not guarantee consistent input quality, reliable delivery volumes or prices that support the processing margin. This leads to overstated utilisation assumptions, understated procurement costs and unrealistic first-year margins. Supply-chain management, encompassing contracts, grading, logistics and payment terms, is an operational discipline that requires investment and management attention, not a geographic fact that can be assumed.

They underestimate water and energy economics. Equipment budgets are straightforward to model. Utility-cost trajectories under subsidy reform and water-scarcity pricing are not. A project that is viable at today's energy cost may not be viable at the cost implied by progressive subsidy removal. This leads to margin erosion that the original investment case did not anticipate and that cannot be corrected without fundamental changes to the operating model.

They budget for equipment but not for ramp-up losses. The first 12 to 18 months of any processing operation involve yield losses, elevated defect rates, workforce training costs and buyer-qualification cycles that consume cash without generating full-margin revenue. This leads to liquidity pressure at exactly the moment when the project needs operational stability to build buyer confidence and secure repeat orders.

They assume certification is paperwork rather than an operating system. GOTS, OEKO-TEX, GlobalG.A.P. and HACCP require management processes, record-keeping disciplines, internal audit capability, corrective-action routines and continuous compliance investment. This leads to delayed market access when the project discovers that a buyer audit requires six months of documented process control history, not a single inspection visit.

They underfund working capital for seasonality and export payment terms. This leads to liquidity stress at precisely the point where production volumes are highest and cash collection is furthest away. The government's deployment of $200 million in concessional working-capital lending for textile companies confirms that this is a system-wide constraint, not a project-specific oversight.

Investors working with advisors experienced in industrials and manufacturing sector strategy will recognise these patterns from processing investments across emerging markets and will structure due diligence around them rather than around headline capacity or raw-material volumes.

Investment Assessment Framework

The following table structures the due-diligence logic for textile and agriculture processing investment in Uzbekistan across the dimensions that determine whether a processing project captures or destroys value.

Assessment Dimension | Textile Chain | Agriculture Processing Chain | Decision Logic |

|---|---|---|---|

Demand channel and buyer economics | International brands sourcing CMT and FOB, with government targets pointing to further export expansion and route-to-market through Turkiye, Russia and the EU | Regional fresh produce buyers, EU and Gulf food processing channels, supermarket private-label and perishable logistics to Russia, Kazakhstan and Gulf states | Buyer specification determines every upstream requirement. Start from demand backward |

Raw material conversion | Short-staple, hand-picked cotton with lint now in deficit. Blending or import increasingly required | Over 20 million tonnes harvested but varietal mix and harvest timing affect yield. Dairy and meat supply chains fragmented | Availability does not equal usability. Conversion yield depends on input quality consistency |

Processing margin and yield | Margin concentrates in dyeing, finishing and compliance. Spinning and assembly are volume-dependent | Margin concentrates in processed, packaged, traceable product. Post-harvest loss represents recoverable margin | Projects that solve the conversion bottleneck capture margin. Those positioned upstream capture volume only |

Water, energy and cold-chain feasibility | Process water for finishing, energy for heat-setting, effluent treatment for compliance | Water for washing and sanitation, energy for refrigeration, cold-chain integrity from farm gate to border | Water at $0.6 per m³ productivity against $15 global average makes this a first-order variable |

Certification and audit pathway | GOTS, OEKO-TEX, Better Cotton, brand restricted substance lists, social audit standards | HACCP, ISO 22000, GlobalG.A.P., organic, EU residue limits, phytosanitary | Certification is market access. Timeline to readiness determines when revenue begins |

Working capital and seasonality | Cotton harvest seasonal. Buyer payment terms 60 to 90 days. Government deploying concessional lending for working capital | Harvest windows create acute seasonal demand. Cold storage extends but does not eliminate the peak | Structure must match the seasonal cash-flow profile |

Governance and operating cadence | Transformation office, KPI-driven production, brand audit readiness, defect-rate management | Traceability, batch management, recall capability, document control, food-safety training | Operating-model maturity determines whether capacity translates to reliable output |

What This Means for Foreign Investors

The investable opportunity in Uzbekistan is controlled conversion. Projects that secure water, standardise inputs, manage processing yield, pass buyer audits and finance seasonal working capital can capture the margin currently lost between raw material and export-ready product. Projects that treat processing as a simple equipment-and-location decision are likely to reproduce the bottlenecks that explain why large volumes remain unprocessed today.

Government policy is aligned with this direction. Presidential Resolution PP-136 targets substantial expansion of processing and cold-chain capacity by 2027. The World Bank is financing irrigation modernisation and horticulture investment credit lines. The Better Cotton certification fund addresses a specific barrier to textile export-market access. Concessional working-capital lending acknowledges the cash-flow reality of seasonal processing operations. These are real institutional commitments that create an enabling environment which did not exist five years ago.

But policy targets do not resolve the operating-model constraints that sit between raw material and final product. The strongest projects in cotton processing in Uzbekistan and across the broader agriculture sector will be those that solve conversion risk at specific, identifiable points along the chain. Understanding where value is created and destroyed, from enterprise modernisation in Uzbekistan through to export compliance, is the foundation of sound capital deployment across the region.

To discuss how Tretiakov Consulting supports foreign investors in structuring textile and agriculture processing investment in Uzbekistan, contact our advisory team.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.