Privatisation in Uzbekistan: How Foreign Investors Can Participate

Privatisation in Uzbekistan has entered its most consequential phase since the reform programme began in 2017. In April 2025, a presidential decree approved the annual privatisation programme with a combined target revenue of 10 trillion UZS from the sale of state shareholdings, real estate assets and land. In parallel, the government launched the $2 billion Uzbekistan National Investment Fund to bring major state enterprises to international capital markets, with a dual London and Tashkent IPO in May 2026 representing the first time an Uzbek state-backed entity has tapped global equity markets. For foreign investors, strategic buyers and corporate development teams, these developments create genuine access to assets that were previously unavailable to private capital. But the transaction reality is more complex than the headline programme suggests. How foreign investors can participate in privatisation in Uzbekistan depends on their ability to assess the quality of the asset, the reliability of available financial information, the sale process itself and the scale of post-acquisition transformation required to convert a former state enterprise into a commercially viable business.

Why Uzbekistan's Privatisation Programme Matters to Foreign Investors

The scope of the programme reflects the scale of the state's economic role. As of March 2025, there are 541 active state-owned enterprises with a state share of 20% or more, and the 10 largest contribute approximately 30% of total state budget revenues. The broader SOE footprint is more significant still: the World Bank's Country Economic Memorandum identifies over 2,000 centrally held SOEs with revenues equivalent to 32% of GDP, four out of five of which operate in sectors where private firms could compete more effectively. SOE reform in Uzbekistan is therefore not a marginal restructuring exercise but a fundamental rebalancing of the relationship between state and market across banking, telecommunications, chemicals, mining, energy, agriculture, manufacturing and transport.

The government is pursuing multiple transaction formats in parallel. Direct Uzbekistan state asset sales are conducted through competitive auctions managed by the Agency for Management of State Assets, which determines whether a sale proceeds via auction, public competition or negotiated process. Capital-market transactions are being channelled through UzNIF, managed by Franklin Templeton, which holds 13 strategic companies and is tasked with increasing their market value, restructuring their governance and attracting institutional investors. The first IPO valued the fund at approximately $1.95 billion, with cornerstone commitments of around $300 million from BlackRock, Franklin Resources and Redwheel.

For firms evaluating business and investment conditions in Uzbekistan, the opportunity is measurable. About 45% of SOEs had been privatised by end-2023, but the process slowed in 2024 as the restructuring of major state-owned banks required more preparation time. The government responded in April 2026 by announcing the privatisation of an additional 67 large enterprises, with the new UzSAMA Director stating a target to sell state property worth 35 trillion soums by year-end. Distinguishing between assets that are genuinely available, strategically attractive and transactionally ready from those that remain on official lists without realistic timelines is the first analytical step for any serious investor.

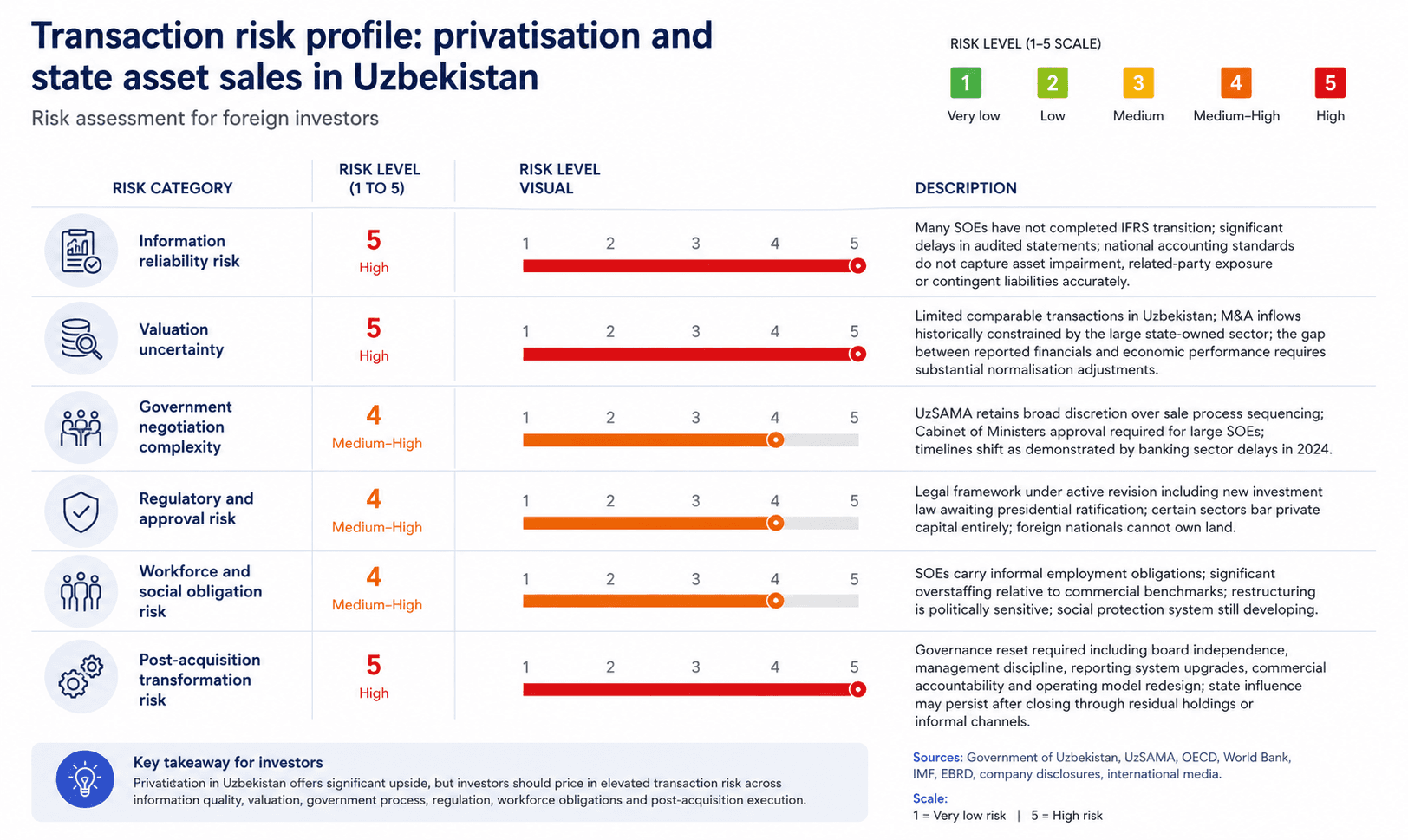

Where Foreign Investors Miscalculate Privatisation Risk

Foreign investors in Uzbekistan's privatisation process face recurring analytical errors that are not visible from published asset lists or reform headlines. Three of these are particularly consequential.

The first and most costly is treating official financial statements as a reliable basis for valuation. According to an August 2025 review by the ESG Foundation, 22 major enterprises including Uzavtosanoat, Uzkimyosanoat, Uzmetkombinat and Uzbekneftegaz had not yet completed the transition to International Financial Reporting Standards. While the largest mining companies such as NMMC and AMMC have institutionalised IFRS reporting with Big Four audits, many target enterprises still produce financial statements under national accounting standards that do not adequately reflect asset impairment, contingent liabilities, related-party transactions or working capital positions. The gap between reported figures and normalised earnings is often substantial. Investors who rely on headline financials without independent adjustment will misprice the asset, and the absence of deep comparable transaction data in Uzbekistan makes cross-referencing more difficult than in established M&A markets. Firms navigating valuation challenges in complex markets with limited transaction comparables will recognise this as a structural rather than incidental constraint.

The second miscalculation is assuming that government approval of a sale translates to transaction certainty. The OECD's 2025 Investment Policy Roadmap for Uzbekistan documents that SOEs continue to receive preferential treatment in access to land, finance and investment incentives, which distorts competitive dynamics and can complicate transactions where the state is simultaneously seller and regulator. The experience of OTP Group's acquisition of Ipoteka Bank illustrates realistic timelines: negotiations began in late 2020, the transaction was announced in 2022 and closed in June 2023, with OTP first acquiring a 75% stake followed by the remaining 25% in a phased process. From initial engagement to financial closing, the process took nearly three years. This is consistent with what privatisation advisory in Uzbekistan should prepare investors for: a deliberate, multi-stage engagement rather than a conventional M&A timeline.

The third is underestimating workforce and social obligations. SOEs remain major employers in many sectors, and some enterprises carry staffing levels materially above commercial benchmarks. The broader labour market context reinforces this sensitivity: the ILO estimates that approximately 40% of Uzbekistan's workforce is employed informally, which means that visible employment at SOEs carries disproportionate social and political weight. Post-acquisition headcount restructuring is legally permissible but politically sensitive, and the informal social obligations that accompany many privatised assets do not appear on the balance sheet. Any serious approach to buying state-owned enterprises in Uzbekistan must account for these obligations in the transaction structure and in post-closing workforce planning.

Framework for Participating in Privatisation in Uzbekistan

The table below sets out the advisory areas, practical questions and investor decisions that define disciplined participation in the Uzbek privatisation programme.

Table: Privatisation Participation Framework for Foreign Investors

Advisory area | Practical question in Uzbekistan | What foreign investors should clarify |

|---|---|---|

Target identification | Is the asset genuinely available, strategically attractive and aligned with investor objectives? | Sector priority within UzSAMA's current programme, sale process readiness, state objectives for the entity, asset quality versus political visibility and realistic timing for transaction launch |

Due diligence | Is the available information sufficient for an investment decision? | Reliability of financial statements (IFRS versus national standards), undisclosed liabilities, management cooperation during data room access, operational data gaps and the extent of state-directed revenues that may not continue under private ownership |

Valuation | Can the asset be priced despite limited comparables and uncertain reporting quality? | Normalised earnings after adjusting for state-directed lending or procurement, deferred maintenance and capex requirements, working capital distortions, contingent liabilities and appropriate downside scenarios reflecting regulatory and operating uncertainty |

Bid structuring | Does the proposed structure protect the investor while remaining acceptable to the seller? | Conditions precedent, governance rights after closing, dispute resolution mechanisms, financing structure, regulatory approvals and the government's stated objectives for employment continuity and social outcomes |

Post-acquisition transformation | Can the former SOE become a commercially disciplined business within 12 to 24 months? | Governance reset including board composition, management capability assessment, workforce adjustment plan, financial reporting upgrades to international standards, operating model redesign and establishment of commercial accountability structures |

The critical point for any advisory engagement in this area is that target selection, due diligence, valuation, bid structuring and post-acquisition transformation cannot be treated as separate sequential workstreams. Buying a state asset is not complete when the deal closes. Value is created only if governance, management discipline and operational execution are addressed after acquisition with the same rigour applied to the transaction itself. Firms requiring M&A transaction and post-deal integration support for complex acquisitions should ensure that their advisory team covers each of these five dimensions with equal depth, particularly in markets where institutional maturity is still developing and the seller retains regulatory authority over the acquired business.

What Foreign Investors Should Assess Before Submitting a Bid

The purpose of advisory in this context is not to confirm that buying state assets in Uzbekistan is attractive. It is to determine which assets are investable, how they should be valued, how the bid should be structured and what transformation plan is required after closing. Firms considering market entry and business expansion support for foreign investors should address the following questions before committing transaction resources.

Is the asset strategically valuable or only politically visible? The 2025 programme includes thermal power plants, automotive producers, telecommunications companies, agricultural holdings and financial institutions. These represent fundamentally different transaction profiles. The planned international listing of NMMC, for which Rothschild & Co is advising, signals a capital-markets approach with institutional investor participation. A regional UzSAMA auction for a processing facility or hotel involves a different risk structure, different due diligence scope and different post-acquisition requirements. Treating these as equivalent opportunities is an analytical error.

Is the financial information reliable enough for a valuation? The December 2024 presidential decree mandating that all large SOEs complete IFRS transition by mid-2025 represents progress, but implementation across 22 enterprises that have not yet adopted international standards will take time. Where IFRS-audited financials are not available, investors should budget for independent financial analysis as part of the transaction cost rather than relying on vendor-prepared materials.

What transformation is required in the first 100 to 180 days? The Ipoteka Bank case is instructive. Following OTP Group's acquisition, the bank introduced international guarantees, trade finance products and new technology platforms, and developed a five-year transformation strategy. But delivering this required management restructuring, resistance to informal state-directed lending requests and sustained investment in operational capability. Post-acquisition transformation in Uzbekistan demands governance clarity, operational capacity and political patience that extend well beyond the bid itself.

For firms seeking senior advisory support for acquisition and privatisation decisions, the starting point is not the purchase price. It is whether the investor has a credible plan for what happens after closing.

Conclusion

Privatisation in Uzbekistan creates genuine opportunities for foreign investors. The government's commitment is demonstrated by the scale of the programme, the engagement of international advisers and the landmark UzNIF offering that opened in 2026 with $300 million in cornerstone institutional commitments. But not every state asset on the programme list is investable on the same terms. Participation in the privatisation process requires disciplined target selection, due diligence adapted to local information constraints, valuation judgement calibrated to limited comparables, planning for government negotiation dynamics and a realistic post-acquisition transformation programme covering governance, management, reporting and operating discipline. Investors who bring this level of rigour will be positioned to capture real value from what is one of the most significant state asset sale programmes in Central Asia.

For foreign investors assessing state asset sales or former SOE acquisitions in Uzbekistan, Tretiakov Consulting provides senior advisory support across target evaluation, due diligence, valuation, transaction structuring and post-acquisition transformation.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.