Strategic Challenges Facing the Chemicals Sector in the Netherlands

Dutch chemical production sits well below its 2022 peak. Order books at major operators across Chemelot, Rotterdam-Moerdijk and the northern cluster have been thin for most of 2024 and 2025, and recent manufacturing data from Statistics Netherlands places chemicals among the weakest-performing manufacturing sub-sectors. Boards continue to describe the situation as cyclical. It is not. The chemicals sector in the Netherlands is being reshaped by forces that will not reverse on the timeline most current business plans assume, and the boards that wait for normalisation will inherit decisions made for them by energy costs, permitting authorities, and acquirers operating from different cost bases.

This article sets out the structural pressures, the strategic postures available to operators, and the governance discipline required to choose between them.

The structural cost squeeze: energy, carbon and the comparative gap

The Dutch problem is not generic European weakness. It is specific to a cluster economy built on cheap pipeline gas, deep integration with German and Belgian downstream chemistry, and permitting that tolerated industrial expansion until the late 2010s. Two of those three conditions have changed.

European natural gas, priced off the Dutch TTF benchmark, trades at a multiple of US Henry Hub that has moved from a historical ratio of around two to current levels of three to five. The Draghi report on European competitiveness, published in September 2024, set the gap formally at two to three times for industrial electricity and four to five times for natural gas. For a steam cracker, a chlor-alkali plant or an ammonia synthesis loop, that ratio does not translate into a cost disadvantage at the margin. It translates into negative gross margin under most operating scenarios, before depreciation, before carbon, and before regulatory overhead.

The carbon cost progression sits on top of this. EU ETS allowance prices, the gradual withdrawal of free allocations for energy-intensive industry, and CBAM implementation on imports do not add to the energy cost burden. They multiply it, because the cash flow effect compounds with each tonne of CO2 not yet abated. A Dutch chemical industry strategy that models energy and carbon independently will produce numbers that are wrong by a meaningful margin.

Electrification helps in part. The IEA's Renewables for Industry analysis notes that around thirty per cent of chemical process heat sits below 200°C and is technically addressable by heat pumps, electric boilers and resistance heating. The other seventy per cent is not. It requires low-carbon hydrogen, carbon capture or alternative feedstocks, none of which is operating at commercial scale on the timelines most current Dutch chemical industry strategy documents assume.

Why waiting for gas prices to normalise is not a strategy

Even an optimistic gas-price scenario does not close the structural gap with US Gulf Coast competitors who locked in feedstock advantages a decade ago. The decision is not whether the cost environment will improve. It is what to do while it does not.

Regulation, permitting and the limits of operating in a dense country

Regulatory pressure is the second axis along which the chemicals sector in the Netherlands is being reshaped, and the one boards consistently underestimate because the timelines look distant on a regulatory calendar but are immediate on an investment calendar.

The universal PFAS restriction proposal, submitted in 2023 jointly by the Netherlands, Denmark, Germany, Norway and Sweden, was updated by ECHA in August 2025 following more than 5,600 stakeholder comments. ECHA's scientific evaluation is scheduled to conclude in 2026, with the SEAC draft opinion expected in the first half of that year. Eight additional sectors have been brought into scope. Derogations are under active discussion. The right reading is not that PFAS will be banned by a specific date. The right reading is that any production line in the Netherlands with fluorochemistry in the value chain is now operating under decision pressure, regardless of whether the final restriction lands at the strict or moderate end of the option spectrum.

The European Commission's Clean Industrial Deal and the accompanying Chemicals Industry Action Plan, published respectively in February and July 2025, point in a partially compensating direction. State aid flexibility, ETS revenue recycling, and the Omnibus simplification packages are designed to relieve the regulatory and energy-cost burden on the European chemicals industry. None of these instruments is yet fully operative. Boards that treat the Action Plan as enacted relief are misreading the politics. Boards that dismiss it as marketing will miss the funding windows when they open.

Then there is the nitrogen problem. Permitting expansion of industrial sites near Natura 2000 areas has become slow, contested, and in several cases practically impossible. Even maintaining existing operations now requires defending permits that were not previously contested. The densely populated geography that historically supported the Dutch cluster model now constrains it. There is no engineering fix for distance to a residential zone.

The portfolio choice: keep, transform or relocate

The portfolio choice, in chemicals and across the materials industry in the Netherlands more broadly, is the decision most boards have been postponing. The reason is structural rather than analytical. Each posture creates different communication problems with employees, customers, regulators and shareholders, and there is no posture without losers.

The four available postures are summarised below.

Strategic posture | When it is rational | Capital intensity | Principal execution risk | Governance requirement |

|---|---|---|---|---|

Defend and electrify | Specialty offtake, integrated cluster position, eligibility for maatwerk support | High, front-loaded | Infrastructure dependency: hydrogen and CCS schedule slippage | Long-cycle capital governance; tolerance for negative NPV in early years |

Shift to specialty | Existing R&D depth and customer technical service; commodity exposure eroding margin | Medium-high; capability-heavy | Capability gap: specialties require commercial skills basic chemistry teams do not have | Acquisition or build of specialty commercial function; talent strategy |

Build circular capability | Brand, customer or regulatory pressure makes circularity a licence-to-operate condition | Medium; uncertain returns | Feedstock supply consistency; technology immaturity in chemical recycling | Patient capital governance; partnership-led structure |

Relocate or rationalise | Production economics do not work under any reasonable energy or carbon scenario | Negative (capital released) | Reputational, workforce and customer-continuity management | Board-level decision authority; clear communication architecture |

Doing all four at once is not a strategy. It is what happens when a board cannot decide. The most expensive position in Dutch chemicals today is the half-committed one, where capex flows into partial electrification, partial specialty conversion, and partial maintenance of declining commodity lines that will not exist in five years.

The Chemelot industrial park strategy illustrates the point. Chemelot operates as an integrated cluster where utilities, feedstocks and infrastructure are shared across operators. Partial decarbonisation of one operator without coordinated decisions across the cluster risks stranding shared assets, which is why the Chemelot industrial park strategy has become a test case for whether integrated clusters can be partially transformed without losing critical mass. The lesson generalises. Chemical industry transformation in the Netherlands is rarely a single-operator decision. It is a cluster-coordination problem dressed up as a corporate one, and the governance design needed to address it sits above the boundaries of any one company.

A serious approach to chemicals and materials industry advisory treats the portfolio decision as the entry point to every other discussion. Operating model redesign, capital deployment and M&A positioning are downstream of the portfolio choice, not parallel to it.

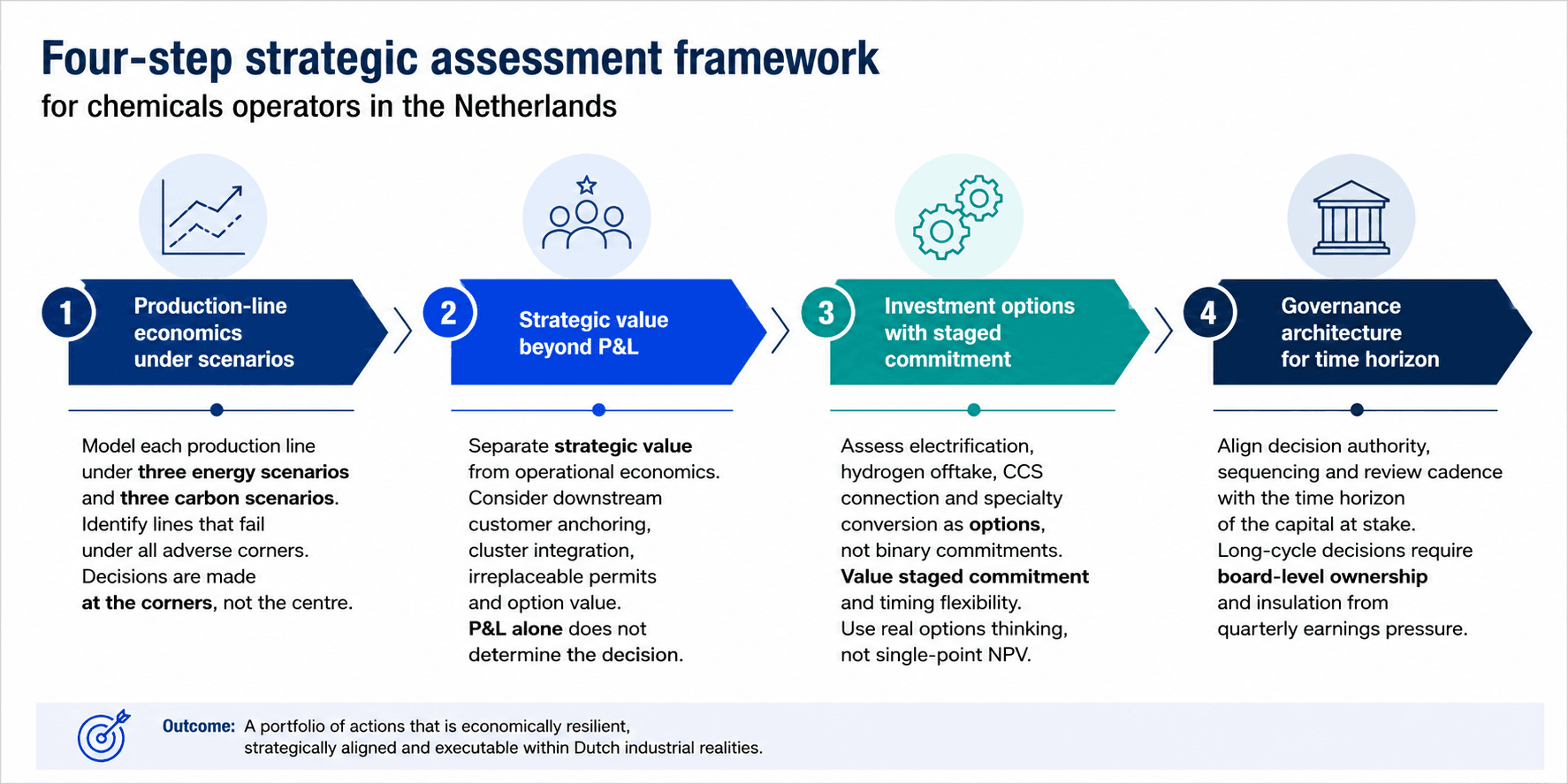

A framework for strategic assessment

The framework runs in sequence. First, model each production line under three energy scenarios and three carbon scenarios. Do not average them. Decisions are made at the corners of the scenario matrix, not at its centre. A line that survives the base case but fails under any adverse corner is a line under decision pressure, regardless of its current cash contribution.

Second, separate strategic value from operational economics. A loss-making line that anchors a downstream customer, integrates into a shared utilities network or holds a permit that cannot be replicated is not the same as a loss-making line that does not. Companies routinely close the wrong assets because the P&L view dominates the strategic view in management reporting.

Third, price investment options with optionality, not point estimates. Electrification, hydrogen offtake, CCS connection and specialty conversion are options, not binary commitments. Net present value calculations that ignore the value of staged commitment will systematically over-reject viable investments. This is one of the most common analytical failures inside Dutch chemical investment committees.

Fourth, build the governance architecture appropriate to the time horizon. A capital decision with a fifteen to twenty-year payback cannot be made by a CFO function under quarterly earnings pressure. Where Dutch operators most often fail is not in the technical analysis but in the decision architecture surrounding it. Chemical industry transformation in the Netherlands almost always requires business transformation and operating model redesign before the operational change itself can be sequenced.

The transaction dimension

The European specialty chemistry segment, and the broader materials industry in the Netherlands, is consolidating quietly through carve-outs, private equity acquisitions and bilateral swaps that rarely reach the headlines. The pattern matters because it changes the strategic options available to boards that have not yet made portfolio decisions.

Three transaction realities deserve attention. Majors are carving out non-core specialty assets at a pace that creates real acquisition opportunities for focused buyers. Mid-cap Dutch specialty producers are increasingly approached as targets by private equity sponsors seeking European footprint at distressed valuations. Divestment of an underperforming line to a strategic acquirer with a different cost base can be value-creating for both sides. Most boards lack the M&A discipline to act on this last insight, partly because it requires admitting that the right owner of an asset is not always the current owner. Disciplined M&A advisory and post-merger integration work changes that calculation by separating the ownership question from the operational question.

Joint ventures, infrastructure-sharing arrangements and tolling agreements are doing transactional work that pure M&A does not. A hydrogen offtake structure, a shared CCS connection or a cluster-level utilities arrangement can reshape the economics of a production line without changing ownership. Boards considering industrial investment and capital projects advisory increasingly find that the transaction question and the investment question are the same question, sequenced differently.

Diligence in this environment requires distinguishing visible activity from investable opportunity, and investable opportunity from executable integration. Announced electrification, hydrogen and CCS capacity is not commissioned capacity. The gap between announcement and commissioning is where many Dutch transformation business cases will be settled, and where most of the value will be lost or gained.

The decision window

The chemicals sector in the Netherlands is not waiting for clarity. Clarity is already present. Energy costs are structurally higher than in the United States and Asia for the foreseeable horizon. Regulatory pressure on fluorochemistry, on permitting and on environmental compliance is tightening. Cluster economics that supported the Dutch position for forty years are being renegotiated, often without explicit decisions by the operators inside them.

Boards that make explicit portfolio choices in the next twenty-four months will shape the next decade. Boards that defer will discover that energy costs, regulators and acquirers make the decisions for them, rarely in the order the company would have chosen. Dutch chemical industry transformation and growth, taken together, is no longer a single-track story. The strategic challenges for the chemicals and materials sector in the Netherlands are not abstract policy questions. They are commercial decisions that map onto specific assets, specific permits and specific capital commitments. The companies that treat them as such will benefit from the chemicals sector outlook and advisory in the Netherlands that survives the next cycle. The rest will be advised by their balance sheets.

Tretiakov Consulting works with boards, owners and investors on portfolio strategy, capital deployment and transaction positioning across the Netherlands, with senior advisory teams active in business transformation and operating model redesign and industrial investment and capital projects.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.