Governance in Dutch Mid-Market Companies and Board Effectiveness in Practice

The boards that actually carry Dutch mid-market companies through succession events, sponsor exits and tightening ESG scrutiny do not stand out for the elegance of their charters. They stand out for how their information flows, how their commissarissen are recruited and how decisions move between management and supervision under real pressure. That is the working reality behind governance in Dutch mid-market companies, and it is the layer the legal framework, by design, does not reach. Statutory reform has redrawn the perimeter of board duties through the Wet bestuur en toezicht rechtspersonen, the Dutch Corporate Governance Code was substantively updated in March 2025, and lender expectations are tightening. Even so, the operational gap between what the Code prescribes for listed issuers and how a privately held BV actually runs its supervisory board has, if anything, widened. This article looks at four pressure points that determine whether oversight produces better commercial decisions: board composition, information flow, the working relationship between bestuur and raad van commissarissen, and the distance between regulatory expectation and boardroom behaviour.

The Dutch governance architecture and why the two-tier model behaves differently in the mid-market

The Netherlands sits in a small group of jurisdictions that still favour a dualistic structure. The OECD Corporate Governance Factbook 2025 records that of fifty-two surveyed jurisdictions, only seven favour a two-tier board while eighteen permit both forms. The one-tier variant has been available in the Netherlands since 2013 yet the two-tier board structure in the Netherlands remains dominant above the smallest privately held companies. The bestuur manages, the raad van commissarissen supervises, and the legal separation is intended to protect oversight quality.

In the mid-market that separation behaves differently than in a listed AEX-25 issuer. The Code, maintained by the Monitoring Commissie Corporate Governance Code, applies on a comply-or-explain basis to listed companies above a €500 million balance-sheet threshold. Almost every mid-market company sits below that threshold. The Code therefore reaches the mid-market only indirectly, through Dutch banks, private-equity sponsors, insurers and pension funds that use it as a working benchmark for credit and portfolio work. The visible governance architecture exists; the supervisory pressure that animates it in a listed context does not, in the same form, exist below the listed perimeter.

What the WBTR actually changed for mid-market boards

The Wet bestuur en toezicht rechtspersonen, adopted by the Eerste Kamer as legislative file 34.491 and in force since 1 July 2021, harmonised the rules on management and supervision across all Dutch legal entities, including BVs, NVs, foundations, cooperatives, and associations. It clarified the duties of directors and commissarissen, addressed conflicts of interest, removed binding tie-breaking votes where they had quietly entered statutes, and tightened liability where a board has been negligent.

The mid-market issue is not the law itself. It is that many BVs and foundations still operate as though WBTR applied only to large institutions. Statutes drafted in 2014 remain in use, conflict-of-interest protocols exist on paper but have never been tested, and the raad van commissarissen of a family-controlled BV has often not formally rebalanced its decision rules. Governance reform for Dutch BVs and foundations under the WBTR is, in a strictly legal sense, complete. In an operational sense, in most companies, it is still being absorbed.

Where raad van commissarissen effectiveness actually breaks down

Strip the legal cover away and the pattern is consistent. The first failure is composition. Dutch mid-market boards are still recruited from a narrow network of advisers, former lenders, sector veterans and former colleagues of the founder. Formal independence in the sense of the Code, meaning the absence of a material business or family relationship with the company, is usually achievable on paper. Social independence, meaning the willingness to challenge a sitting CEO with whom a commissaris has shared a region, a sector, and twenty years of professional history, is materially harder to engineer.

The second failure is sizing. A raad van commissarissen of three is too thin to support a credible audit committee, a remuneration committee and serious succession work in parallel. A board of seven becomes a deliberative body that struggles to move at the pace a private-equity sponsor or a turnaround situation demands. Most mid-market companies have not made the structural choice consciously, and most boards therefore default to whichever size emerged from the last appointment cycle.

The third failure is the information asymmetry the system structurally produces. The board pack is drafted by the bestuur, framed by the bestuur and presented by the bestuur. The raad van commissarissen is then expected to challenge management on the same numbers, without independent access to the operational layer below the board. The 2025 Code update introduces a new risk management statement, the Verklaring omtrent Risicobeheersing, applicable from financial year 2025, which is a serious attempt to force substantive engagement between management and supervision on operational, compliance and reporting risk. Whether mid-market companies that voluntarily adopt elements of the Code engage with it substantively or treat it as a documentation exercise is the open question.

The fourth failure is time. Commissarissen who hold five or six mandates, often spread across foundations and BVs, cannot give any single board the operational attention it requires. Raad van commissarissen effectiveness in this environment is not a function of intent. It is a function of capacity, and in family-controlled companies, of interim leadership at the management layer that can give the supervisory board something substantive to supervise.

The overleg culture and the polder effect on board decisions

Dutch consultative decision-making, the overleg tradition and the broader polder model, shape board behaviour in ways an outside observer often misreads as weakness. Consensus-seeking on a Dutch supervisory board is not avoidance. It is a deliberate method that, when it works, produces durable decisions with broad stakeholder alignment. When it does not work, it produces slow decisions, late confrontation of underperforming management, and a structural reluctance to vote against a CEO whose tenure is being defended by the chair.

The commercial cost surfaces in three places. In turnaround situations, where speed of decision matters more than completeness of consultation, the polder reflex is materially expensive and often requires a parallel operating-model reset to give the board something concrete to decide on. In private-equity ownership, where the sponsor's fund timeline is not negotiable. And in succession events, where consensus is mistaken for resolution and a transition that should have taken nine months runs to twenty-four.

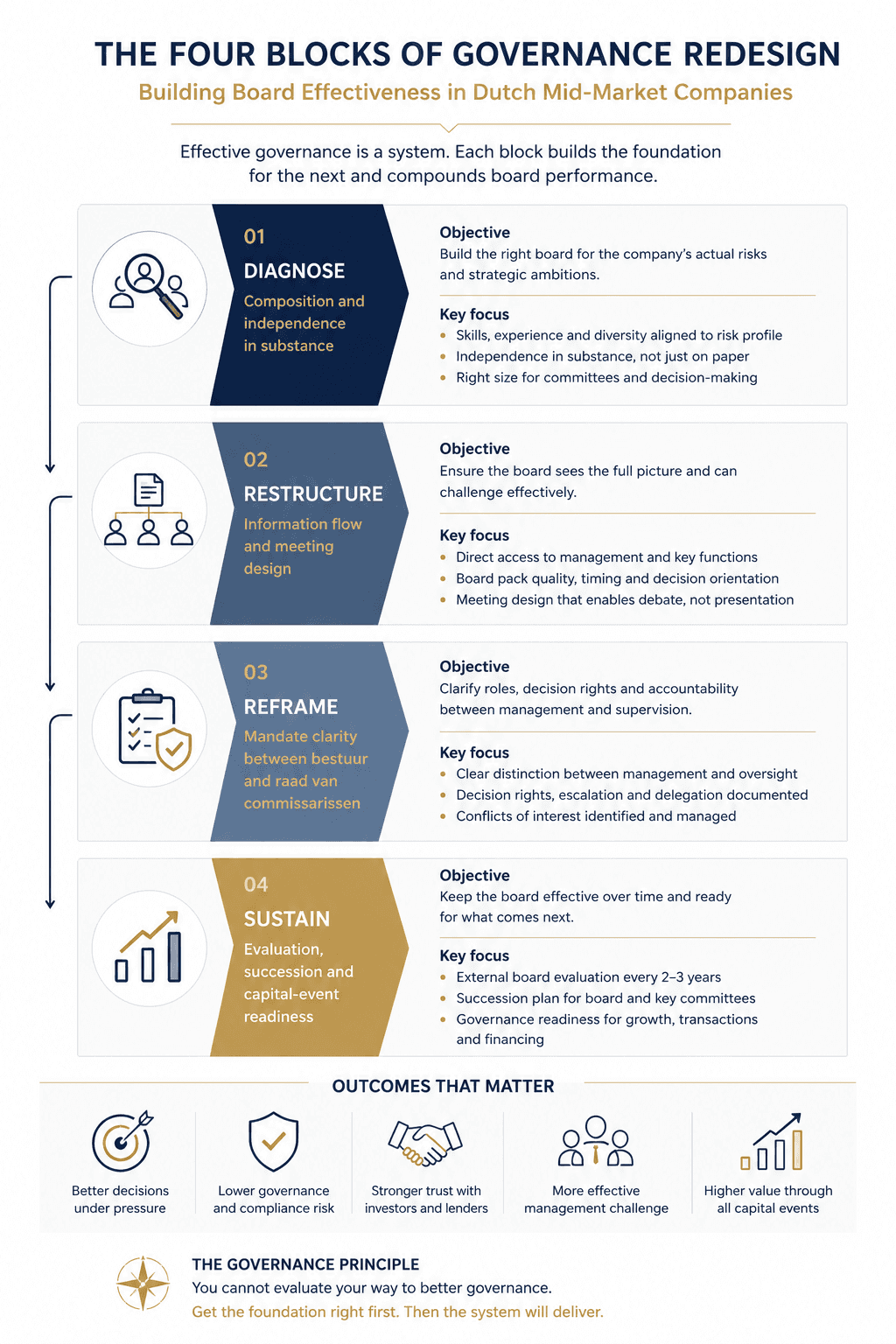

A practical framework for improving governance in Dutch mid-market companies

The mid-market boards that perform under pressure share four design choices, which can be sequenced as a working diagnostic for owners, sponsors and chairs. The framework is structural rather than aspirational; each block produces a board that decides better, not a board that reads better.

Dimension | Common mid-market reality | Effectiveness signal | Typical intervention |

|---|---|---|---|

Composition | Network-sourced commissarissen with functional gaps in cyber, ESG and treasury | Independent expertise tested against the company's actual risk profile | Targeted recruitment outside the founder's network, with clear term limits |

Information flow | Board pack drafted entirely by the bestuur | Direct access to the layer below the board and an independent internal-audit reporting line | Restructured pack and standing access to operational management |

Mandate clarity | Supervisory role blurred with advisory role | Documented separation, with advisory work flagged and minuted | Charter revision and an explicit conflicts protocol |

Evaluation and succession | Internal self-assessment, reactive succession | External facilitation every two to three years, documented pipeline for both boards | Structured evaluation programme and a written succession charter |

Visual framework: the four blocks of governance redesign

Read top to bottom. Diagnose covers composition and independence in substance. Restructure covers information flow and meeting design. Reframe covers mandate clarity between bestuur and raad van commissarissen. Sustain covers evaluation, succession and capital-event readiness. The blocks are sequential because attempting evaluation reform on a board with the wrong composition produces a report, not a change.

Improving board effectiveness in Dutch mid-market companies depends on completing all four blocks. Most mid-market boards have completed one, occasionally two. That is the gap that becomes commercially expensive at the moment a transaction or a downturn forces the board to actually decide.

Governance, transactions and capital

Governance defects are systematically priced into transactions. The mechanism is straightforward. A sponsor's due diligence reveals a thin or conflicted raad van commissarissen, a board pack that does not support an audit trail, and an executive team running without genuine supervisory challenge. The result is warranty exposure, longer diligence cycles, restructured earn-outs, or a multiple discount the seller is unable to articulate but the buyer can defend.

Sponsors who acquire Dutch mid-market companies typically redesign the raad van commissarissen in the first one hundred days post-deal, and the same redesign discipline matters at the post-merger integration stage of any transaction. The point is not that PE governance is intrinsically superior. The point is that PE governance treats board design as a value lever rather than a compliance topic.

The capital side is moving in the same direction. De Nederlandsche Bank, in its supervisory framework on governance, behaviour and culture, makes explicit that these themes are core supervisory matters for financial institutions on the understanding that poor financial results often originate in inadequate governance. That stance has practical consequences for non-financial mid-market borrowers, because Dutch banks now carry the same expectation into their credit and ESG conversations with clients. Corporate governance in the Netherlands is moving, in commercial substance if not in legal form, into the perimeter of lender risk management.

The structural backdrop is worth keeping in proportion. Eurostat's structural business statistics show that small and medium-sized enterprises form the dominant share of active enterprises in the EU business economy, with the Netherlands among the most service-weighted member economies. That density is the reason board design in the Dutch mid-market is not a niche concern. It sits at the centre of how the productive base of the economy actually transacts, borrows and changes ownership. Targeted board advisory and governance support earns its commercial keep here, particularly where owners, sponsors and chairs treat the raad van commissarissen as a strategic asset rather than a statutory checklist.

Conclusion

The Dutch mid-market boards that perform under real pressure are not the ones with the most polished governance documentation. They are the ones that have done the unglamorous structural work: rebuilding composition outside the founder's network, restructuring information flows so that supervision is not dependent on the same data management writes, and setting an evaluation cadence that actually changes who sits in the room. Reform has set the legal perimeter, the Code sets the benchmark, and lender expectations are rising. The boards that close the gap between those perimeters and their actual practice are the ones that turn governance in Dutch mid-market companies from a compliance topic into a value-protection tool. For owners, sponsors, and chairs working in the country, Tretiakov Consulting's advisory work in the Netherlands and board advisory in the Netherlands address exactly that gap, particularly where capital events, succession or operational pressure are forcing the question.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.