Go-to-Market Strategy Consulting in the Netherlands

Foreign-owned and mid-market companies routinely mistake distribution coverage for commercial control. In a market where growth is now thin and has to be taken rather than received, that mistake quietly costs them the margin they can least afford to lose.

Most companies that sell into the Netherlands believe the difficult part is behind them once a distributor is signed and stock is sitting near Rotterdam. The orders confirm it, the coverage map looks complete, and the commercial position appears settled. It is not, and the reason go-to-market strategy consulting in the Netherlands has moved off the sales team's desk and onto the agenda of owners and boards is that this comfortable-looking arrangement quietly hands away the three things that decide whether the business makes money. The customer relationship, the pricing decision and the demand signal now sit with a third party whose interests only partly overlap with the principal's, and the transfer happens without anyone deciding to make it. What looks like market entry is in fact the surrender of commercial control.

This matters because of how the Dutch market actually clears product. A large portion of goods is handled by distributors who purchase for their own account and distribute throughout the country and the wider European market, as the United States International Trade Administration sets out in its country commercial guide for the Netherlands. In that model the principal typically sells once, into the channel, and then loses sight of the end customer. It sees volume rather than demand. When a segment softens it cannot tell whether the cause is price, a competitor, a specification change or simply a distributor reallocating effort towards a higher-margin line, and it has no instrument with which to respond, because it never built one.

For most of the past decade that was tolerable, because volume tended to rise and the cost of the missing visibility stayed hidden inside a growing market. That cover has gone. The OECD's 2025 economic survey of the Netherlands puts growth at roughly 1.3 per cent for 2025 and 1.1 per cent for 2026, and the IMF's most recent assessment is broadly consistent, with output expanding close to one per cent and the balance of risks tilted to the downside in its 2026 Article IV concluding statement. When the market is barely moving, revenue has to be taken from competitors or recovered from inside the channel, and neither is available to a company that cannot see past its own distributor.

The gateway advantage is also a commercial trap

The Netherlands is one of the most efficient places in the world to move goods. It sits at or near the top of the World Bank's Logistics Performance Index, and the OECD describes it as Europe's gateway, integrated deeply into global value chains through its location, low trade friction and efficient border procedures. Rotterdam is the largest port on the continent. For a company arriving from outside, this is read as evidence that market access is straightforward, and the natural response is to invest heavily in the logistics layer, the warehousing, the third-party fulfilment, the customs handling, and to treat the commercial layer as something that will follow.

The error sits in the word access. A great deal of what crosses Dutch borders is transit and re-export rather than domestic consumption, which means the trade and throughput figures that make the country look like a large market substantially overstate the addressable demand inside it. Logistics performance measures how well goods pass through. It says nothing about whether a buyer in Eindhoven or Utrecht will switch supplier, at what price, on what terms or against which incumbent. A firm that confuses the two builds an efficient route into a market it has not yet learned how to sell to, and a sound distribution strategy in the Netherlands has to begin by separating the physical question of moving product from the commercial question of who decides to buy it. Foreign companies in particular tend to over-resource the first and under-resource the second, then conclude that the market is difficult when in reality their commercial design never existed. A credible go-to-market strategy for foreign companies in the Netherlands therefore has to begin with the commercial design that the efficiency of the gateway tempts them to defer.

Who actually owns the customer

The distributor model is attractive precisely because it removes work. The distributor carries local relationships, credit risk and last-mile coverage, and in return it takes ownership of the end customer. That ownership is the part most principals underestimate. Because the distributor purchases on its own account, it sets the price the customer pays, controls the data the relationship generates and decides how much attention the line receives relative to everything else it carries. The principal becomes a supplier to its own route to market rather than a participant in it.

This produces three consequences that compound over time. Margin is the first, because the distributor's terms, not the end-market's willingness to pay, set the price the principal receives, and once a discount structure is established it is very hard to recover. The second is the loss of the demand signal, which is the more damaging of the two, because without end-customer data the principal cannot see early enough when a segment is shifting, when a competitor is gaining or when a product is being positioned away from its strongest use case. The third is optionality, since a principal that has never built a direct relationship cannot credibly threaten to go direct, and therefore has little leverage when terms are renegotiated.

The right response is rarely to dismantle the distributor relationship, which usually destroys coverage faster than the principal can replace it. A considered route-to-market strategy in the Netherlands treats the question as one of control rather than ownership. It asks how much of the customer relationship, the pricing decision and the data the principal needs to retain in order to manage its own commercial outcome, and then designs the channel around that requirement. For many businesses the answer is a hybrid model in which the distributor continues to handle fulfilment and breadth while the principal builds a direct relationship with its largest and most strategic accounts. A distribution strategy for foreign brands in the Netherlands that keeps the largest accounts inside the principal's own line of sight protects both margin and the ability to read the market, and a route-to-market strategy for industrial companies in the Netherlands usually has to go further still, because specification-led selling and long replacement cycles make the loss of the end-customer relationship even more costly.

When growth has to come from the channel, not the market

In a market growing at around one per cent, revenue growth is almost entirely a function of commercial effectiveness rather than market expansion, and this is the part of the macro picture that actually reaches the income statement. There is no rising tide to carry a weak commercial model, so every point of growth has to be won through pricing discipline, a better product and account mix, higher sales productivity, improved win rates and lower customer churn. These are the components that commercial excellence and revenue transformation are meant to address, and they are exactly the components a distributor-led model hides from the principal.

The constraint is sharper than the growth figure alone suggests, because the Dutch labour market remains tight. The OECD records that around a third of firms cited a shortage of staff as the main obstacle to operating at the start of the second quarter of 2025, which means a company cannot simply add salespeople to buy its way to growth. Commercial headcount is expensive and slow to recruit, so the return on each existing commercial role has to rise. That pushes the entire question towards productivity, coverage design and the quality of the commercial information a business runs on, and this is the terrain that go-to-market strategy consulting in the Netherlands actually has to operate on, rather than the abstract market-sizing exercises that dominate generic advisory work. A serious B2B growth strategy in the Netherlands starts from the recognition that the growth has to be manufactured inside the commercial system, and that the same pressure is shaping the wider commercial strategy of Dutch B2B companies competing internationally.

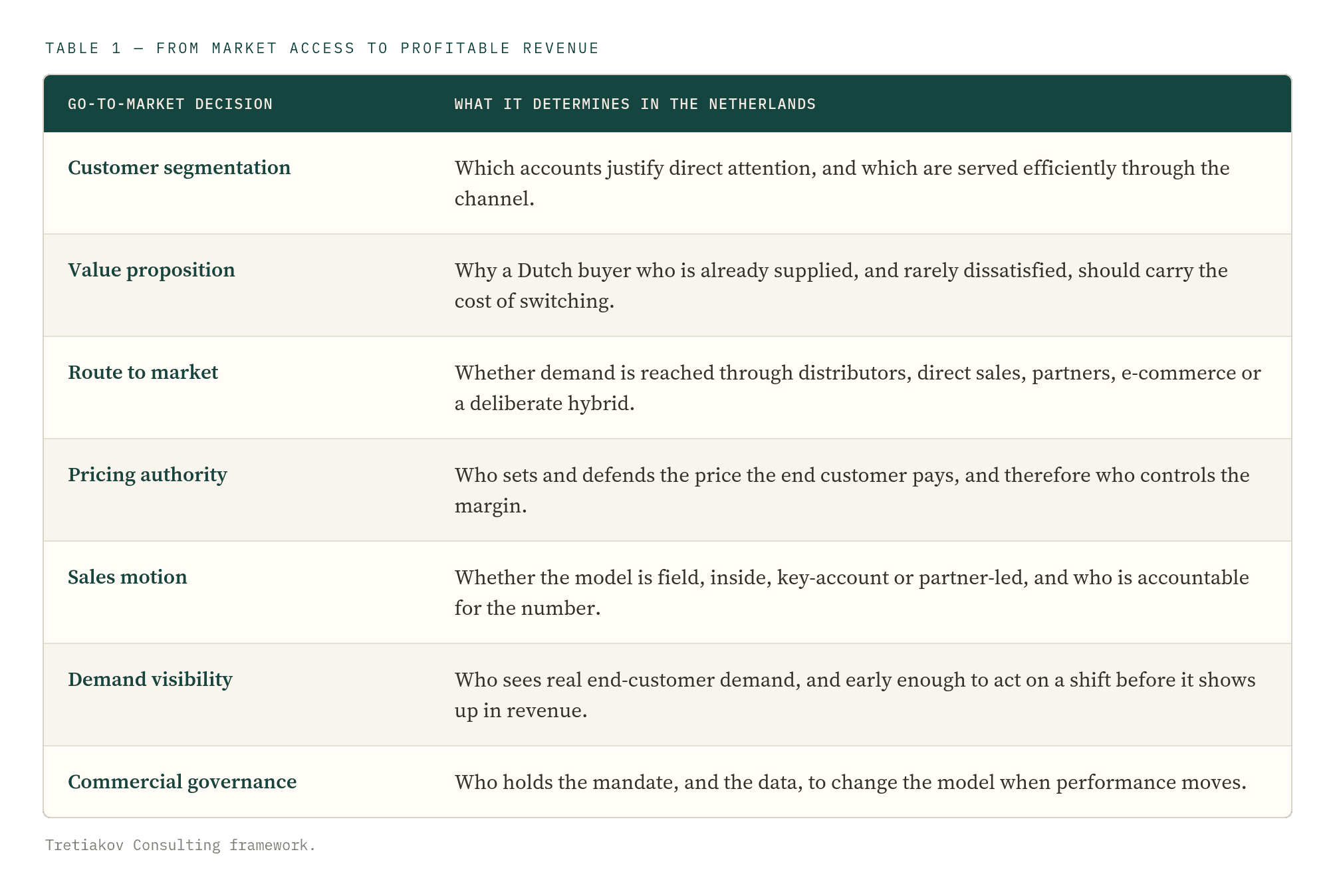

A go-to-market strategy framework for profitable B2B growth

Stepping back from the distributor question, a go-to-market design in the Netherlands is best understood as a connected set of decisions rather than a single channel choice, and each one determines where margin is made or lost. A useful go-to-market strategy framework forces a business to be explicit about all of them at the same time, because weakness in any single decision quietly undermines the others. Precise account segmentation sold through a channel the principal cannot see produces accurate targeting and blind execution in equal measure, and a strong value proposition priced by someone else earns volume for the distributor rather than margin for the principal. The framework matters because it exposes those mismatches before they reach the income statement, and it is the surface on which commercial excellence and revenue transformation are actually built rather than an alternative to them.

The connected go-to-market decisions that determine commercial outcomes in the Netherlands.

Read together, these decisions describe the distance a company has to travel from market access, which the Netherlands makes unusually easy, to profitable and repeatable revenue, which it does not. Most businesses have made three or four of these choices deliberately and left the rest to the distributor by default, and the decisions they never consciously made are precisely where their commercial result is now being set for them.

The quiet re-architecture of B2B buying

While companies argue about distributors, the way Dutch businesses buy is being rebuilt underneath them. Procurement is moving onto structured digital rails, and a commercial model designed around relationships and field visits is being slowly disintermediated by one designed around platforms, catalogues and machine-readable data. The clearest fixed point in this shift is regulatory. Under the European Union's VAT in the Digital Age package, adopted in March 2025, structured electronic invoicing and digital reporting become mandatory for intra-EU business-to-business transactions from 1 July 2030, and member states are already free to require domestic e-invoicing ahead of that date. This is usually filed under tax compliance, which is a mistake. It standardises the data layer of every B2B transaction and accelerates the move of purchasing onto formats and systems that reward suppliers who are integrated and penalise those who are not.

The Netherlands is a demanding place for this transition because its businesses are already highly digitalised, a pattern visible in the European Commission's Digital Decade monitoring and in Eurostat data on enterprise digitalisation. A Dutch buyer is rarely choosing between a manual process and a supplier; it is choosing between suppliers that already fit cleanly into its procurement systems. The direction of travel is reinforced on the consumer side, where Statistics Netherlands reports that retailers whose core activity is selling over the internet have been expanding faster than multi-channel retailers, with online-only retailers growing by around eight per cent year on year against roughly four per cent for multi-channel retailers in the mid-2025 figures. The B2B parallel is that the channel which is easiest to transact with is the one that wins, and that places sales transformation in the Netherlands on the critical path rather than at the margin, and makes sales channel optimisation in the Netherlands a question of access to demand rather than mere efficiency. A company that cannot present its products in a buyer's procurement platform, with clean data and predictable terms, is removed from consideration before any relationship can be brought to bear.

What go-to-market strategy consulting in the Netherlands actually addresses

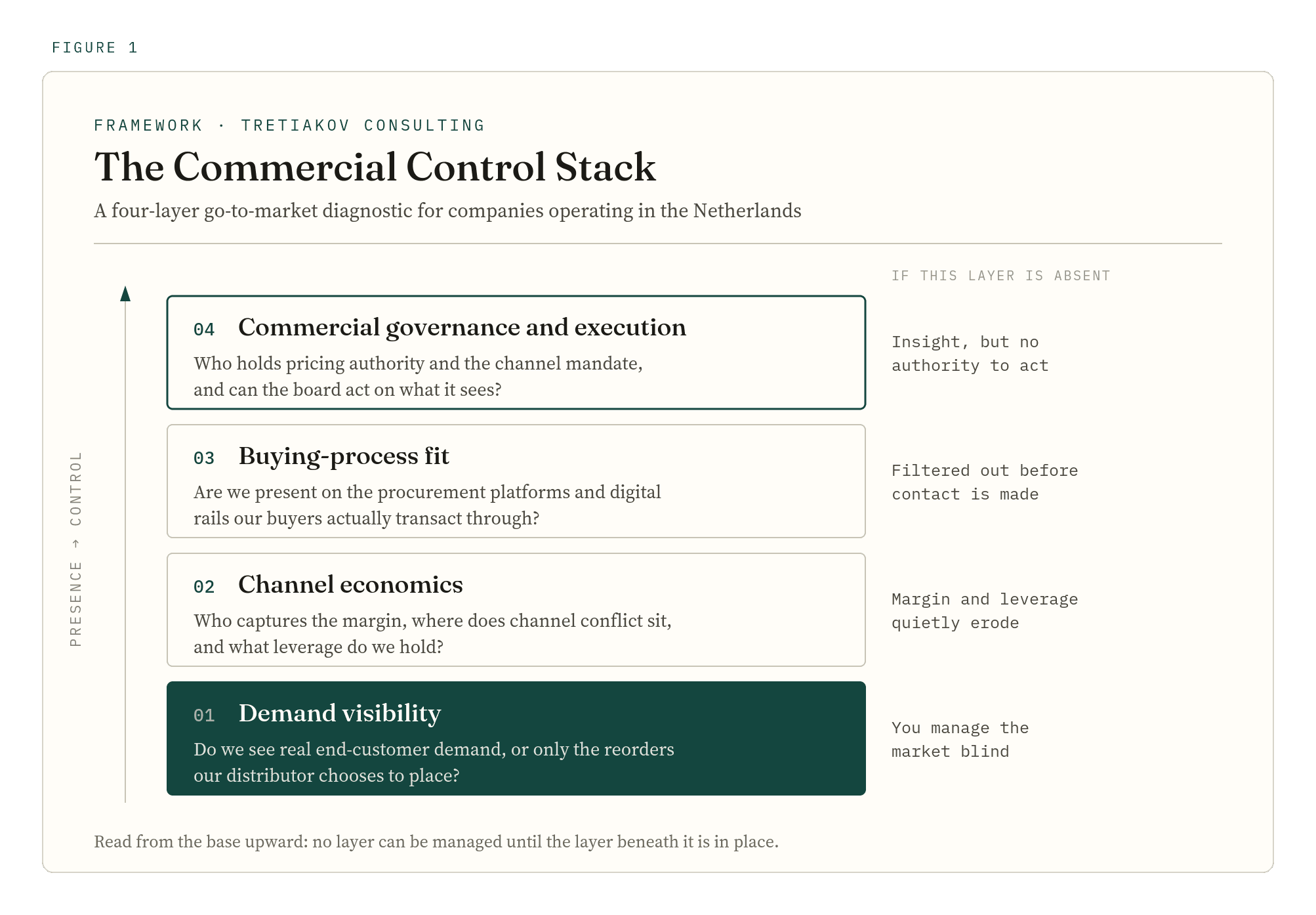

The problems above are not separate. They are layers of the same question, which is how much of its own commercial outcome a business genuinely controls. We use a simple diagnostic to separate the layers, because companies tend to be strong in one and quietly absent in another, and the absent layer is usually where the value is leaking. It runs from the most basic question, whether the company can even see its market, up to whether it can act on what it sees. In practice, go-to-market strategy consulting in the Netherlands begins here, with the stack rather than with a market-sizing model, because the model tends to flatter a position the stack would expose.

The diagnostic reads from the base upward. A business that cannot see end-customer demand (Layer 1) cannot meaningfully manage anything above it, however strong its governance looks on paper. Most distributor-led companies are absent at Layers 1 and 3 while believing their problem sits at Layer 4.

Read from the base, the logic is unforgiving. A company that cannot see end-customer demand has no reliable basis for pricing, for product decisions or for judging whether its channel is performing, so the upper layers rest on guesswork. Commercial transformation for mid-market companies in the Netherlands almost always has to begin by rebuilding demand visibility, because without it every later intervention is applied blind. The same diagnostic explains why companies so often misdiagnose their own situation. They experience the symptom at the top of the stack, a board frustrated that it cannot move the numbers, and assume the problem is execution or people, when the actual failure is two layers down in a channel that was never designed to give them sight of the market.

Reading the Dutch market correctly

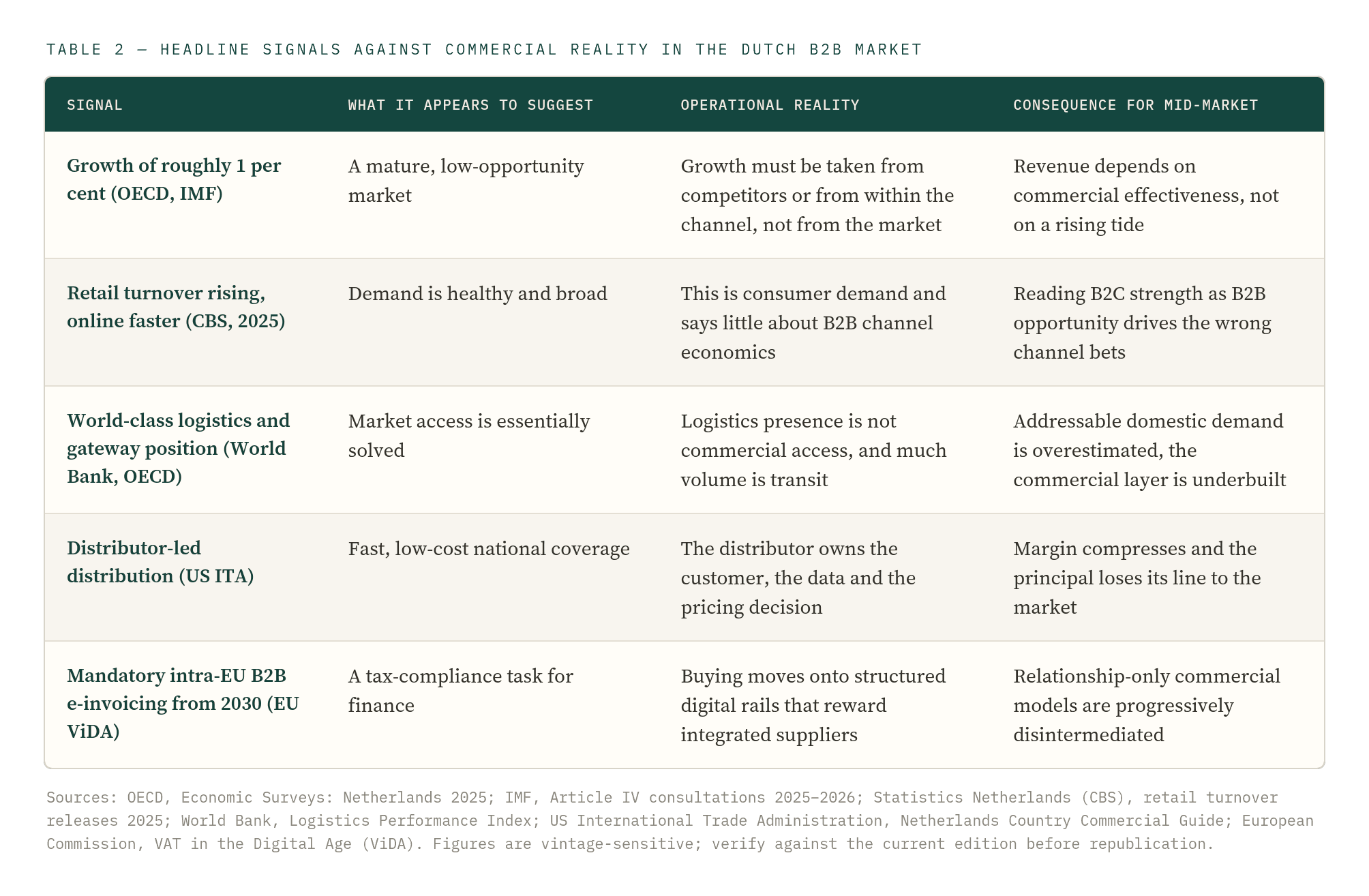

Much of the difficulty is that the headline indicators for the Netherlands point in directions that mislead a commercial planner. The market looks large, efficient and digitally mature, and each of those readings, taken at face value, encourages exactly the wrong allocation of effort. The table below sets the most common signals against the operational reality and the consequence for a mid-market business.

Comparison of headline market signals, their apparent implication, the operational reality and the commercial consequence for mid-market companies.

The pattern across the table is consistent. Every signal that makes the Netherlands look easy is a signal that the commercial work has been displaced rather than removed. The market is reachable, which is not the same as winnable, and the distance between those two words is where most of the value, and most of the disappointment, is found.

Governance and execution: where commercial plans fail

A commercial design is only as good as the structure that runs it, and this is where otherwise sensible plans come apart in the Netherlands. The most common structural weakness is key-person dependence. In many mid-market and foreign-owned operations the entire commercial relationship with the country rests on a single country manager or a single distributor contact, and when that person leaves, the demand signal, the pricing history and the negotiating context leave with them. The business discovers that what it called a market position was in fact one individual's relationships, and it cannot be transferred or governed because it was never written down.

The second weakness is reporting. A board cannot manage what it cannot see, and a distributor-led model frequently leaves the board reading shipment volumes and invoiced revenue while the variables that actually determine the future, win rates, end-customer concentration, price erosion by segment, sit entirely outside its view. Decisions are then made late and on the wrong information. These are not commercial failures in the narrow sense; they are governance failures, and addressing them properly often connects to the wider questions of governance in Dutch mid-market companies and to how authority over pricing and channel is actually allocated inside the business.

The third weakness is that commercial ambition frequently outruns the operating model that has to deliver it. A plan to move from a distributor-led to a hybrid model implies new roles, new systems, new data flows and a different cost base, and where the existing structure cannot support that, the commercial strategy stalls regardless of its quality. This is the point at which commercial design has to be reconciled with operating model redesign in the Netherlands, so that the way the company is organised actually supports the way it intends to sell. Where growth is pursued through acquisition rather than organic channel change, the same discipline extends into transaction advisory and Dutch holding structures, because an acquired commercial platform carries the same questions of customer ownership and data that the buyer was trying to solve in the first place.

None of this is unique to the Netherlands in kind, and the underlying discipline is the same one we apply to commercial growth for European companies expanding across the continent. What is specific to the Dutch market is the combination: a gateway that flatters logistics over commerce, a distributor culture that quietly absorbs the customer relationship, a buying process digitalising faster than most suppliers are ready for, and a flat market that punishes any of these weaknesses immediately rather than eventually.

Conclusion

The Dutch market rewards commercial control rather than commercial presence, and the gap between the two is widening. A company can hold warehousing, a distributor and a clean coverage map, and still have almost no ability to influence its own price, read its own demand or defend its own margin, and in a market growing near one per cent that gap stops being a future risk and becomes a current cost. The work that matters is not market entry, which most companies have already completed, but the recovery of control over a commercial system they handed away without noticing. That is the real purpose of go-to-market strategy consulting in the Netherlands: not to produce another market-sizing deck, but to rebuild the principal's line of sight to its customers, repair the economics of its channel, and prepare its commercial model for a buying process that will not wait for it. Owners and boards that take the question seriously now will be negotiating from a position of control while the rest are still reading reorder volumes and calling it a strategy.

Frequently asked questions

What is a go-to-market strategy?

A go-to-market strategy is the connected set of decisions that turns a market opportunity into profitable, repeatable revenue: which customers to pursue, why they should switch, how to reach them, who controls price, how the sales motion runs and what evidence is required before scaling. In practice it is less a document than a question of control, because the strategy is only real to the extent that the company can see its own demand and act on it. A plan that names target segments but then routes them through a channel the business cannot observe is not a go-to-market strategy; it is an aspiration, and in the Netherlands the difference between the two is measured in lost margin.

How is go-to-market strategy different from marketing strategy?

Marketing strategy is largely concerned with demand generation, with how a company creates awareness, positions itself and brings prospects to the point of interest. Go-to-market strategy is concerned with demand capture and the economics that follow it, with how that interest is converted through a chosen route to market, at what price, through which sales motion and with how much margin retained. Conflating the two is expensive, because a business can run excellent marketing and still lose the commercial outcome at the point where the channel, the pricing authority and the demand data sit with somebody else. In the Dutch market that handover is exactly where most of the value quietly disappears.

We already have a capable Dutch distributor. Why revisit our go-to-market position at all?

Because a capable distributor and a controlled commercial position are different things, and the difference only becomes visible when growth stalls. A strong distributor will move product efficiently, but it does so on its own terms and with its own ownership of the customer, the pricing decision and the demand data. The question to ask is not whether the distributor performs but whether the board can see end-customer demand, defend its margin and act independently if it needs to. Where the honest answer is no, the business is exposed regardless of how well the channel is currently running, and the right response is to redesign the relationship around the control the principal needs to retain rather than to replace a partner that is doing its job.

Is going direct always better than working through distribution in the Netherlands?

No, and treating it as a binary choice is one of the more expensive mistakes in this market. Direct models give the principal ownership of the customer and the data but carry the full cost and complexity of coverage, credit and service in a country where commercial headcount is scarce and expensive. For most mid-market businesses the better answer is a hybrid in which the distributor retains breadth and fulfilment while the principal builds a direct relationship with its largest and most strategic accounts. The design question is which customers, which data and which decisions the principal must own, and the channel is then built backwards from that requirement rather than chosen as an article of faith.

How does the move to mandatory B2B e-invoicing change our commercial model rather than just our finance function?

It changes who gets considered. The European e-invoicing and digital reporting requirements standardise the data layer of cross-border intra-EU business-to-business transactions and accelerate a wider shift of purchasing onto structured platforms, which means buyers increasingly select on the basis of which suppliers fit cleanly into their procurement systems before any commercial relationship is brought to bear. A supplier that cannot present clean product data, predictable terms and platform compatibility is filtered out early, often without ever knowing it was in contention. Preparing for this is a commercial and systems question about being transactable, not a compliance question about issuing invoices, and the companies treating it only as the latter are quietly losing access to demand.

The Dutch market is relatively small. Does it justify a dedicated commercial strategy?

It justifies a sharper one. The Netherlands is a high-value, decision-fast market that also functions as a base into the wider Benelux and German economies, so the return on getting the commercial model right extends well beyond the domestic numbers. The risk in treating a small market casually is that the casual approach is precisely what produces the distributor dependence and the lost demand signal described above, and those weaknesses then travel into the larger surrounding markets a company is using the Netherlands to reach. A disciplined commercial strategy in the Netherlands, and a clear growth strategy for companies entering the Netherlands as a base for the surrounding region, is often the cheapest place to fix a problem before it becomes a regional one.

How long before a commercial transformation shows up in revenue?

The honest answer is that the sequence matters more than the calendar. Rebuilding demand visibility and closing the most damaging points of channel and pricing leakage can begin to show in margin visibility, forecasting quality and pricing discipline within the first few quarters, because these are about seeing and governing what already exists rather than creating new demand. The structural changes, a shift in channel model, new commercial roles, integration into buyers' procurement systems, run on a longer horizon and depend heavily on whether the operating model and governance can support them. Boards that expect revenue before they have rebuilt visibility usually conclude the transformation has failed when in fact it was sequenced backwards.

SOURCES

OECD, OECD Economic Surveys: Netherlands 2025. International Monetary Fund, 2025 Article IV Consultation, Kingdom of the Netherlands and 2026 Article IV concluding statement. Statistics Netherlands (CBS), retail turnover releases, 2025. European Commission, VAT in the Digital Age package and Digital Decade monitoring. Eurostat, enterprise digitalisation statistics. United States International Trade Administration, Netherlands Country Commercial Guide. World Bank, Logistics Performance Index. Figures are vintage-sensitive and should be checked against the current edition of each source before republication.

© Tretiakov Consulting. This insight is provided for general information and does not constitute legal, tax or investment advice.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.