Transaction Advisory in the Netherlands | Dutch Holding Structures

A Dutch BV at the top of a cross-border group is one of the most familiar sights in European M&A. That familiarity is also where the trouble starts. Transaction advisory in the Netherlands too often begins with the assumption that the holding layer is settled territory, efficient, well-trodden and fiscally optimised, and that the real work lies further down. In practice the opposite is closer to the truth. A BV holding entity can look impeccable in the corporate organogram while obscuring intercompany dependencies, management substance, governance gaps and the operating reality of the business beneath it. The work of an advisor is to see through it.

Why Dutch Holding Structures Change the Transaction Advisory Logic

Dutch holding structures appear in private-equity-backed groups, family-owned international businesses and mid-market corporate structures with a regularity that has stopped attracting scrutiny. The participation exemption, as set out by the Belastingdienst, can shield qualifying dividends and capital gains from corporate tax at the holding level, and it remains a defensible reason to use a BV as the parent. The exemption is conditional, however. It requires a qualifying participation, it carves out non-qualifying investment participations, and its application in any given transaction is a question of fact, not assumption.

This is where Dutch holding company M&A starts to diverge from generic deal logic. The structure that proved efficient for holding a group of subsidiaries through a long ownership period is not necessarily the structure that supports an exit, a carve-out or a strategic acquisition. Holding-level accounts may consolidate, simplify or quietly disguise the cash generation, working capital pressure and management dependency of the operating subsidiaries. Buyers who run their financial diligence at holding level alone are reading a summary, not the business. Sellers who enter a process without stress-testing the holding layer underestimate how quickly a buyer's advisors will surface the gap.

The deeper risk in transaction advisory for Netherlands-based holding structures is not that tax efficiency is wrong. It is that tax efficiency is mistaken for transaction readiness. The two are different things, and the difference becomes commercial the moment heads of terms are signed. This is also why our advisory work in the Netherlands starts with the holding layer rather than around it.

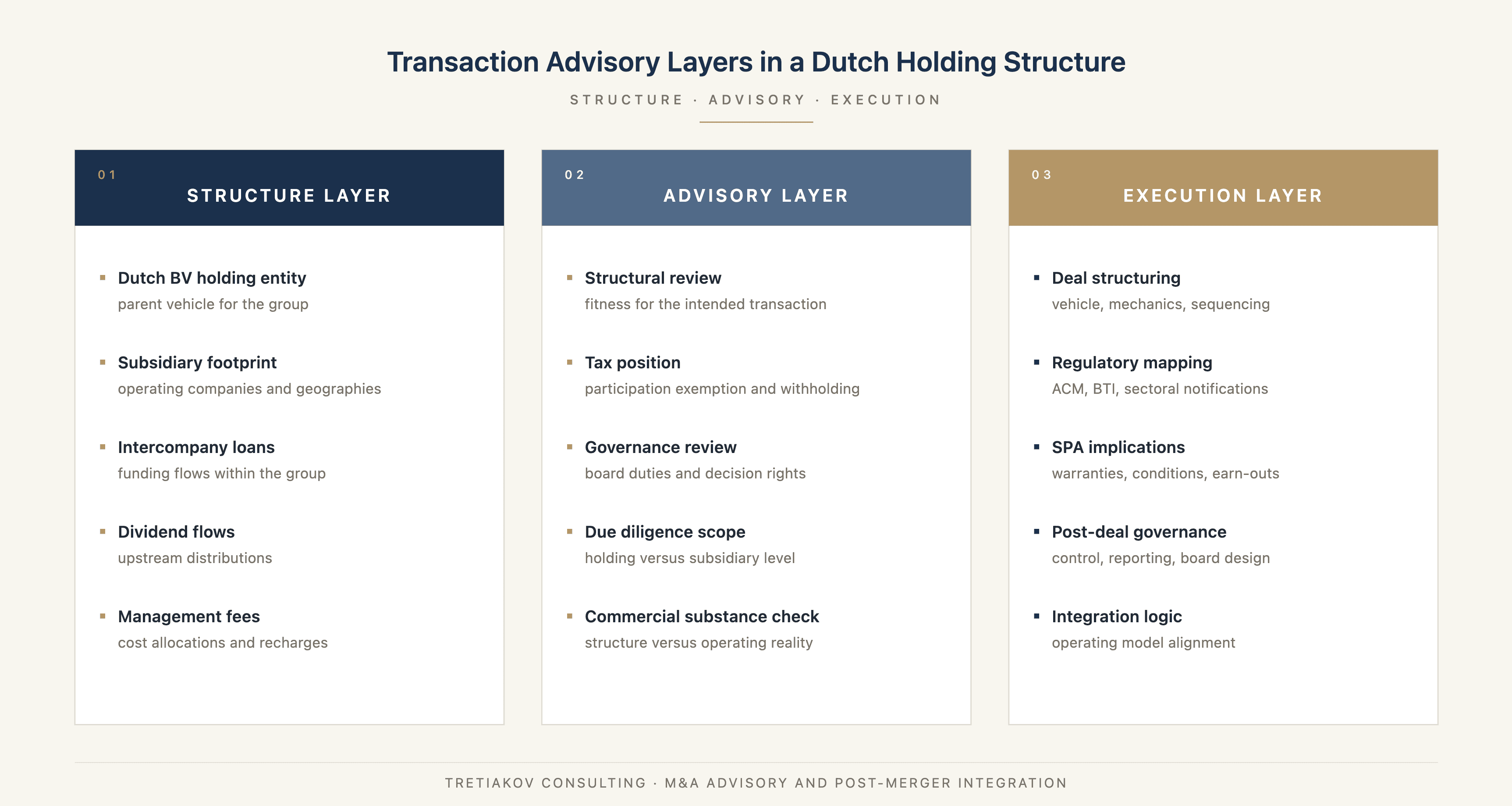

Transaction Advisory in the Netherlands: What the Structural Review Must Cover

A rigorous structural review tests the holding layer against the actual deal objective. Tax efficiency is one input, not the conclusion. Where the transaction is an exit, the review asks whether the structure facilitates a clean sale, an earn-out, a roll-over or a partial divestment without triggering substance disputes or unexpected consequences on intercompany flows. Where the transaction is an acquisition, it asks whether the Dutch entity is the appropriate vehicle to hold the target, or whether the existing footprint forces a structural compromise that will need to be unwound later. Acquisition advisory in the Netherlands that does not test the holding layer at this stage is incomplete.

Governance sits inside the same review. The Wet bestuur en toezicht rechtspersonen, which amended Book 2 of the Dutch Civil Code with effect from January 2023, sharpened the rules on director duties, conflict of interest and supervisory arrangements across Dutch legal persons including the BV. None of this is exotic. The questions it forces are practical. Who has decision rights at signing. Whose signature binds the entity. Where conflicts of interest sit. How the board is protected when those conflicts are unavoidable in the transaction itself.

Regulatory mapping belongs in the same exercise. Concentrations that meet the statutory turnover thresholds under the Mededingingswet require notification to the Netherlands Authority for Consumers and Markets with a standstill obligation pending clearance, and that regime is itself moving. The ACM has signalled an expansion of its powers over below-threshold transactions, which means timing assumptions made today on a routine deal may no longer hold by signing. Foreign investment screening is the other moving regime. Where the target sits in a vital sector or is active in sensitive technology, the Wet veiligheidstoets investeringen, fusies en overnames, administered by the Bureau Toetsing Investeringen, may impose a separate mandatory notification with its own standstill. Deal structuring in the Netherlands that leaves these regimes until after heads of terms has, in practice, already lost time.

Legal and tax counsel cannot solve this gap by working in parallel without integration. They optimise their respective scopes. The advisory layer that connects them is where structure becomes a commercial question.

Due Diligence on Dutch Holding Entities: Where Transaction Risk Is Hidden

Due diligence at holding level is not the same as understanding the business. A Dutch BV holding entity may have a director, a registered address, a set of consolidated accounts and a clean audit trail, and still tell a buyer almost nothing about how value is created in the subsidiaries beneath it.

This is where Dutch BV holding structures in M&A transactions hide the harder questions. Intercompany loans funded at the holding level can carry interest rates that look defensible in isolation but breach arm's length tests once the wider group context is applied. Management fees charged from the holding to operating companies can flatter holding-level profits and starve subsidiaries of disclosed margin. Cost allocations, guarantees and related-party transactions can shift economic substance in ways that are invisible to a balance-sheet reader and very visible to a transfer pricing inspector.

The OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations, in their consolidated 2022 edition, remain the international reference point for arm's length analysis. They are not exotic, but their application to a Dutch holding entity in the middle of a transaction is rarely as tidy as the documentation suggests. Where the transfer pricing file dates from a different deal cycle, where intercompany agreements have not been refreshed since the last reorganisation, or where the operating reality has drifted from the contractual terms, the risk is borne by the buyer unless it is surfaced before signing. This is the territory of due diligence that goes beyond the financial statements.

M&A advisory for Dutch BV holding companies must therefore be vertical, not horizontal. The advisor reads through the holding layer to the subsidiary, and reads through the subsidiary to the actual operating dynamics. Consolidated accounts can confirm or conceal. They cannot replace the work.

A second layer of risk appears during carve-outs and partial exits where the Dutch holding entity sits above operational businesses that were never designed to function independently. Shared ERP environments, centralised procurement, undocumented pricing exceptions, founder-controlled commercial approvals and informal intercompany dependencies often surface only after confirmatory diligence has begun. At that point the issue is no longer structural elegance but operational separability. Buyers discover that financial reporting can be separated faster than decision-making authority, supplier relationships or customer-management processes.

This is why transaction advisory in the Netherlands increasingly requires operational diligence alongside legal and tax review. A holding structure may be technically compliant and fiscally efficient while still creating post-signing integration risk, stranded cost exposure or governance confusion between the holding entity and the operating subsidiaries beneath it. In practice, many transaction delays emerge not from the headline structure itself but from the gap between documented governance and the way the group actually operates day to day.

Where Independent Advisory Adds Value Beyond Legal and Tax Structuring

The standard model of transaction advisory in the Netherlands assembles legal counsel, tax counsel and financial due diligence side by side. Each is well defined. Each protects its mandate. None of them is typically asked to test whether the transaction structure supports the strategic, operational and post-deal objectives of the principal, because that is not what they were retained to do.

This is the gap that an independent commercial advisor closes. The Dutch holding layer sits at the intersection of legal form, tax flow, management control and operating reality. When those four are not aligned, the failure mode is post-signing. Integration teams discover that decision rights live in the wrong entity, reporting lines cross legal boundaries that nobody flagged at diligence, governance documentation does not match how the group actually operates, or earn-out mechanics depend on subsidiary-level metrics that the holding structure cannot deliver cleanly.

Independent advisory of this kind belongs at the front of the process, before advisors are appointed and scopes are fixed. By the time legal and tax counsel are drafting documents, the advisory question has already been settled, often by default. Deal structuring and transaction support in the Netherlands is most useful when it sits upstream of the documentation, not parallel to it.

This is the connecting work that our M&A advisory and post-merger integration support is designed for. Where the transaction structure has consequences for the wider operating model, the same logic extends to post-deal operating model and integration questions. The function is the same: connect structure, due diligence, commercial logic and post-deal governance into a single coherent advisory layer.

Six Advisory Checkpoints for Transactions Involving a Dutch Holding Structure

The framework below is the working sequence we apply when a Dutch holding structure sits inside the transaction. It is a sequence, not a checklist. Each checkpoint informs the next, and each is most useful before the corresponding question has been answered by default.

Checkpoint | Core question | Why it matters |

|---|---|---|

1. Pre-process structural assessment | Is the current BV structure fit for the intended transaction type? | Prevents late-stage restructuring and avoidable resets at heads of terms |

2. Participation exemption and tax position | Are the participation exemption, withholding and intercompany flow assumptions valid for the intended transaction? | Protects deal economics and avoids false tax comfort |

3. Governance and compliance review | Are board decision rights, director duties and governance documentation aligned with the transaction? | Reduces transaction and post-signing governance risk |

4. Commercial and operating substance check | Does the holding structure reflect how value is actually created, managed and reported across the group? | Prevents structure-versus-substance mismatches in diligence and negotiation |

5. Due diligence scope definition | Is diligence focused only on the holding entity, or also on subsidiaries and intercompany flows? | Improves visibility of real business performance |

6. Post-deal integration and governance design | How will the Dutch holding layer interact with the post-deal group structure? | Links transaction design to execution reality |

From Structure to Substance

Dutch holding structures are familiar precisely because they work. The risk is that familiarity becomes a substitute for analysis. Transaction advisory in the Netherlands earns its place when it tests the holding layer against the actual transaction rather than against general practice, when it reads through the structure to the substance, when it integrates legal and tax thinking into a commercial view, and when it anticipates the regulatory and governance regimes that are now moving rather than static. Investors, acquirers, owners and corporate development teams preparing a deal with a Dutch holding component are welcome to discuss a transaction involving a Dutch holding structure with us at the point when structural choices can still be made.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.