Post-Merger Integration Consulting in France: Accelerating Value Capture Without Breaking the Business

Many French acquisitions that disappoint do so after the deal has been announced, when the integration plan proves too weak to convert the investment thesis into an operating result. The price has been agreed, the diligence findings have been summarised and the financing is in place. Yet 12 to 18 months later the board is still asking why the synergy run-rate is below plan, why the acquired business operates through parallel systems and informal decision rights, why the founder remains the only person who can unblock key customers, and why the works-council process has become a constraint rather than a planned part of the critical path.

This is where post-merger integration consulting in France becomes a distinct management discipline within the M&A lifecycle. Deal advisory and due diligence identify the value, the risks and the price. Integration has to convert those findings into governance, people decisions, systems, customer protection, operating routines and measurable run-rate value. The capabilities, the time horizons and the type of leadership required are different from those that close the transaction, and the cost of pretending otherwise is paid in the operating year that follows.

The French environment can protect value through continuity, social dialogue and consensus, but those qualities work commercially only when matched with clear governance, pre-close planning and disciplined synergy tracking. The modern standard in French M&A is not reckless speed. It is disciplined speed, anchored in pre-close planning, instrumented synergy tracking and a Day-365 operating model that protects culture while still capturing value on schedule.

The Underestimated Part of M&A: Why the Deal Is Not Won at Closing

Closing transfers ownership. It does not transfer value. The investment thesis remains a hypothesis until the integration proves it, and the proof depends on decisions that the deal team is rarely positioned to make: which customers to protect first, which contracts to renegotiate, which managers to keep, which systems to retire, and which parts of the acquired business to leave alone for now. Each is operational rather than transactional, and each compounds over the first year.

The market is making that distinction harder to ignore. According to Bain & Company's 2026 Global M&A Report, strategic deal value rose by roughly 40% in 2025 to around $4.9 trillion, while approximately 80% of executives surveyed expect to sustain or increase activity through 2026. At the same time, M&A as a share of corporate capital allocation has fallen to a 30-year low. More deals will close into organisations that have spent the past decade reallocating capital away from integration capability.

McKinsey's research repeatedly returns to the same fault line: in roughly 42% of transactions, due diligence does not produce an adequate roadmap for synergy capture, and the handover from deal team to operators leaves the most important questions unanswered. Practitioner literature has long quoted failure rates near 70%, a figure widely contested in scale but rarely in direction. Across failed-deal reviews, weak integration is one of the most consistent causes of value destruction, particularly where the deal thesis depends on synergy capture rather than passive ownership.

This is why mergers and acquisitions advisory in France increasingly treats post-merger integration consulting in France as a discipline separate from transaction execution. The deal team usually owns valuation, risk allocation and completion. The integration team has to own the operating result that makes the valuation defensible. When that handover is not designed and resourced in advance, the deal model quietly becomes fiction.

France's Integration Challenge: Continuity, Consensus and the Cost of Delay

France's reputation for slow integration is partly a misreading. What looks like slowness from the outside is often legitimate process: information and consultation of the works council, careful handling of long-tenured management, attention to regional relationships, and a preference for resolving structural questions before announcing them. Done well, this protects the parts of the business the acquirer is paying for, namely customer relationships, institutional knowledge and the social licence to operate. The French issue is therefore not a lack of discipline; it is that discipline has to be designed through consultation, governance and social sequencing rather than imposed as a post-close command structure.

The mechanism that creates real cost is different. The Comité Social et Économique does not have a veto over integration, but the integration calendar has a legally structured consultation sequence that must be built into the critical path. In companies with 50 or more employees, decisions affecting organisation, headcount or working conditions require information and consultation under the Code du travail, with statutory timelines that typically run for one month and can extend when an expert is appointed. Failure to consult carries criminal exposure under the délit d'entrave regime, with fines up to €37,500. Key decisions affecting organisation, headcount or working conditions therefore need to be sequenced around the consultation before they can be announced or implemented in the first 90 days.

The macroeconomic backdrop sharpens the price of mismanaging that sequence. According to the OECD Economic Outlook 2025 Issue 2, French GDP growth is projected at 0.8% in 2025 and 1.0% in 2026 and 2027. In a slow-growth environment, value leakage during integration is not absorbed by underlying market expansion; it is simply lost. France's deal market reflects the same tightening: BCG's 22nd Annual M&A Report (October 2025) shows announced deal value in France down by 29% year-on-year through Q3 2025, while global value rose by 10%. Buyers remain active in France but more selective, which means weak integration outcomes are punished more visibly.

France remains the leading European destination for foreign direct investment for the seventh consecutive year according to the EY Attractiveness Survey France 2026, with 852 project announcements in 2025. Deal flow continues, but integration capability does not always match it, and cross-border M&A advisory in France increasingly turns on whether the buyer's organisation can convert that activity into operating value within a politically and socially codified environment.

Why Slow PMI Is Expensive: The Economics of Integration Delay

Integration delay is rarely a single decision. It is a series of small deferrals, each defensible in isolation, that compound into a measurable loss. Cost synergies that should be banked in the first 18 months drift into year three, by which point benchmark research from BCG and McKinsey suggests buyers typically retain only around 50% of synergies announced at deal close. Revenue synergies erode faster: the same research places revenue synergy realisation in middle-market deals in the region of 25–35% against original plan. Once key customers and key managers have absorbed the uncertainty, the lost share rarely comes back at the original margin.

The productivity backdrop in France compounds this. The Banque de France has documented a labour productivity gap of approximately 8.5% against the pre-Covid trend, with apprenticeship effects and changes in workforce composition explaining a little over half of the shortfall. In an economy absorbing a productivity loss of that scale, an integration that runs two systems, two reporting cadences and two management committees in parallel for two years is not a neutral choice. It is an additional drag layered on a national one.

Table 1. The economics of integration delay

Delay area | What happens operationally | Economic effect |

|---|---|---|

Synergy capture deferred | Cost and revenue actions pushed beyond year one; early wins not banked | Benchmarks suggest buyers retain only ~50% of announced synergies; cost synergies that should reach 70–85% within 18 months erode (BCG/McKinsey) |

Key-person and talent attrition | Uncertainty drives the strongest people, and often founders, to leave first | Tacit knowledge and customer relationships are lost; revenue synergies, already only 25–35% realised in benchmark studies, become materially harder to reach |

Decision-rights vacuum | No empowered integration management office; choices wait for a consensus that does not form | Momentum decays into recurring meetings; the deal thesis quietly lapses into a status report |

Works-council process mishandled | CSE consultation rushed, sequenced wrongly or treated as administrative | Délit d'entrave exposure, fines up to €37,500, reputational damage and an adversarial transition |

Productivity drift in a slow economy | Combined entity operates parallel systems, reporting and governance | Compounds the 8.5% productivity gap documented by Banque de France against a 1% GDP backdrop (OECD) |

Capital tied up too long | Working capital optimisation, footprint consolidation and procurement scale benefits deferred | Return on invested capital deteriorates; the financing case for the next acquisition weakens |

Synergy realisation ranges are BCG and McKinsey middle-market benchmarks rather than France-specific measurements; the directional pattern is consistent across European mid-market deals.

The cumulative effect becomes visible at the 18-month point, when the board asks why cost synergies sit at 60% of plan, why three of the five named managers from due diligence have left, and why a customer the model treated as cross-sell-ready is in advanced discussions with a competitor.

What Has Changed: Why the Old 18-Month Integration Rhythm No Longer Fits

The 18-month integration calendar that served European mid-market M&A for most of the past two decades no longer fits because the economic tolerance for delayed value has narrowed. Capital is more selective, buyers are more cautious, and integration capability is increasingly part of the investment case rather than an operational afterthought. Acquirers that continue to manage integration on an 18-month rhythm risk losing value to buyers that can prove the deal thesis inside the first operating year.

Three structural shifts have driven the change. The cost of capital has disciplined allocation, raising the threshold for value capture from each deal. Private equity, with its hold-period economics, has compressed integration timelines that strategic acquirers historically allowed to extend. And AI-enabled diligence, integration-planning workflows and synergy-tracking systems make a faster pace genuinely possible without sacrificing analytical depth.

These shifts are reflected in current market signals. Goldman Sachs's 2026 M&A outlook describes a bullish backdrop with private equity now representing approximately 40% of M&A activity and a record 63 megadeals above $10 billion announced in 2025 according to LSEG data, while the CMS European M&A Outlook 2026 records that around 85% of European dealmakers expect to engage in M&A within the next 12 months. In France specifically, the integration calendar is already constrained by works-council consultation, FDI screening where relevant, founder transition and local governance translation, and the appropriate response is not to compress those constraints but to prepare them earlier. Corporate development advisory in France is increasingly asked to design integration capability before the next acquisition rather than after the current one is completed, and Day 1 readiness for acquisitions in France is no longer a checklist owned by IT and HR but a board-level question.

Due Diligence Is Written for the Investment Committee; PMI Must Be Written for Management

The accountability gap between deal teams and operators is the most consistent failure mode in M&A integration. Due diligence is a document written to support a decision: buy or not buy, at what price, on what terms. Its questions are necessarily financial, legal and risk-oriented, and its outputs are calibrated for an investment committee. On the day after closing, the operating team frequently inherits an answer to a question they did not ask.

McKinsey's research suggests early operating performance is a remarkably durable signal: in roughly 79% of cases, deals that outperformed their peers within the first 18 months were still doing so three years later. Underperformance in the early integration phase is rarely recovered, and the window in which the integration team has to convert diligence findings into management actions is narrow.

Table 2. Diligence questions versus integration questions

Due diligence asks | Post-merger integration must answer |

|---|---|

Is EBITDA sustainable and properly normalised? | Which operating decisions protect EBITDA in the first 12 months? |

What synergies does the model assume? | Who owns each synergy lever, on what timeline, and when does it hit the P&L? |

What are the ESG and regulatory risks? | Which findings become Day 100 workstreams with named accountability? |

What legal and contractual constraints apply? | How do those constraints sequence the critical path of integration decisions? |

What is the quality of management? | Which managers must be retained, on what arrangements, before Day 1? |

What is the customer base worth? | Which customer relationships are most exposed to competitor pressure during transition? |

Post-acquisition operating model integration in France must therefore answer what to combine first, what to leave alone, where the customer concentration risks live, which managers are critical for the first year, and how the new organisation will be governed in a way that satisfies both group reporting and the French management culture that the deal was, in part, paying to keep.

ESG due diligence in France M&A has become part of that translation rather than a separate workstream. The Council of the EU signed off in February 2026 on the Omnibus simplification of CSRD and CSDDD, narrowing CSRD scope to companies with more than 1,000 employees and more than €450 million of turnover, with member-state transposition still pending. ESG diligence cannot be calibrated against last year's framework; it needs to be calibrated against the boundary that will apply when the combined entity actually reports. The AMF Annual Report 2024 records 37 public tender offers supervised and 272 visas granted in 2024, confirming that public-market M&A in France remains an active and tightly supervised channel.

Modern PMI Tools: From Integration Meetings to Value Control

The difference between an integration that captures value and one that holds meetings about value is largely instrumental. The Integration Management Office, properly constituted, is the central instrument. Its purpose is not to coordinate workstreams in the abstract; it is to convert each line of the synergy model into a named owner, a baseline measurement, a defined timing, a tracked dependency and a weekly conversation with the P&L.

A modern PMI toolkit has a small number of essential components. A value tree decomposes the deal thesis into discrete synergy levers, each with an agreed definition. An owner is named for each lever, with authority to make trade-offs across functions rather than within them. A weekly run-rate report tracks both realised synergies, which have hit the P&L, and committed synergies, which have an executed action plan but have not yet flowed through to earnings. A decision-rights matrix removes ambiguity between group, country and business-unit authority. A customer and talent heatmap identifies where value is concentrated in specific relationships and specific people. A regulatory and ESG register tracks obligations that have a hard calendar, including CSE consultation milestones and CSRD reporting boundaries. Without these instruments, governance remains a structure on paper rather than a management system capable of protecting value.

Modern M&A integration services in France should therefore be judged less by the number of workstreams they coordinate and more by their ability to translate the deal thesis into owned, measured and finance-validated value levers. The governance benchmark is set by the Code AFEP-MEDEF, the reference corporate-governance code for listed French companies, operating on a comply-or-explain basis. Its principles function as a credibility benchmark for the boards of acquired companies whether or not they are listed, and integration designs that ignore this benchmark often need to be revisited once investor, board or stakeholder expectations become more formalised.

Our M&A advisory and post-merger integration work is organised around exactly these instruments, because synergy capture in French M&A deals is, in operational terms, a function of how cleanly each lever is owned, measured and converted into management decisions during the first year.

Family-Owned and Founder-Led Targets: Respecting Legacy Without Freezing the Business

The French mid-market is overwhelmingly family-influenced. Research published by EY, OpinionWay and FBN France indicates that approximately 71% of French companies are family-owned, including roughly 68% of PME, 73% of ETI and 60% of large groups. INSEE records 7,442 entreprises de taille intermédiaire in France in 2023, employing around 3.5 million people and generating around €377 billion of value added. The mid-market is the economic backbone, and a substantial share of M&A advisory for mid-market companies in France involves businesses where ownership, management and identity have been concentrated in one family or one founder for decades.

The integration risk in these targets is not cultural in the soft sense; it is structural. Decision rights are often undocumented because they did not need to be documented when the founder was in the room every day. Key customer relationships are anchored in personal history rather than account governance, and pricing decisions, supplier choices and credit terms have evolved through judgement rather than process. None of this is dysfunctional; it is the operating system that produced the value the acquirer is paying for. The question is how to formalise enough of it to make the business governable under new ownership without breaking what made the business worth buying.

The succession backdrop sharpens the urgency. Bpifrance Le Lab's research on family-business transmission found that approximately 47% of family-business owners aged 60 to 69, and roughly 36% of those over 70, have not formalised a succession plan, while 76% of family SMEs and ETI have no family council or charter. The practical transmission of a family business often takes up to ten years. A meaningful share of mid-market deals in France over the next decade will be succession-driven, and the integration question is not how to apply the group operating model; it is how to codify the founder's operating system before it walks out of the building.

Succession M&A advisory for family-owned companies in France works best when codification begins before signing. Three workstreams matter most: decision-rights translation, in which the founder participates in writing down who decides what, on what evidence, with what authority; relationship transfer, introducing next-level managers into customer, supplier and banking relationships on a timeline that allows trust to compound; and governance design, building a board, management committee and reporting cadence that match the new ownership's expectations without dismantling the informal mechanisms that still work. Governance in French owner-managed companies is rarely an off-the-shelf design; it is a translation between two operating systems, and the price of getting it wrong is paid in the second and third year of the integration, when the founder is gone and the institutional memory has not been transferred.

Cross-Border Buyers: Why France Requires Integration Translation, Not Just Integration Planning

For cross-border acquirers, the most expensive misconception is that the integration playbook that worked in Germany, the Netherlands, the United Kingdom or the United States can be applied in France with light translation. The formal stages may look familiar, but the operating mechanics are different, and the differences sit in the areas that determine first-year value capture.

Regulatory sequencing alone reshapes the integration calendar. The French Treasury's 2024 annual report on foreign investment control recorded 392 foreign-investment filings, an increase of approximately 27% on 2023, with around 54% of authorisations granted subject to conditions, up from 44% the year before, one of the highest conditionality rates in Europe. Cross-border M&A advisory for foreign investors in France must build the FDI screening calendar into the integration plan from the outset rather than treating it as a parallel legal workstream. Conditions imposed on authorisation frequently constrain integration choices in areas the buyer assumed were within full operational discretion.

Works-council process is the second sequencing constraint. The CSE consultation is not negotiable in companies with 50 or more employees, and the calendar attached to it determines what can be communicated, decided or executed in the first 90 days. Cross-border buyers that treat this as a paperwork exercise often discover too late that the sequence determines what can be implemented before Day 1, with consequences ranging from délit d'entrave exposure to reputational damage in a market that takes social dialogue seriously.

Governance translation is the third sequencing constraint, and arguably the most subtle. A group operating model that arrives as a fait accompli, without space for the French management team to engage with its logic, produces compliance rather than commitment. The same operating model, introduced with two weeks of structured discussion before adoption, typically produces both. The cost differential between those two outcomes is large and rarely modelled. Successful post-acquisition integration in France therefore turns less on familiar deal mechanics and more on translating governance, sequencing and communication into the local operating reality.

The macro-context still supports the deal logic. France remains a top European target, and entering the French marketthrough acquisition is, for many groups, the most credible path to scale. The challenge is not whether to enter; it is whether the integration capability matches the entry strategy. Acquiring a company in France as a foreign buyer is, increasingly, less a transaction question and more an operating-capability question.

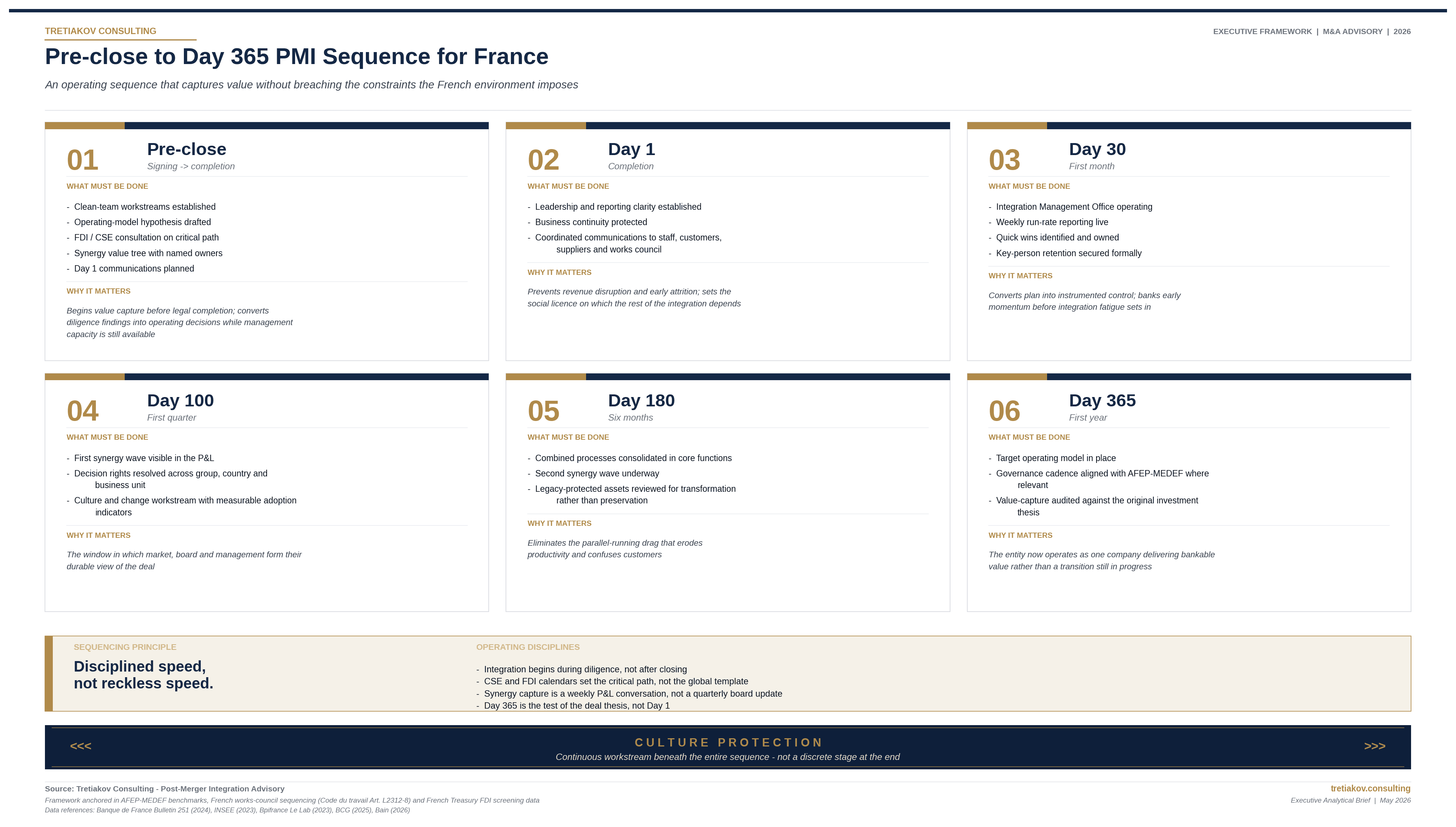

A Faster, Safer PMI Model for France: From Pre-Close to Day 365

Effective post-acquisition integration in France depends on an operating sequence that begins before signing and continues through the first operating year. The model below sets out that sequence without breaching the constraints the French environment imposes. Each phase has a defined set of actions and a clear test of whether the phase is complete, and culture protection runs as a continuous workstream beneath the entire sequence rather than as a discrete stage at the end.

Visual 1. Pre-close to Day 365 PMI sequence for France

The sequence is practical because it is built backwards from the board's first-year test: did the acquisition deliver the value the investment thesis promised, and is the combined business demonstrably more capable than the sum of its parts. If the answer at Day 365 is that the business is still in transition, the original deal model has already diverged from the operating reality. Redesigning the operating model and putting interim management in place to stabilise operations during the sequence are the two areas where capability gaps most often emerge, and both are areas where pre-close preparation determines whether the operating year proceeds on schedule.

What Better PMI Could Change for Companies and the French Economy

The quality of integration has consequences that extend beyond any single transaction. France runs a measurable productivity gap against its own pre-Covid trend and against several European peers, and the OECD's projections of 1% GDP growth in 2026 and 2027 leave little room for value to be lost in the second derivative of corporate performance. At scale, repeated integration underperformance contributes to the productivity problem French institutions are trying to address: resources are tied up, management attention is absorbed, and acquired companies fail to diffuse better systems and practices quickly enough.

The mid-market carries disproportionate weight in this calculation. INSEE's data on the 7,442 ETI in 2023 places this segment at the centre of French employment and value-added generation, and a meaningful share of those companies will change ownership over the next decade through succession or strategic sale. Whether those transitions produce stronger, better-governed businesses or weaker, fragmented ones is determined less by the price paid than by the integration that follows. Better PMI is, in aggregate, a competitiveness lever, not a deal-level optimisation.

For boards and investment committees, the implication is direct: integration capability is a strategic asset that deserves the same scrutiny as financing capability, the same investment as commercial capability, and the same governance as risk capability. Board and governance support at the start of an integration is materially less expensive than the remediation that follows when value has already leaked.

Outlook: What Will Change in PMI Over the Next Three Years

Five shifts are likely to define how post-merger integration in France develops between 2026 and 2029. None is a certainty, but the directional logic is consistent enough to plan around.

Integration is likely to begin earlier in the deal cycle. Pre-close planning, currently treated as best practice by sophisticated buyers, is likely to become a default expectation, particularly in cross-border and private-equity-led transactions where the cost of the 18-month calendar is most visible. Synergy tracking is likely to become more granular and more financial, with boards demanding realised value against committed value rather than activity status against milestones.

AI and data integration should be expected to move into the core of the integration toolkit rather than sitting alongside it. Diligence acceleration, synergy-model validation, customer-base analysis and process harmonisation are areas where AI-enabled tooling is increasingly being used to compress timelines and improve analytical depth in international transactions, and French acquirers and targets should be expected to adopt similar instruments at pace.

ESG integration is likely to continue evolving with the Omnibus simplification and member-state transposition of CSRD and CSDDD. The regulatory boundary will shift during the lifetime of integrations currently being planned, and designs that assume a static regulatory environment will need to be rebuilt. Cross-border activity in France is likely to remain selectively constrained: the Treasury's foreign-investment screening regime, with its rising conditionality rate, signals an enforcement environment that should be expected to continue shaping what foreign acquirers can do operationally after closing.

The acquirers most likely to outperform in this environment are those who treat integration capability as a strategic investment in its own right. Post-merger integration consulting in France is, in that sense, no longer a downstream service to deal-making. It is the discipline through which deal-making produces returns.

Conclusion: Disciplined Speed Is the New Standard for PMI in France

A French acquisition is often made or unmade in the year that follows signing, because that is when the investment thesis is converted into management decisions, customer stability, retained talent and measurable synergy run-rate. The acquirers who design for continuity, consensus and social process generally produce both faster and more durable value capture, while those who do not generally produce a long, expensive transition that is recorded on the balance sheet as an acquisition and on the management agenda as an unresolved problem.

Post-merger integration consulting in France is now the discipline through which deal-making converts into earnings. Pre-close planning, instrumented synergy tracking, governance design that respects French management culture, and a Day-365 operating model built backwards from the board's first-year question are the components that consistently distinguish integrations that work from integrations that drift. The acquirers building this capability now will be the ones converting the next wave of activity into measurable value.

Discuss how a pre-close to Day-365 integration model could protect value in your next French acquisition →Tretiakov Consulting — M&A advisory and post-merger integration

FAQ

What makes post-merger integration in France different from integration in other European markets?

The principal differences are structural rather than cultural. Article L2312-8 of the Code du travail imposes a sequenced information-and-consultation process with the CSE in any company of 50 employees or more, and the calendar attached to it determines what can be communicated, decided or executed in the first 90 days after a transaction. The French Treasury's foreign-investment screening regime adds a second sequencing constraint, with roughly 54% of authorisations granted subject to conditions in 2024. France's governance environment, anchored by the Code AFEP-MEDEF, also expects board-level engagement with long-term value creation and stakeholder considerations in a way that is more formalised than in several comparable jurisdictions.

When should integration planning begin, and who should own it?

Integration planning should begin during due diligence, not after closing. The handover from deal team to operating team is the most consistent failure point in M&A, and it can only be done cleanly if integration leadership is involved in the diligence findings as they emerge. Pre-close planning typically covers the operating-model hypothesis, the synergy value tree with named owners, the FDI and CSE calendars, the Day 1 communications sequence and retention arrangements for critical management. Ownership should sit with a dedicated integration lead reporting to the executive committee, supported by an Integration Management Office, rather than with the deal team that closed the transaction.

How does the CSE consultation affect the integration timeline in practice?

The CSE must be informed and consulted before decisions affecting organisation, headcount or working conditions, with a statutory consultation period that typically runs for one month and can extend when an expert is appointed. The consultation is advisory rather than a veto, but failure to consult carries criminal exposure with fines up to €37,500. Key integration decisions in companies with 50 or more employees cannot be announced or implemented until consultation is properly concluded. Well-run integrations sequence the CSE process onto the critical path from pre-close planning, rather than treating it as a workstream parallel to the operating decisions it actually governs.

How should buyers integrate a founder-led or family-owned business without losing what made it valuable?

The first task is to codify the founder's operating system, including decision rights, customer relationships and supplier arrangements, before the founder reduces involvement. Bpifrance Le Lab indicates that approximately 47% of family-business owners aged 60 to 69 and around 36% of those over 70 have not formalised a succession plan, and that 76% of family SMEs and ETI have no family council or charter, which means the codification work is rarely complete at signing. The integration should classify assets into legacy-protected, combine-now and transform categories, with explicit board-level decisions on each. Retention arrangements need to be in place before Day 1, and governance design should evolve from the existing informal mechanisms rather than replace them in a single step.

Do foreign acquirers need FDI clearance to acquire a French company, and how does it affect the integration?

Foreign acquirers require clearance under the French foreign-investment screening regime for transactions in sensitive sectors, including defence, dual-use technologies, energy, water, transport, public health, telecommunications, critical raw materials and certain digital infrastructure activities. The Treasury's 2024 report records 392 filings during the year, of which approximately 54% of authorisations were granted subject to conditions. The conditions frequently constrain integration choices in areas such as governance composition, sensitive-activity ringfencing, headquarters location and information-sharing with the foreign parent. Building the FDI calendar into the integration plan at pre-close is the single most reliable way to avoid post-close surprises.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.