Operating Model Redesign in the Netherlands for Trading Companies

The Dutch trading and distribution model was historically built on three quiet advantages: information asymmetry between manufacturer and buyer, predictable European trade flows through Rotterdam, and relationship density that protected mid-market accounts from outside competition. None of those advantages compound the way they once did. Margin headroom is narrower, large European distributors are consolidating regionally, manufacturers are running direct channels in selected categories, and B2B customers expect the responsiveness they meet as consumers. In that environment, operating model redesign in the Netherlands has become a P&L necessity rather than a strategic-planning exercise, a practical question of how to redesign a distribution operating model in the Netherlands before the next economic cycle, transaction or generational transition forces the issue.

Why Dutch Trading and Distribution Models Are Under Pressure

The most useful way to read margin compression in Dutch distribution is not as a pricing problem but as a transparency problem. For decades, the intermediary captured part of the margin precisely because the buyer could not easily see the manufacturer's price and the manufacturer could not easily see downstream behaviour. That gap has closed. B2B procurement teams now run line-item benchmarks, manufacturers monitor downstream pricing in near-real time, and mark-ups that once sat undisturbed are negotiated each quarter. Trading company restructuring in the Netherlands is, at its core, a response to that structural loss of asymmetry not a reaction to short-term price competition.

Manufacturer disintermediation is the second mechanic, and it is more selective than it is usually described. Large European manufacturers are not eliminating distributors as a category they are choosing categories - typically high-margin SKUs with predictable demand and direct-fit customers and serving those themselves, while leaving the operationally complex tail to the intermediary. The distributor inherits the lower-margin, higher-effort end of the assortment, which fundamentally changes the economics of the business it thought it was in.

The third pressure is service-level inflation. B2B customers now expect B2C-like transparency, real-time stock visibility, fast quotes and accurate delivery promises. Industrial complexity has not disappeared; the gap between what customers expect and what mid-market systems can deliver has widened. Meanwhile, larger pan-European distributors are acquiring regional players, widening assortment and lifting service standards squeezing Dutch mid-market businesses between price pressure above and service-cost inflation below.

These pressures sit on top of a less visible shift in Dutch trade flows. The Port of Rotterdam Authority's 2025 container year review describes a clear pattern of stronger imports, lagging exports and growing pressure on the container balance, against a backdrop of carrier-network changes and weakening European competitiveness. For distributors, the implication is operational: the inbound-flow assumptions baked into the existing operating model predictability of transit, balanced container availability, stable hinterland costs can no longer be treated as constants. That alone is sufficient reason for Dutch distribution transformation to move up the board's agenda.

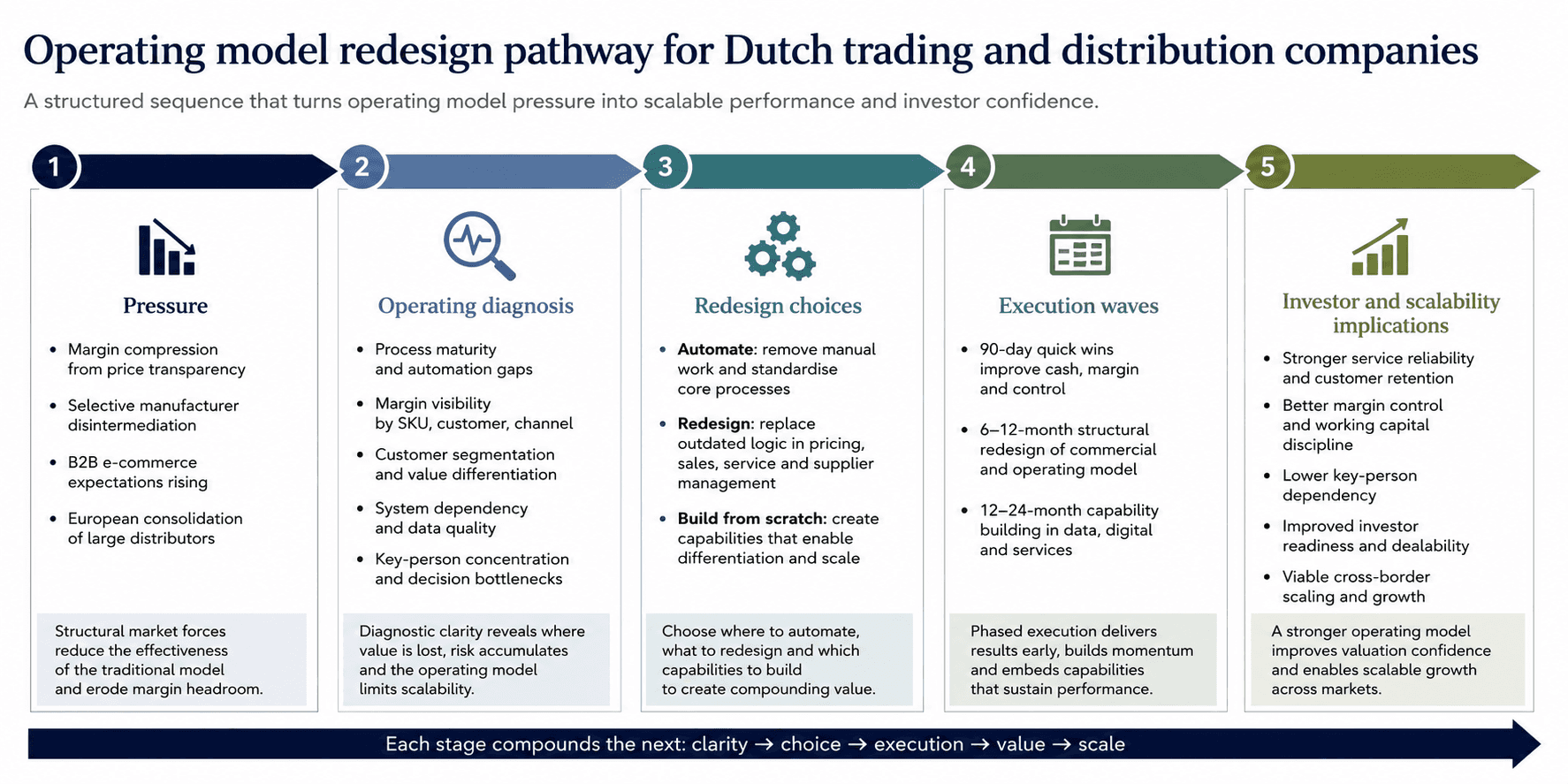

What Operating Model Redesign in the Netherlands Should Change

A useful diagnostic separates the operating model into three categories: what to automate, what to redesign, and what to build from scratch. Automation addresses work where human effort no longer creates strategic value. Redesign addresses logic that has expired. Build-from-scratch addresses capabilities that were never there.

Redesign area | What to automate, redesign or build | Business reason |

|---|---|---|

Order management and invoicing | Automate through EDI, API integration and workflow rules | Reduce manual effort, error rate and response time |

Warehouse operations and inventory planning | Automate WMS, demand sensing and reorder logic | Improve service reliability and working-capital discipline |

Sales model and pricing architecture | Redesign towards value-selling and segment-based margin guardrails | Protect margin under price transparency |

Customer service and supplier management | Redesign service tiers and supplier segmentation | Align service cost with customer value |

Data, digital channels and value-added services | Build analytics, B2B e-commerce and value-added service capability | Create differentiation beyond basic distribution |

The harder shift sits in the redesign column. Replacing cost-plus pricing with a segment-based margin architecture changes how the commercial team is organised, compensated and held accountable; it cannot be delivered as a technology project. The same applies to moving from a flat service promise to tiered service levels, which forces the business to decide explicitly which customers it will not serve at premium responsiveness. Most management teams find that conversation harder than any system implementation.

Build-from-scratch is where the largest value is typically left on the table. Margin visibility at SKU, customer and channel level is rarely available in mid-market Dutch distributors. Without it, every commercial decision is taken on weighted-average instinct and weighted-average instinct is precisely what the new market punishes. This is also where operating model maturity in Dutch trading companies is most visibly tested by external assessors. Credible business transformation and operating model redesign work treats this capability as the platform on which every other redesign sits, not as an analytics add-on.

The Dutch Context: Rotterdam, Schiphol, Labour Costs and Scale

Rotterdam remains a strategic asset for distributors with European reach, but the Port Authority's own commentary on container flows makes clear that the underlying supply-chain logic is shifting and operating models built on yesterday's flow assumptions are exposed. Air-freight-oriented distributors, high-value goods, perishables, electronics - retain an operating advantage through Schiphol, but that advantage rewards companies whose operating model is built to exploit it: customs orchestration, value-added warehousing close to the airport, time-definite delivery commitments. Geography alone does not pay for itself.

Labour costs are the most underestimated lever in the discussion. Eurostat's latest release on hourly labour costs places the Netherlands at €47.9 per hour for 2025 the third highest in the European Union after Luxembourg and Denmark, against an EU average of €34.9. For a distribution business, this is not a complaint to be lodged; it is a design constraint to be accepted. Manual order processing, paper-based warehouse workflows and Tier-1 customer service handled by people on every account are not absorbable on a €47.9 cost base. Automation in those workflows is a financial necessity, not an efficiency initiative — and this is what changes the economics of a distribution operating model in the Netherlands relative to peer European markets.

The digital readiness picture has two layers that should not be conflated. At country level, the EIB's 2025 Investment Survey for the Netherlands confirms that Dutch firms remain in the European front pack on digital and AI adoption, with high investment intentions overall. At SME level, the European Commission's Netherlands 2025 Digital Decade Country Report is more specific: smaller Dutch enterprises often lag in adopting key digital technologies, particularly AI, in part because innovation is fragmented and regionally driven. Mid-market distributors sit squarely in that SME band. The capability gap is not abstract it is the difference between what their large customers and competitors already deploy and what their own operating model can support.

International orientation is the final piece. Dutch trading companies are unusual in Europe in how routinely they already operate across borders. That makes them natural candidates for market entry and business expansion into adjacent geographies but only when the operating model itself can carry the additional scale, rather than being held together by founder attention and bespoke workarounds.

Why Operating Model Modernisation Matters for Valuation and Succession

The link between operating model maturity in Dutch trading companies and valuation is rarely captured by a single multiplier; it is a discount that accumulates quietly. Buyers and PE sponsors price for what they can verify. Manual processes, fragmented systems, key-person dependency, ambiguous unit economics and weak margin visibility are read as operational risk and priced accordingly. Operating model redesign for Dutch trading and distribution companies can support valuation by reducing each of those risks — improving the transparency of unit economics, lowering key-person dependency, narrowing the diligence findings list but it does not produce a deterministic increase in the EBITDA multiple. Multiple expansion depends on a wider set of conditions, including sector dynamics, customer concentration, working-capital quality, management depth and the growth narrative the buyer is willing to underwrite.

For PE-backed assets, the carve-out and post-integration sequence is its own discipline; the adjacent work is M&A advisory and post-merger integration, in which the operating-model question is separated from the deal mechanics but governed in parallel. For family-owned Dutch distributors approaching succession, the risk profile is different. An unmodernised operating model means the next-generation team or external buyer inherits a business whose continuity depends on the outgoing founder typically the most common single cause of failed transitions in this segment.

The strategic backdrop reinforces the urgency. The OECD's 2025 Economic Survey of the Netherlands observes that preserving Dutch trade competitiveness in conditions of global fragmentation now requires firms to strengthen supply-chain resilience, expand digitalisation in trade and operate in a more dynamic business environment. For owners considering a transaction, succession or external capital over the next two to three years, this turns Dutch distribution transformation from a multi-year programme into a pre-transaction priority and trading company restructuring in the Netherlands becomes a value-creation lever rather than a remedial one.

How to Redesign the Operating Model Without Disrupting Customer Service

Most management teams already know what needs to change. Their real constraint is execution capacity, not insight. Daily operations consume the bandwidth that transformation requires, and customer-continuity risk makes any visible disruption uncomfortable customers leave quickly and return slowly. Mid-market Netherlands-based distributors typically do not have an internal transformation office or programme-management function able to hold structural change in parallel with running the business.

The realistic sequencing runs in three waves. The first 90 days deliver quick wins: tariff fixes, pricing-floor enforcement, basic margin dashboards and the obvious automation in invoicing and order entry. Months 6 to 12 deliver structural change: pricing architecture, customer-tier service redesign, supplier segmentation and the substantive WMS or ERP work. Months 12 to 24 build the capabilities that did not previously exist — analytics, B2B e-commerce and value-added services. Each wave has to produce visible commercial output, otherwise the organisation loses confidence in the next one and the programme stalls in its second year.

The role of external advisory in transforming Dutch distribution and trading businesses is not primarily diagnostic. Most owners already know what is wrong. The advisor's job is to hold the structural logic of the redesign while management continues to run operations, and to maintain decision rhythm when internal capacity is stretched. In channel-based business and distribution models this often calls for operational involvement during transformation rather than a conventional report-and-leave engagement, because the trade-offs in the redesign column above only hold if someone is in the room when the operational choices are actually made.

Operating model redesign in the Netherlands is no longer a forward-looking topic for boards. The transparency of B2B markets, the labour-cost base, the changing role of Rotterdam in European supply chains and the consolidation pressure from larger pan-European distributors have moved faster than most mid-market operating models. Owners, CEOs and COOs considering a transaction, succession, private-equity entry or cross-border move in the next 24–36 months have a narrow window in which redesign produces both operational and valuation effect. Tretiakov Consulting works with owners and management teams on exactly that window - please contact Tretiakov Consulting to discuss operating model change.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.