Commercial Strategy for Dutch B2B Companies: Competing When the Trading-Hub Advantage Fades

A familiar pattern is showing up in Dutch B2B mid-market businesses, particularly in industrial distribution, specialty chemicals and technical components. Revenue is stable, the order book looks healthy, but gross margin has been thinning year after year. Sales directors describe it as a tougher market. Owners describe it as cyclical. Neither description is wrong, and neither is sufficient.

What is happening underneath is structural. The commercial strategy for Dutch B2B companies that worked for two decades, built around geographic proximity, dense distributor networks and relationship-priced contracts, is no longer matched to how procurement decisions are now made. German engineering depth, Eastern European cost positioning and digital B2B platforms have not arrived gradually. They have arrived together, and they compound. This article describes what is breaking inside the Dutch B2B commercial model, why the usual fixes do not hold, and how to sequence a redesign that survives a buyer's diligence.

Why the Dutch Trading-Hub Advantage Is Eroding

The Netherlands has been a European trade hub for far longer than its current B2B leadership generation has been in business. CBS in Dutch Trade in Facts and Figures 2025 continues to show that a substantial share of Dutch goods exports moves in re-export form to neighbouring EU markets, with Germany, Belgium and France dominating partner geography. The OECD Economic Survey of the Netherlands published in July 2025 reinforces the same picture from a competitiveness angle, but it also draws attention to a more uncomfortable structural reality. Productivity per hour worked has lagged peer economies for years, and the country remains exposed to trade fragmentation. The broader commercial environment in the Netherlands is changing faster than the operating models inside most mid-market businesses.

For the Dutch B2B mid-market, three sources of international competition facing Dutch companies are now operating at once. German competitors are pricing engineering depth into contracts that used to be won on local responsiveness. Eastern European producers offer a cost base that distributors increasingly find difficult to undercut through volume alone. Digital B2B platforms strip out the information asymmetry that previously protected relationship margins. None of these is a future threat. They are visible inside renewal cycles, in contract retentions and in deferred decisions on standard SKUs that customers are quietly testing elsewhere. The hub is intact statistically. The premium it once supported is not.

The Operating Model Underneath the Margin Erosion

Margin erosion in the Dutch B2B mid-market is rarely the consequence of a single market event. It is the consequence of a commercial operating model that was designed for a more forgiving environment and has not been refreshed. The IMF's 2025 Article IV Staff Report on the Netherlands documents wide firm-level productivity dispersion within sectors and a slowdown in capital deepening, both of which point at internal rather than external explanations. CPB Netherlands' 2025 work on dynamics, productivity and innovation goes further, showing a weakening of creative destruction since 2008 and innovation concentrating in larger and older incumbents. Translated into operating terms, the Dutch mid-market has not been continuously refreshed by competitive entry, and many companies are still running the commercial structures they built in 2010.

Three patterns are typical. Sales coverage is organised by geography rather than by customer value, which means an account manager gives the same hours to a sixty-thousand-euro customer as to a two-million-euro customer. CRM is treated as reporting infrastructure rather than as a commercial management system, so pricing, mix and contract leakage are invisible until the year-end review. Pricing decisions sit at the discretion of individual sales representatives, with no discount governance and no analytical layer to test what the customer would actually have paid.

This is where execution friction becomes commercially expensive. Even when ownership recognises the problem, account managers with twenty-year client relationships are simultaneously the largest commercial asset and the largest dependency. Diagnosing the underlying causes of revenue stagnation cannot be done from a quarterly P&L. It requires customer-level economics, and most Dutch B2B mid-market companies do not yet have that visibility. Sales organisation redesign in the Dutch mid-market is rarely a failure of will. It is a failure of measurement.

Four Strategic Options and Their Execution Realities

Boards facing this situation tend to discuss the same four strategic options. Each carries an execution reality that determines whether it will produce margin or simply reorganise the problem. This is where competitive strategy in the Netherlands separates from competitive ambition.

The first is value-added service development, meaning technical advisory, customised logistics and supply chain integration. This is the most credible response to German rivals, but it requires a sales profile and an engineering function the company often does not yet have. Hiring it externally takes eighteen to twenty-four months before it stabilises, and during that period legacy account managers see the new function as a threat.

The second is customer segment specialisation. Consultants prefer it and shareholders most resist it. It means choosing the customer base on which the company can defensibly earn margin and deliberately stepping back from the unprofitable tail. Most founder-led Dutch B2B companies do not execute this because revenue concentration unsettles banks and family stakeholders, even when contribution margin would improve.

The third is geographic expansion using the Dutch logistics advantage. This is widely available in theory and rarely well executed. Selling into Germany or the Nordics through distributor partnerships repeats the same intermediated model that is failing at home. Direct local presence is what generates margin abroad, and that requires a different cost commitment than the export-from-Rotterdam template assumes.

The fourth is digital commercial transformation, meaning e-commerce, configurators and pricing engines. Digital does not complement the existing sales force, it competes with it internally. Without channel governance, sales representatives undercut the platform to protect their commission, and the digital channel becomes a discount route rather than a margin route. This is the failure mode behind almost every public case study of how Dutch mid-market B2B companies compete with German and Eastern European rivals.

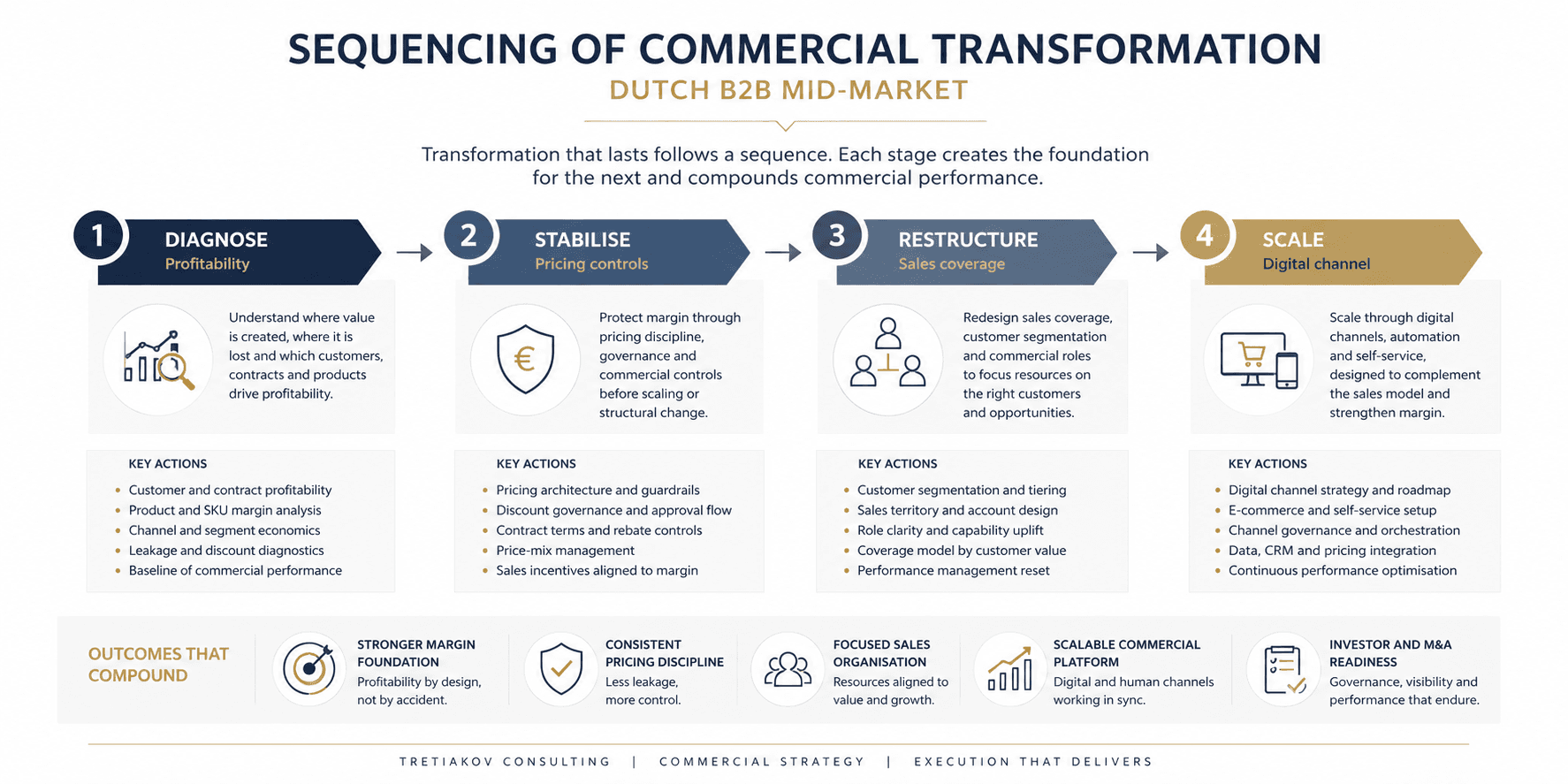

The sequence in which these options are pursued matters more than the options themselves. The framework below has been useful as a board-level anchor.

Each stage carries a typical failure mode if skipped. Diagnose skipped: option selection becomes intuition-driven. Stabilise skipped: margin leaks through unmanaged discounts even after redesign. Restructure skipped: digital tooling is built on top of an unreformed sales organisation. Scale skipped: the company performs the work without converting it into commercial capacity. Companies that announce Stage 4 ambitions while still operating at Stage 1 governance are not transforming, they are accelerating.

Building the Commercial Strategy for Dutch B2B Companies: A Diagnostic Framework

Before choosing among those options, leadership teams need a diagnostic. A commercial strategy for Dutch B2B companies that skips diagnosis selects options intuitively, and intuition in this environment selects the wrong sequence. Three axes of assessment matter most.

The first is customer profitability concentration. In a typical Dutch B2B mid-market portfolio, a minority of customers generates more than the full reported EBITDA, with the remainder subsidised at contribution level. Until finance can produce this view by customer and by contract, every other discussion is premature.

The second is pricing autonomy. The question is not who formally approves discounts. The question is who actually does, and whether that decision is supported by data on what comparable customers pay. In most cases, discount decisions are taken inside sales representatives' inboxes rather than inside pricing committees.

The third is channel readiness. Adding a digital channel to an unreformed sales organisation is the single most common failure mode in commercial transformation in the Netherlands. Channel governance must precede channel launch.

The diagnostic below has been useful in board-level conversations.

Dimension | Stage 1 — Legacy | Stage 2 — Transitional | Stage 3 — Restructured |

|---|---|---|---|

Customer profitability visibility | Gross margin only, no per-customer view | Customer-level GM tracked, EBITDA contribution unclear | Full contribution margin by customer and by contract |

Pricing governance | Rep-level discretion, no discount approval flow | Discount thresholds defined, weak enforcement | Pricing committee with analytics-supported approvals |

Sales organisation logic | Geographic territories | Hybrid (territory plus key accounts) | Coverage based on customer value tier |

Channel architecture | Direct sales only | Digital channel added, conflicts unresolved | Channel mix governed, cannibalisation managed |

CRM role | Reporting tool | Pipeline management | Commercial management system (price, margin, mix) |

The diagnostic is not a maturity scoring exercise. It is a sequencing test. Most companies discover, uncomfortably, that they are operating across two stages at once. Pricing governance is at Stage 1, while the leadership team is pitching Stage 3 digital ambitions to the board. That misalignment is the proximate cause of failed transformation programmes, and it is the reason a serious commercial transformation programme begins with diagnosis rather than with channel investment.

Governance, Pricing Discipline and the M&A Lens

Pricing discipline is not a sales topic. It is a governance topic, and the Dutch B2B mid-market is materially behind on this. De Nederlandsche Bank's Financial Stability Report and Autumn Projections published towards the end of 2025 are consistent on one point. Dutch corporates retain a competitive edge on price, quality and innovation, but that edge is under pressure from low productivity growth and rising export prices, requiring targeted structural investment. At firm level this translates into a board-level pricing function, a CFO who approves above-threshold discounts on contract-level profitability evidence, and a contracts review process that closes leakage from automatic renewals. A competitive strategy in the Netherlands that ignores this link delivers slideware, not margin.

This is also the lens through which strategic and private equity buyers now read the Dutch B2B mid-market. A founder-led commercial model with key-person dependency, geographic sales organisation and rep-level pricing autonomy is not a defensible asset, irrespective of headline EBITDA. The B2B growth strategy in the Netherlands that a company tells itself it is following is interrogated against contract data, churn cohorts and pricing dispersion. Where evidence is thin, valuation is discounted.

The link between governance and execution becomes practical here. Pricing discipline for Dutch B2B companies under procurement pressure cannot be built on top of fragmented systems. Operating model redesign of the sales, pricing and contract functions usually precedes meaningful digital investment, not the other way around. The companies that survive the next consolidation cycle will be the ones that did this work before a buyer demanded it.

Conclusion

The next three to five years will sort the Dutch B2B mid-market into two groups. The first will redesign their commercial model deliberately and on their own terms, accepting that part of the revenue base is structurally unprofitable and reorganising sales coverage, pricing governance and channel architecture accordingly. The second will defer, will continue to attribute margin erosion to a difficult market, and will eventually be repriced by either procurement professionalisation or a buyer's due diligence team. The international competition facing Dutch companies will not soften, and the commercial transformation in the Netherlands that buyers reward will increasingly be the one that has already been delivered, not the one that has been announced.

A commercial strategy for Dutch B2B companies built on diagnosis first, governance second and channel last is harder, slower and less photogenic than a digital transformation announcement. It is also the only sequence that produces a defensible margin position, and the only B2B growth strategy in the Netherlands that survives serious diligence. The trading-hub advantage will not return. What replaces it is an internal capability question, and the answer is built one pricing decision, one contract and one customer cohort at a time.

Tretiakov Consulting works with Dutch B2B leadership teams on commercial diagnostics, pricing redesign and sales organisation realignment. To discuss your specific commercial position, request a commercial diagnostic review.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.