Investing in Uzbekistan: Practical Realities for Foreign Companies

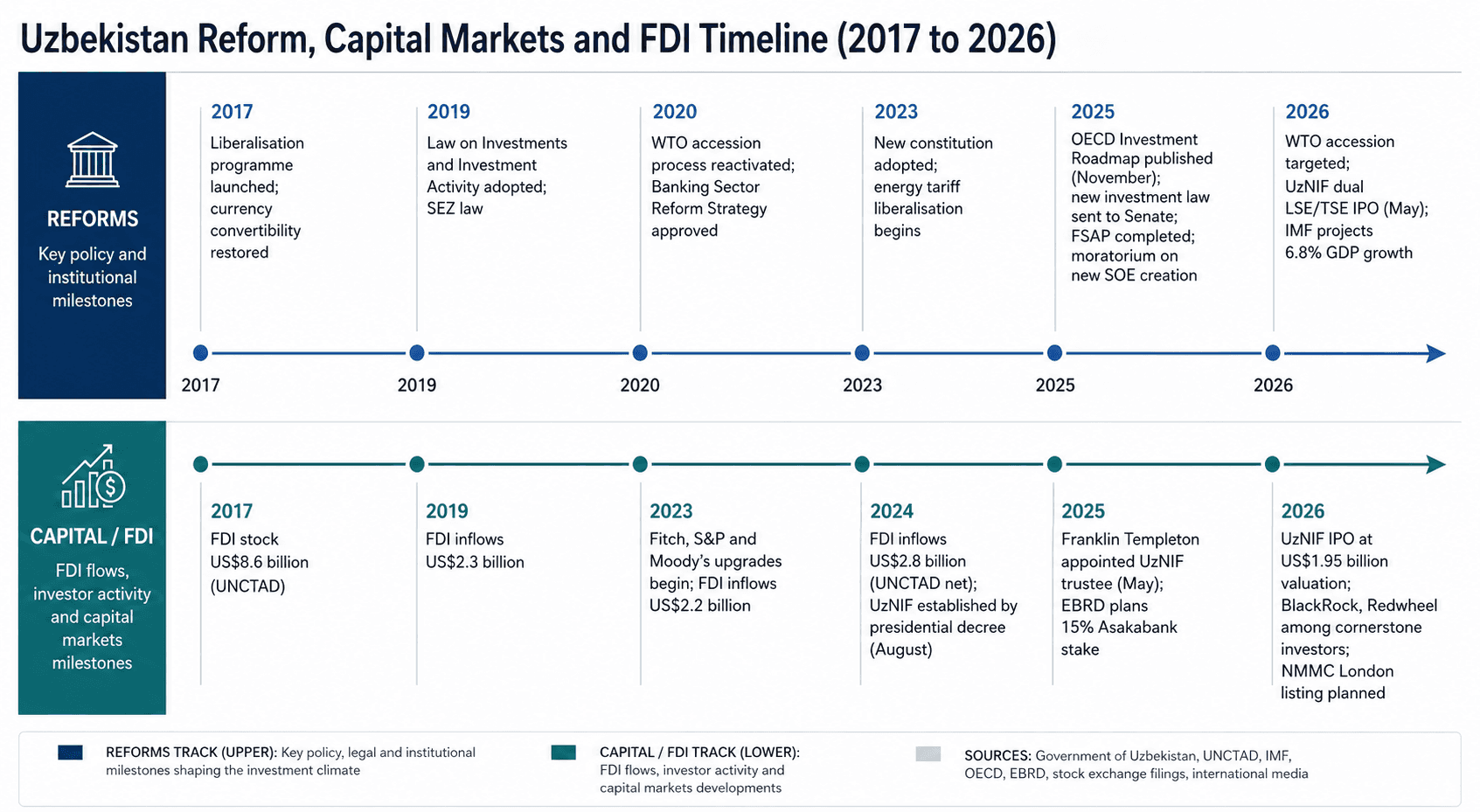

Investing in Uzbekistan is no longer a conversation about potential. The economy demonstrated remarkable strength in 2025, with real GDP growth reaching 7.7%, driven by robust consumption and investment, while the unemployment rate declined by 0.7 percentage points to 4.8%. Supported by ongoing reforms, sustained investment, buoyant remittances and higher gold prices, real GDP growth is projected to remain resilient at 6.8% in 2026. Capital inflows are accelerating, credit ratings are moving upward and the country is approaching WTO accession after a process that began in 1994. For foreign companies evaluating Central Asian markets, the question has shifted from whether Uzbekistan warrants attention to how a firm should structure its engagement given the gap between policy ambition and operational maturity on the ground.

This article examines the practical realities behind the reform narrative. It is written for decision-makers who need to understand not only why the macroeconomic picture is compelling, but where the operating frictions lie, what institutional risks remain underpriced and how to structure an entry decision that accounts for both.

Why Foreign Investment in Uzbekistan Is Accelerating

The investment case rests on a convergence of structural advantages that few markets in the region can match. Uzbekistan has a population of approximately 38.9 million, the largest in Central Asia, with steady demographic expansion that strengthens the long-term consumption base. Growth in 2025 was broad-based, with services and construction expanding the fastest.

Capital markets have responded accordingly. Headline CPI inflation declined to 7.3% year-on-year at end-2025, from 9.8% a year earlier, reflecting fading effects of the May 2024 energy price increases, a 6.9% appreciation of the sum against the US dollar and an appropriately tight monetary policy stance. The current account deficit narrowed to 3.9% of GDP, as strong commodity and non-commodity exports and remittance inflows outpaced imports, while international reserves remained ample at around 13 months of imports. The fiscal deficit fell to 2.1% of GDP, below the government's 3% target.

International credit reassessment reinforces this trajectory. Fitch and S&P both upgraded Uzbekistan to BB in 2024, while Moody's shifted to a positive outlook. UzNIF was established in August 2024. The Fund, which includes 13 strategic companies, is tasked with increasing the market value of the assets under its management, reforming them and attracting international institutional investors. In May 2026, this vehicle will deliver the first-ever international equity offering from Uzbekistan through a dual listing on the London and Tashkent stock exchanges.

These are material indicators of improved macroeconomic management. However, they describe the economy's direction of travel rather than the conditions a foreign company encounters when registering an entity, negotiating a supply agreement, recruiting local management or enforcing a contract. That distinction is where advisory value lies.

The Operating Environment: Where Reform Meets Institutional Reality

Foreign companies entering Uzbekistan encounter an economy in active transition. The pace of that transition itself introduces specific operational risks that standard country-risk frameworks tend to underweight.

Regulatory velocity creates compliance exposure. In only five years, the country has completely restructured its legal framework on investment, adopting the Law on Investment and Investment Activity of 2019, the Law on Public-Private Partnerships and the Law on Special Economic Zones, among others. While only recently adopted, all these instruments have already been subject to significant revisions, including to comply with WTO requirements, with a new draft Law on Investment and Investment Activities under preparation. The OECD's 2025 Roadmap for Sustainable Investment Policy Reforms in Uzbekistan, approved in November 2025 following discussion with Uzbekistan's Deputy Prime Minister at the OECD Investment Committee, is direct in its assessment: the modalities under which reforms are implemented and the quick pace at which they are put in place can give rise to concerns. For firms structuring long-term investments, this means that the legal framework governing an entry decision today may look materially different within 18 months. Firms that invest in sustained board-level advisory and governance oversight are better positioned to navigate this regulatory environment than those relying on point-in-time legal due diligence.

State-owned enterprises remain the dominant economic force. According to the U.S. Department of State's 2025 Investment Climate Statement, there are 541 active SOEs in Uzbekistan with a state share of 20% or more as of March 2025. The 10 largest SOEs contribute about 30% of total state budget revenues. The World Bank's broader count puts the figure at approximately 2,000 state-owned enterprises with total revenues equal to roughly 30% of GDP, most operating in competitive sectors. State-owned banks also hold around 60% of banking assets, which limits competition by crowding out private businesses.

This is not a matter of legacy structures awaiting dismantlement. SOEs retain preferential treatment in terms of access to land, financing and investment incentives that distort market entry for private firms. Around 900 SOEs enjoy tax and duty subsidies. For foreign companies evaluating independent market positioning, this competitive asymmetry represents a structural consideration that persists regardless of sector-specific incentive packages.

The banking system constrains private-sector financing. As of March 2025, 36 commercial banks operated in Uzbekistan: nine fully state-owned, 15 partially state-owned and 12 private, including seven with foreign capital. The declared goal of the government is to reduce the state's share of the sector to 40%, but as of February 2025, only two out of a planned six state-owned bank privatisations had been completed. The IMF noted that the policy rate has been held at 14% since March 2025. For foreign companies requiring local credit facilities or evaluating domestic acquisition targets, the cost and availability of finance remain materially constrained.

WTO accession is close but not yet concluded. At the 12th meeting of the Working Party on 9 March 2026, Uzbekistan's Deputy Prime Minister said his country is committed to bringing the accession process to a successful conclusion this year. To date, 30 agreements have been deposited with the WTO Secretariat, including five since the last Working Party meeting, with Ecuador, the European Union, Paraguay, the Russian Federation and Uruguay. Uzbekistan has completed bilateral market-access negotiations with 33 of its 34 members, with only Taiwan remaining. For firms weighing market entry and business expansion, WTO membership would anchor regulatory reforms within an enforceable international framework and reduce the risk of arbitrary tariff or regulatory changes. But the timeline should not be assumed as a basis for near-term contractual structures, since final accession depends on completing remaining multilateral commitments and parliamentary ratifications.

How Foreign Companies Should Structure an Entry Decision

Uzbekistan rewards structured, well-informed market entries and penalises opportunistic ones. Any firm committing capital should address four operational dimensions simultaneously.

Entry mode and local partner logic

In certain sectors, SOEs retain proprietary access to commodities, infrastructure, utilities and financial resources. Independent entry is legally permitted in most sectors, but the operating landscape strongly favours partnerships with established local groups who bring regulatory navigation, procurement access and workforce networks. The choice between wholly-owned subsidiary, joint venture and contractual partnership should be driven by sector-specific competitive dynamics rather than by a generic preference for ownership control.

Regulatory and licensing pathway

Foreign ownership of airlines, railways and long-distance telecommunication networks requires special government permission. By law, foreign nationals cannot obtain a licence or tax permit for individual entrepreneurship in Uzbekistan. Local companies with at least 15% foreign ownership can qualify as having a foreign investment. The SEZ law requires that at least 90% of employees of a zone participant should consist of Uzbek nationals. Firms should map the full regulatory pathway, including sector-specific licensing, minimum charter capital requirements and employment localisation rules, before committing to a corporate structure. This mapping exercise benefits significantly from structured operational due diligence rather than from reliance on framework legislation alone.

Privatisation exposure and SOE procurement risk

The privatisation programme is entering a decisive phase. The government of Uzbekistan will sell a 30% stake in UzNIF through initial public offerings on the London and Tashkent stock exchanges in May, marking the first time an Uzbek state-backed entity has tapped global capital markets. The offering is priced at $25 per GDR, each representing 64,700 shares, implying a market capitalisation of approximately $1.95 billion. Cornerstone investors including BlackRock and Franklin Resources have committed around $300 million.

In parallel, the government introduced a moratorium until 2030 on establishing new state-owned enterprises, except in cases related to defence and security. Shares of 12 key SOEs are scheduled for offering on both domestic and international stock exchanges between 2025 and 2028, including NMMC, Uzbekistan Airways, Uzbektelecom and the national electric grids.

For foreign firms, the implications are specific. Privatisation is creating new investable assets and partnership opportunities, but the state retains majority control in strategic entities. Procurement relationships with SOEs undergoing privatisation may shift as governance structures evolve. Firms already operating in markets where state entities are key clients or partners should actively monitor these transitions.

Operational readiness outside Tashkent

Currently 24 large SEZs and 742 small industrial zones with over four thousand registered companies operate in Uzbekistan, with combined industrial output exceeding $4 billion in 2023 and almost $1 billion in export earnings. Tax holiday duration in SEZs depends on the size of investment: three years for $3 to 5 million, five years for $5 to 15 million and ten years for over $15 million. These benefits are meaningful, but infrastructure quality, logistics connectivity and institutional capacity vary sharply beyond Tashkent. Firms planning regional operations should conduct site-specific assessments of infrastructure, labour market depth and municipal governance through a structured market assessment at the regional rather than national level.

Table: Market Entry Assessment Framework for Uzbekistan

Dimension | Current position (Q2 2026) | Practical implication for foreign firms |

|---|---|---|

Macroeconomic trajectory | GDP +7.7% in 2025; +6.8% projected 2026 (IMF); fiscal deficit 2.1% of GDP; CPI inflation declining to 7.3% | Strong demand environment with fiscal discipline improving, but the CBU policy rate at 14% reflects persistent inflationary pressures that increase operating and financing costs |

FDI regime | New investment law under preparation; OECD Roadmap published November 2025 with detailed reform recommendations | Improving in principle, but framework is in active revision and firms should not finalise structures based on current law alone without monitoring legislative trajectory |

SOE landscape | 541 entities with 20%+ state share; approximately 2,000 broader SOEs per World Bank; UzNIF IPO live; moratorium on new SOE creation until 2030 | SOE reform is genuine but gradual and competitive distortions in procurement, land access and financing persist; joint ventures remain the pragmatic default in many sectors |

Banking and financing | 36 banks (March 2025); 9 fully state-owned; state banks hold approximately 60% of assets; 2 of 6 planned privatisations completed | High interest rates, state bank dominance and limited private credit market constrain local financing; IFI co-financing or parent-company funding more reliable |

WTO accession | 30 bilateral deals deposited; 33 of 34 bilaterals concluded; accession targeted end-2026 | Once effective, will embed regulatory commitments in enforceable multilateral framework; until then, policy risk remains under-anchored |

Privatisation instruments | UzNIF dual LSE/TSE listing May 2026 at $1.95bn; 12 SOE IPOs/SPOs scheduled 2025 to 2028; Franklin Templeton as fund manager | Creates structured entry points for portfolio and strategic investors; minority stakes mean the state retains operational influence |

Conclusion

Investing in Uzbekistan today means engaging with an economy where the reform trajectory is credible, the demographic and growth fundamentals are strong and the institutional architecture is being rebuilt simultaneously across multiple fronts. The macroeconomic signals, including 7.7% growth, narrowing fiscal and current account deficits, sovereign rating upgrades and the first-ever international equity offering, describe a transition economy at a genuinely promising inflection point. But the practical realities of SOE dominance, regulatory churn, banking sector constraints and uneven institutional capacity outside Tashkent mean that the distance between policy intention and operating experience remains significant.

The firms that extract the most value from this market will be those that approach it with rigour and discipline, combining structured due diligence at the sector and regional level with realistic timelines for regulatory and institutional maturation and advisory support calibrated to the specific challenges of emerging-market operations in Central Asia. Uzbekistan rewards informed commitment and penalises assumptions.

For a confidential discussion about how your firm can position effectively in Uzbekistan or the wider Central Asian market, contact our team.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.