Restructuring and Turnaround in Switzerland: Board and Owner Guide

When a Swiss company moves into distress, the situation is governed by a tighter and more specific regime than most owners expect, and the practical room for manoeuvre closes faster than in most European jurisdictions. Restructuring and turnaround in Switzerland sit at the intersection of statutory duty, banking discipline and a business culture that punishes uncertainty quickly. The legal architecture has its own logic, but the commercial outcome is rarely decided by procedure. It is decided by how soon the board recognises the situation, how the principal bank receives the first conversation, and whether the leadership team retains credibility with the parties that determine cash, supply and revenue.

This article is written for boards, owners, lenders and investors dealing with a Swiss company under pressure. It is not a legal primer and does not constitute legal advice. The framework matters because it sets the deadlines that govern board action. Beyond that the outcome is operational. The companies that recover value treat Swiss distress as an integrated governance, cash and execution exercise rather than as a sequence of legal filings.

The Swiss restructuring context: legal framework as governance discipline

The revised Swiss company law regime, in force since 1 January 2023, made board duties in distressed and pre-distressed situations more explicit, particularly around liquidity monitoring, capital loss and over-indebtedness under Art. 725 ff. CO. The consolidated text of the Code of Obligations is published in the Swiss Federal Law Collection (Fedlex). The practical effect of the revision is that boards have less interpretive space than under the previous regime. Capital loss and illiquidity must be addressed earlier and more explicitly, and the reporting trail must reflect that.

The composition agreement (Nachlassvertrag) and the moratorium (Nachlassstundung) are the protective structures most relevant for distressed Swiss companies, set out in the Federal Act on Debt Enforcement and Bankruptcy (SchKG). A provisional moratorium can create a protected assessment window, often with a court-appointed commissioner, while a definitive moratorium involves formal supervision and a broader restructuring or composition process. In practice these are governance instruments, not legal shelters. Banks, suppliers and customers continue to make commercial decisions about the company during the moratorium based on what they observe operationally, and the protective layer disappears if execution does not match the plan. Sanierung and Nachlassstundung in Switzerland are tools that work only when the underlying business case works.

Art. 725 ff. CO and the board's duty to act

The revised provisions create a staged governance cascade. Art. 725 CO addresses liquidity monitoring and obliges the board to track solvency and act on indications of impending illiquidity. Art. 725a CO governs capital loss, the situation in which half of share capital and statutory reserves are no longer covered, and obliges the board to take corrective measures and, in many cases, to commission an interim audit. Art. 725b CO addresses over-indebtedness, in which liabilities exceed assets on a going-concern or liquidation basis. Where over-indebtedness exists, the board must notify the court unless statutory exceptions apply, such as sufficient creditor subordination or a credible restructuring path within the limits recognised by Swiss law.

The Revisionsstelle should be treated as part of the control and escalation architecture, not as an informal advisory resource. Where management's response to capital loss or over-indebtedness signals is inadequate, the auditor is expected to escalate, and that escalation is not a discretionary courtesy. For boards this changes the dynamic. The auditor is not waiting to be reassured. The auditor is documenting a position.

The most common failure point in Swiss company restructuring is the delay between the moment when liquidity stress is operationally visible and the moment the board formally recognises it. Owners who continue to focus on the operating business while the cash position deteriorates expose themselves to personal liability under Art. 754 CO and undermine every later restructuring lever, because the bank conversation then begins from a position of forced disclosure rather than controlled communication. This is the difference between turnaround management in Switzerland that retains optionality and a situation that has already narrowed to insolvency-adjacent outcomes.

Stabilisation in the first thirty days: cash, banks and counterparty confidence

The first month of any Swiss restructuring engagement determines whether the board controls the process or the process controls the board. The minimum analytical standard is a rolling thirteen-week cash forecast, reconciled to the bank account and updated weekly. It must include Swiss VAT, AHV and other social security obligations, which fall due on fixed dates and are treated severely when missed.

The conversation with the principal bank is the first external test. Swiss banks operate a relationship model in which the principal banker is the decision broker and the workout team is engaged early. Swiss banking practice in distressed situations generally rewards early, factual and structured communication rather than optimistic reassurance. Banks support a coherent plan with named milestones, defined cash discipline and a credible execution layer. They do not support narrative.

Counterparty confidence is the third axis of stabilisation. Swiss suppliers and customers respond to early signals. Payment delays, missed deliveries and unannounced changes in commercial terms travel through the market within days. Reputation during restructuring and turnaround in Switzerland is operational, not cosmetic. A controlled supplier strategy that prioritises the suppliers whose loss would interrupt revenue is more valuable than any press statement. The same applies to key customers, whose relationship typically deteriorates earlier than internal reporting suggests.

Workforce, suppliers and the operational restructuring plan

Swiss employment law gives employers more flexibility than several neighbouring European regimes, but workforce restructuring is not unconstrained. Mass dismissal rules apply once statutory thresholds are crossed: 10 dismissals in undertakings of 20 to 99 employees, 10 per cent in undertakings of 100 to 299 employees, and 30 dismissals in undertakings of 300 or more. The obligation to consult employees applies before the decision is final. A mandatory social plan may be triggered in larger organisations, notably where at least 30 employees are dismissed within 30 days in an undertaking employing 250 or more people. The mechanics are set out in the Code of Obligations and explained in labour law guidance published by SECO. Measures executed without observing these provisions create immediate legal exposure and damage internal cooperation at precisely the moment when execution capacity is most valuable.

Supplier concentration risk is a recurring weakness in Swiss mid-market companies. A small number of Swiss and German suppliers often hold disproportionate operational leverage, and their credit terms typically collapse on the first credible signal of distress. The same dynamic applies to specialised subcontractors, logistics providers and software vendors whose payment terms can shift from net thirty to advance payment within a week. Procurement risk and operational continuity are inseparable in Swiss company restructuring.

The operational restructuring plan is the substance against which lenders underwrite continued support. Cost reductions, working capital release, product portfolio rationalisation and operating model adjustments must be specific, measurable and sequenced. Generic statements about efficiency are not financeable. This is the territory of business transformation and operating model redesign, and Swiss distress situations require it in compressed form.

Governance and leadership: when internal management is no longer credible

There comes a point in many engagements when the existing CEO or CFO, regardless of capability in normal conditions, is no longer the right voice for the bank, the auditor and the principal customers. The reasons are rarely about competence. They are about credibility. Stakeholders need an independent signal that the situation is under new control. This is where turnaround management in Switzerland most often turns or stalls.

An interim chief restructuring officer or interim CEO provides that signal when the brief is correctly defined. The mandate must include executive authority over cash, clear decision rights with the board, and the seniority to engage banks and major counterparties directly. This is where interim management and operational leadership can become more relevant than traditional advisory support, particularly where cash authority, stakeholder communication and execution discipline need to sit in one mandate. Governance and execution in Swiss restructuring situations frequently require this combined profile rather than the parallel structure of separate advisors.

Board composition matters in parallel. The OECD Principles of Corporate Governance frame board responsibilities in distressed contexts as a strengthened obligation of oversight and informed decision-making. In Swiss practice this usually requires either a strengthened board or a restructuring committee with defined authority over cash, communication and disposals. Where this layer is missing, decisions slow and credibility erodes faster than the operating business deteriorates, which is one of the reasons many Swiss boards in distress engage external board advisory and governance support at this stage. The auditor and the principal banker both register that erosion before internal management does.

A practical timeline for restructuring and turnaround in Switzerland

The sequence below reflects how restructuring and turnaround in Switzerland typically unfold when boards act in time. It is not prescriptive, but it is the shape that successful engagements share.

Phase | Duration | Board priorities | What stakeholders observe |

|---|---|---|---|

Diagnostic | Weeks 1 to 2 | Cash position, Art. 725 ff. CO trigger status, stakeholder map, covenant review | The board has commissioned a structured assessment |

Stabilisation | Weeks 3 to 4 | Bank standstill discussions, supplier prioritisation, communication plan, key-person retention | The principal banker and major suppliers are in regular structured contact |

Plan development | Months 2 to 3 | Operational measures defined and quantified, balance sheet options assessed, decision on protective moratorium | A financeable plan with milestones reaches the bank workout team |

Execution | Months 3 to 9 | Operational delivery against the plan, milestone reporting, rebuilding of counterparty trust | Cash performance tracks the forecast, suppliers normalise terms |

Exit | Months 9 to 18 | Stabilised performance, governance handover, interim leadership exit where appropriate | The company returns to standard credit conditions |

The provisional Nachlassstundung enters this timeline only where the cash and stakeholder position cannot be stabilised through direct negotiation. When required, it functions as a protective platform for execution rather than as an end in itself. The outcome that determines value recovery is operational, not procedural.

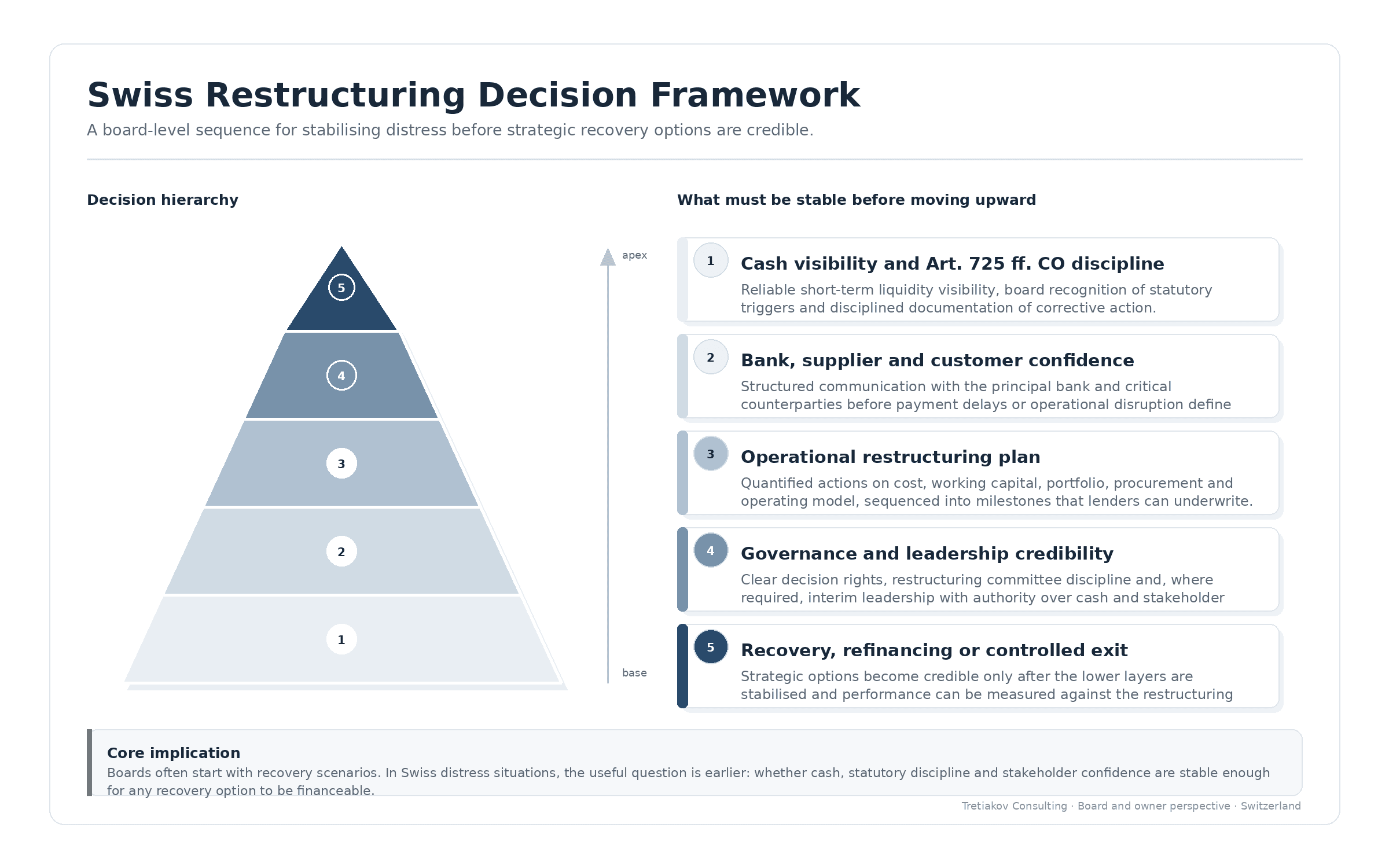

The Swiss restructuring decision pyramid

Each layer depends on the one beneath it. Recovery cannot be reached if the layers below remain unstable.

The pyramid is the practical answer to a question that boards in distress often ask in the wrong order. The discussion frequently starts at the apex, with recovery scenarios and exit narratives, when the only useful question at that stage is whether the base is secure.

What this means for boards and owners

Restructuring and turnaround in Switzerland reward boards that move early, communicate directly with their principal banker, and accept the limits of internal credibility once stakeholders have started to recalibrate. The legal framework is precise but it is not the source of recovered value. Cash control, supplier and customer continuity, operational execution and a leadership layer that the bank and the auditor recognise as independent are what determine outcomes.

Official Swiss bankruptcy statistics published by the Federal Statistical Office reported a continued increase in corporate insolvencies into 2024, and subsequent amendments to the Debt Enforcement and Bankruptcy Act in 2025 have made it harder for distressed companies to delay proceedings and have widened the range of creditors able to initiate them. The practical implication for owners and investors is that the framework will be tested sooner rather than later, and the question is whether the company is ready when it is. For owners and investors evaluating a portfolio asset under financial pressure, business rescue in Switzerland is best approached as a structured governance and execution engagement rather than as a procedural matter handed to lawyers.

This article does not constitute legal advice. In distressed situations qualified Swiss counsel should be involved early, particularly where Art. 725 ff. CO, Nachlassstundung options, mass dismissal procedures or social plan obligations may be triggered.

For Swiss boards, owners and lenders facing turnaround management for Swiss companies under financial pressure, Tretiakov Consulting provides board-level support and interim execution through its advisory work in Switzerland and interim management and operational leadership mandates.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.