Market Entry Consulting in Uzbekistan: Separating Reform Signals from Executable Reality

Uzbekistan is a genuine opportunity, and that is precisely why it is dangerous to enter casually. The growth is real, the demographic base is favourable, and the reform direction has been consistent for several years, yet capital is still arriving faster than the operating conditions that make that capital productive. For a mid-market company, the commercial risk is rarely the decision to enter; it is the sequence, the structure, and the local dependencies chosen along the way. Treating an announced reform as though it were an administered one is the single most expensive error an entrant can make in this market. Disciplined market entry consulting in Uzbekistan exists to close that gap. It separates what the verifiable data supports from what the promotional narrative implies, and it converts an attractive macro story into an executable plan a board can stand behind. This brief sets out how to read the market and, more importantly, how to sequence the decision.

Why growth in Uzbekistan does not remove execution risk

The macro case is worth stating plainly before it is qualified. According to the World Bank's Uzbekistan country overview, real GDP growth averaged around 6 per cent annually between 2017 and 2025, and output expanded by roughly 7.7 per cent in 2025 after about 6.7 per cent the year before. The International Monetary Fund's 2026 Article IV mission recorded the same broad trajectory, with growth supported by consumption and investment rather than a single commodity cycle, and the Asian Development Bank projects continued expansion through 2026 and 2027. Beneath these figures sits a population of more than 38 million, young by regional standards, with a majority under thirty, as documented in the United States Department of State's 2025 Investment Climate Statement.

Strong growth of this kind attracts a particular mistake. Investors read the demographic and growth data, conclude that demand exists, and then treat the investment climate in Uzbekistan as if it were already an operating environment of the type they know at home. Demand and operability are different variables, and they move on different timelines. Doing business in Uzbekistan today means working inside an economy that is liberalising quickly but unevenly, where the rules an entrant negotiates in the first quarter may be revised in the third. The practical consequence for an entrant is that the entry question must be reframed from the start. It should not ask only whether the country is growing; it should ask whether the specific segment is accessible, whether the route to customers is controllable, whether the chosen entry mode reduces or imports local dependency, and whether the company can actually govern the operation after launch. Holding that discipline is the core of any serious FDI advisory in Uzbekistan, and it is what separates a thesis that reads well in an investment committee from one that survives the first eighteen months of execution.

Reform signal versus executable reality

The most useful distinction for anyone assessing foreign direct investment in Uzbekistan is the line between a reform that has been announced and a reform that has been implemented and is being administered consistently. The two are routinely conflated, and the conflation is expensive because it leads entrants to price assets and timelines as though the reformed state already exists.

The legal architecture illustrates the point. As the OECD's 2025 Roadmap for Sustainable Investment Policy Reforms in Uzbekistan sets out, the country has rebuilt its investment framework over recent years, adopting a Law on Investments in 2019, a public-private partnership law in 2019, and a special economic zones law in 2020. The same review notes that these instruments have already been revised significantly and that a new draft Law on Investment was under examination during 2025. That pace of legislative change is double-edged. It signals genuine intent, and it means the statute governing an investor's protections at the point of commitment may not be the statute that governs them at the point of dispute. A market entry strategy framework that does not build for legislative churn is incomplete. The administrative reforms tell the same story in miniature: the State Department records that twenty-two licence categories were abolished in January 2024 and that dedicated investment-manager roles were created within the Ministry of Investment, Industry and Trade, while the same source notes that local officials have at times interpreted laws inconsistently and in ways detrimental to private operators. Both statements are true at once, and a credible market entry strategy in Uzbekistan holds them together rather than choosing the more flattering one.

For a board, the issue is not whether reform is genuine. It is which reforms are already administered, which remain in transition, and which assumptions should be treated as contingencies rather than baselines. The table below frames the reforms that most affect an entrant's commercial case around exactly that question.

Table 1. Reform signal versus executable reality

Reform area | Announced signal | Executable reality | Board question for the entrant |

|---|---|---|---|

Currency convertibility | Som liberalised; Article VIII accepted in 2017 | Current-account convertibility functions; the capital account remains only partially open | Can we move trading flows freely, and have we deliberately structured capital movement and exit? |

Investment law | New draft Law on Investment under review in 2025 | Framework rebuilt repeatedly since 2019 and still revising | Are investor protections stable enough for this commitment, and are contracts drafted defensively? |

Banking privatisation | State share of bank assets targeted at no more than 40 per cent by 2025 | Target not met; only Ipoteka Bank sold to a foreign strategic investor since 2020 | Where will local financing come from, and what is the quality of the lending balance sheet behind it? |

State enterprise divestment | Large privatisations and a National Investment Fund launched | Fund established in 2024 to prepare state assets; Uzbekistan's National Investment Fund completed its first international IPO on the London Stock Exchange in May 2026, while several underlying flagship asset sales and privatisations remain uneven | Does the listing improve liquidity and governance at fund level, and which underlying assets are genuinely investable, governable and exit-ready? |

Energy tariffs | Liberalisation programme | Base electricity tariff effectively doubled across the 2024 and 2025 increases | Do our input-cost assumptions for energy-intensive operations use post-liberalisation pricing? |

WTO accession | Accession actively pursued | Bilateral deals concluded with key partners; the country is not yet a member | Does our tariff and market-access model rely on member treatment that does not yet exist? |

Sources: OECD (2025); IMF Article IV (2024); EBRD Transition Report (2024-25); U.S. State Department (2025); WTO accession record.

How to read FDI data before committing capital

Few parts of the Uzbekistan story are more misread than the headline investment figures, and the misreading directly affects how an entrant sizes the competitive field. Two numbers are in wide circulation, and they are not interchangeable.

On the balance-of-payments basis used for cross-country comparison, the UNCTAD World Investment Report 2025 country fact sheet records inflows of about 2.84 billion US dollars in 2024, up from roughly 2.16 billion the previous year, with an accumulated inward FDI stock of around 16.73 billion dollars, equivalent to close to 15 per cent of GDP. The State Department, drawing on the national definition, reports a far larger figure of around 12 billion dollars of FDI in 2024. Both are accurate within their own conventions. The divergence is definitional: the UNCTAD measure captures net equity, reinvested earnings, and intercompany lending after disinvestment, while the national measure counts a broader pool of investment with foreign participation, including loans. The instruction for an entrant is to never quote a single FDI number without naming its basis, and to treat the government's published ambition, a cumulative target of roughly 110 billion dollars by 2030, as a statement of intent rather than a record of flows that have arrived.

This reconciliation is not pedantry, and it changes a real decision. If a competitor's apparent presence is inferred from the broad figure while an entrant's own capital is modelled on the narrow one, the entrant systematically overestimates the field and underestimates its own relative weight. Rigorous foreign direct investment advisory in Uzbekistan reconciles the bases first and reasons second, which is why disciplined FDI advisory earns its place ahead of the deal rather than after it.

The operational constraints foreign entrants underestimate

The reform debate becomes concrete at the level of who actually controls the market an entrant proposes to serve. Four constraints recur, and each one changes a specific entry assumption.

State-owned enterprises and state banks

The EBRD's Uzbekistan country strategy for 2024 to 2029 notes that large state-owned enterprises and state-owned banks still account for more than half of GDP. That single fact reshapes the meaning of competition. In the most state-heavy sectors an entrant is not competing with a private incumbent on commercial terms; it is operating alongside an enterprise whose cost of capital, procurement behaviour, and pricing latitude are shaped by the state. The mechanism that matters is crowd-out: where a state enterprise dominates supply or distribution, a private entrant's unit economics are set less by its own efficiency than by the incumbent's mandate. The entry implication is that competitive analysis must map state ownership across the value chain before any pricing model is built, and that genuine state withdrawal from an asset, rather than its mere announcement, is what creates a real opening, a distinction we examine in detail in our analysis of privatisation in Uzbekistan for foreign investors.

Financing and foreign exchange

The financing system carries the same imprint. The IMF's 2024 Article IV staff report documents a banking sector in which privatisation has advanced slowly; the only large state bank sold to a foreign strategic owner since 2020 is Ipoteka Bank, acquired by OTP Group, and several other flagged sales have been postponed more than once. Local debt capacity therefore remains concentrated in institutions with legacy books. Currency mechanics follow the same logic of partial reform. The som is convertible for current-account transactions, a status secured when the country accepted the relevant IMF obligations in 2017, but the capital account is only partially open. Reserves are substantial, with the EBRD's Transition Report 2024-25 recording cover well above ten months of imports, and the central bank has held a firm stance with a policy rate of 14 per cent set in 2025. The entry implication is precise: trading cash flows can be moved with reasonable confidence, while capital structuring, dividend timing, and exit routes deserve early and specific design rather than a template imported from a more open market.

Talent and management capacity

The working-age population is large, but managerial and specialist capacity is scarce, female labour-force participation runs materially below male participation according to the ADB's country partnership strategy for 2024 to 2028, and sustained labour migration continues to draw skilled workers abroad. The entry implication is that a hiring and retention plan, including expatriate cover for key roles in the first phase, belongs in the entry model rather than in a later operational review.

Logistics and corridor dependency

The country is doubly land-locked and depends heavily on regional transport corridors, so landed cost and lead-time assumptions must be built from the corridor outwards rather than from a port that does not exist. The entry implication is that any business case resting on imported inputs or exported output should stress-test transit cost and time before it is presented, because logistics, not tariffs, is frequently the binding cost variable.

Choosing the right entry mode in Uzbekistan

Once the operating environment is understood, the question of how to enter becomes tractable. The error to avoid is selecting a mode by familiarity. The modes of market entry available here, a lighter distribution arrangement, a wholly owned subsidiary, a joint venture with a local partner, or an acquisition of an existing operator, each interact differently with the constraints above, and the right choice depends on where an entrant's principal risk actually sits.

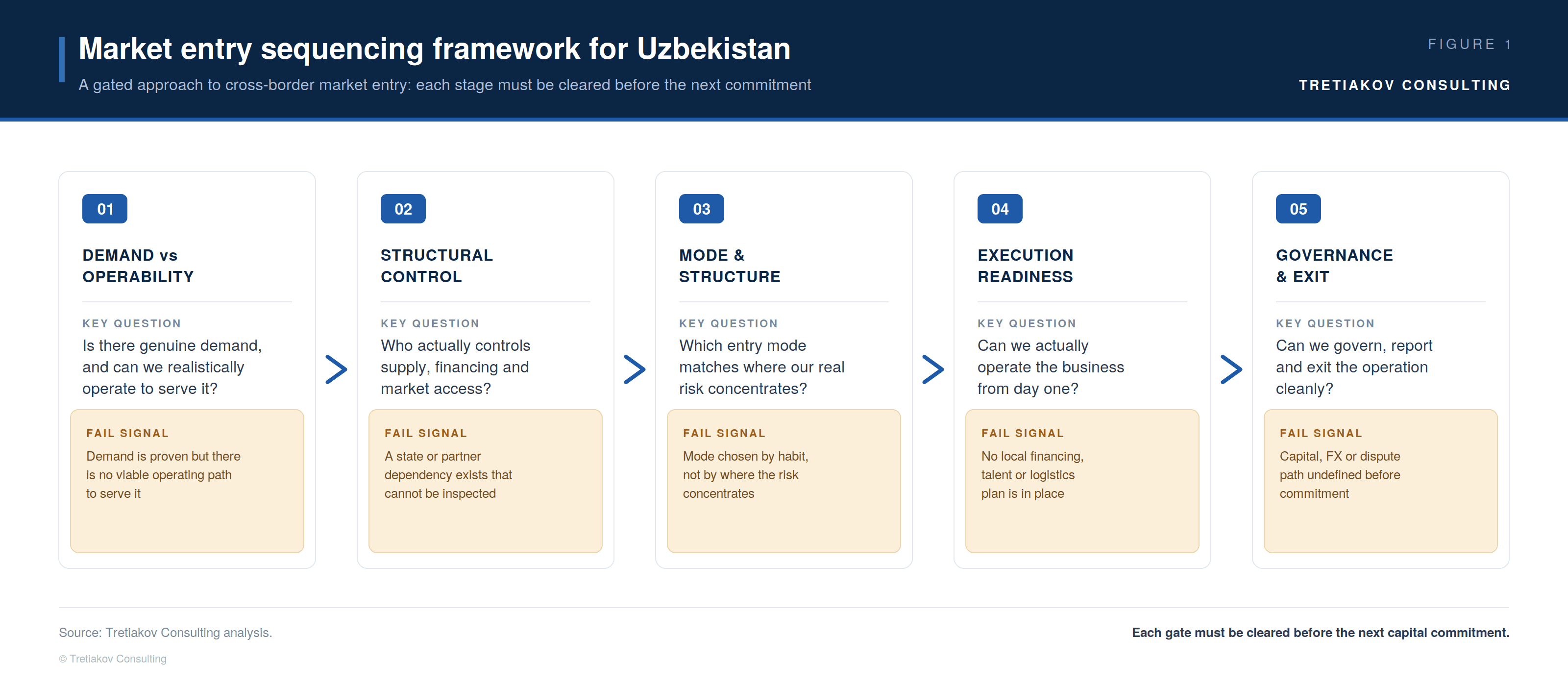

The framework below sets out the sequence we apply. It is deliberately gated: each stage carries a question and a failure signal, and an entrant that cannot clear a gate should not pay to proceed past it. This is the discipline that turns an opportunistic commitment into a defensible country entry strategy, and it is the operational backbone of any sound international expansion strategy.

Figure 1. Market entry sequencing framework for Uzbekistan

Most failed entries did not fail at stage one; demand was usually real. They failed at stages two and four, where a structural dependency was missed or where a legal entity was created without an operating spine beneath it. A market entry strategy for foreign companies in Uzbekistan that runs these gates in order will reject some attractive-looking opportunities early, which is the point. The matrix below makes the mode decision itself explicit.

Table 2. Entry-mode decision matrix

Entry mode | Use when | Avoid when | Main diligence question |

|---|---|---|---|

Distributor or light presence | Demand is unproven and a low-commitment test is sensible | Control, brand execution or IP are central to value | Can the distributor genuinely create demand, or only fulfil it? |

Wholly owned subsidiary | Control, IP protection and long-term presence matter | Market access depends on relationships the entrant cannot build alone | Can the company operate without an undisclosed local dependency? |

Joint venture | Access and execution require capabilities only a local partner holds | Partner transparency or independence is weak | Is the partner's advantage inspectable, lawful and durable? |

Acquisition | Speed and an existing customer base are decisive | Accounts, contracts or liabilities are unreliable | Can value be controlled after closing, not just bought? |

Foreign subsidiary setup

Foreign subsidiary setup in Uzbekistan is more straightforward administratively than its reputation suggests, and that can mislead. The common vehicle is a limited liability company with foreign participation, which carries a minimum charter capital of around 31,000 to 32,000 US dollars, and registration itself can be completed within a small number of business days. Ease of incorporation is not the same as ease of operation. Setting up a subsidiary in Uzbekistan establishes a legal presence; it does not resolve supply access, distribution reach, or the regulatory relationships that determine whether that presence trades profitably. The administrative gate is low and the operational gate is high, and conflating the two is a frequent cause of stranded local entities.

Local partner search and the acquisition route

Local partner search in Uzbekistan is therefore less a procurement exercise than a control decision. A capable partner can shorten the path to distribution, regulatory familiarity, and recruitment, which is precisely why local partner search for foreign investors in Uzbekistan should test the partner's independence from the state-dominated parts of the value chain as carefully as it tests commercial fit. The risk is not the absence of partners; it is dependency on a partner whose advantages flow from relationships an entrant cannot inspect and cannot replace. Entering Uzbekistan through acquisition or partnership can compress timelines materially, but it transfers the diligence burden onto the integrity of the target's accounts, contracts, and obligations, and it raises the question of post-deal control that determines whether value is captured or merely purchased. Our market entry and business expansion advisory is built around exactly this distinction, supported by Uzbekistan-specific advisory context.

Where opportunity is bankable and where it is still a target

Sector selection is where the reform-versus-implementation distinction pays off most directly, because some sectors have moved from policy to bankable transactions while others remain at the announcement stage. The useful question is not which sector is growing, but for whom it is an opportunity, through which entry route, and with what risk profile.

Energy and renewables is the clearest case of executed opportunity. The OECD review records that a substantial pipeline of solar and wind capacity, equivalent to a meaningful share of installed generation, is being developed by foreign investors under public-private partnership structures, with a large portion awarded competitively. For suppliers, EPC contractors, specialist equipment manufacturers and industrial service providers, this is not merely a policy theme; it creates an addressable project ecosystem with identifiable foreign sponsors, PPP frameworks and clearer procurement channels than most other sectors offer, a dynamic we set out further in our review of infrastructure investment in Uzbekistan. The flagship is a multi-gigawatt wind programme in the country's west backed by a regional developer under long-term power-purchase agreements, which means the route to revenue is contractible rather than speculative. Information technology and digital services occupy a similar position for software firms and service providers, supported by a residency regime that offers genuine tax relief and a dedicated legal framework. Automotive and industrial assembly have attracted committed foreign capital, illustrated by a joint venture in electric-vehicle manufacturing that progressed from agreement to an operating facility within a year, an entry route most relevant to manufacturers and component suppliers willing to localise. Mining and metals carry world-class reserves but also display the implementation gap visibly: a flagship metals listing has been delayed repeatedly and the stake on offer reduced, a clean example of an asset that is real but not yet transactable on the terms a foreign minority investor would want.

The integration agenda sits above all of these. The country is pursuing accession to the World Trade Organization and has concluded bilateral market-access deals with major partners, including an agreement with the European Union in late 2025. The World Bank's 2025 Country Economic Memorandum estimates that accession could lift GDP by a substantial margin over time, while noting that trade openness has risen sharply yet only a small minority of firms export. The commercial read is that the integration upside is large and credible but not yet realised, so an entrant should model the present regime and treat accession as optionality rather than as a baseline. This is also where business expansion in Uzbekistan connects to the wider region, because a presence here is increasingly a corridor position rather than a single-country play, and a considered business expansion strategy in Uzbekistan should account for that regional logic from the outset.

What disciplined market entry consulting in Uzbekistan should deliver

The purpose of advisory work in this market is not to assemble a country report; it is to convert an attractive macro story into an executable plan that survives contact with the operating environment. A serious mandate should not stop at market sizing. It should test demand, access, structure, partner risk, operating model, governance and exit assumptions as a single sequence, and produce decisions rather than description. In practical terms, that means market entry consulting in Uzbekistan has to deliver across the workstreams set out below.

Table 3. What a serious market entry mandate should cover

Workstream | What must be tested | Output |

|---|---|---|

Market attractiveness | Demand, price points, customer concentration, competitive structure | A defensible entry thesis |

Operability | Supply, logistics, licences, foreign exchange, talent availability | An operating feasibility map |

Partner and acquisition screen | Ownership, political exposure, contracts, hidden liabilities | A partner shortlist and red-flag register |

Entry mode and structure | Subsidiary, joint venture, acquisition or distributor against the risk profile | A recommended entry structure |

Governance and exit | Reporting lines, controls, escalation, repatriation and exit routes | A board-ready entry and governance plan |

Read against this standard, the difference between a generic market study and disciplined market entry consulting becomes clear. The first describes a country; the second tells a board which gate it has not yet cleared and what evidence is required to clear it. Market entry consulting for European companies in Uzbekistan, in particular, should be grounded in the corridor logic, the partner-dependency risk and the structuring discipline above rather than in an imported playbook, and it should answer the real question owners and chief executives are asking, which is how to enter the Uzbekistan market as a foreign mid-market company without mispricing execution risk.

This is also where entry connects to the work that follows it. A subsidiary or joint venture is only the beginning; the harder task is building the operating model for new market operations that makes the local entity perform, and, where an entrant has chosen the acquisition route, executing the M&A and post-deal integration that determines whether the deal creates value or merely consolidates two sets of problems. For companies whose principal challenge is reaching customers rather than building operations, the entry question shades into commercial transformation and go-to-market strategy, and the choice of mode should reflect that. Each of these is a continuation of the same sequence, delivered under a clear advisory engagement model, because the entrants who succeed are those who plan the second year while deciding the first.

Conclusion

Uzbekistan rewards the entrant who reads it accurately and punishes the one who reads it optimistically. The growth is durable, the demographic base is favourable, the reform direction is consistent, and the integration agenda is credible. None of that removes the practical truth that capital is still arriving ahead of operability, that more than half the economy remains in state hands, and that the gap between an announced reform and an administered one is wide enough to decide whether a project earns its cost of capital. Sound market entry consulting in Uzbekistan does not resolve that gap by ignoring it; it builds the entry around it, gating the decision so that demand, structural control, mode, execution readiness and governance are each proven before the next commitment is made. Entrants who reason this way will find a market that is genuinely open to them, while those who treat the headline as the whole story will fund the difference between the two on the most expensive terms the market offers.

Before committing capital, Tretiakov Consulting can help you test whether the Uzbekistan opportunity is commercially attractive, operationally executable and governable after entry, and translate that judgement into a board-ready entry plan. Speak to our team before the commitment, not after it.

Frequently asked questions

What does market entry consulting in Uzbekistan involve beyond a market study? At the executive level it involves three things a study does not provide. It reconciles conflicting investment and reform data into a single defensible commercial case, it selects an entry mode based on where the entrant's risk actually concentrates, and it designs the post-entry operating and governance model. The deliverable is a sequenced, gated decision rather than a report, because the commercial failures in this market occur in execution and structuring, not in the initial assessment of demand.

What is the best entry mode for a foreign company in Uzbekistan? There is no single best mode; the right one follows the entrant's principal risk. Where the binding constraint is distribution and regulatory access, a local partner can shorten the path, provided the partner's independence is verified. Where the constraint is control or intellectual property, a wholly owned subsidiary is preferable despite a slower commercial ramp. Where speed and an existing customer base are decisive, acquisition is strongest, but it transfers the entire risk burden onto diligence and integration. The mode is a consequence of the risk profile, not a starting preference.

Why do FDI figures for Uzbekistan differ between sources? Because two definitions are in circulation. The balance-of-payments measure used internationally captures net equity, reinvested earnings and intercompany debt, and produces a figure in the low single-digit billions for recent years. The national measure captures a broader pool of investment with foreign participation, including loans, and produces a figure several times larger. Neither is wrong, but comparing a competitor's presence under one definition with an entrant's plan under the other distorts the analysis. The first task of foreign direct investment advisory in Uzbekistan is to fix the basis before drawing conclusions.

How long does it take to build a functioning operation in Uzbekistan? Incorporation is fast and can be completed within days, but a functioning operation is a different milestone. Once supply access, distribution, local financing, recruitment and the necessary regulatory relationships are accounted for, a realistic horizon to stable operation is measured in quarters rather than weeks. The administrative speed of foreign subsidiary setup in Uzbekistan is genuinely high, which is precisely why entrants underestimate the operational timeline that follows it.

Should WTO accession change the timing of entry? It should inform timing without dictating it. Accession is being actively pursued and bilateral market-access deals have been concluded, but the country is not yet a member, so tariff and market-access modelling should use the present regime. An entrant who establishes a credible position before accession is better placed to benefit from it than one who waits for confirmation, provided the commercial case already stands on current conditions rather than on a future treatment that has not yet taken legal effect.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.