M&A Advisory in Uzbekistan for Mid-Market Cross-Border Deals

For much of the past decade, the binding constraint in buying a company in Uzbekistan was not price or process but the scarcity of targets a foreign buyer could seriously underwrite. That constraint has begun to ease as reform, privatisation and private-sector expansion bring more assets into view, and the difficulty has moved downstream. The harder question now is whether a target that looks acquirable can in fact be governed, integrated and made to hold its value once an external owner takes control, because that is where the investment case is either confirmed or quietly destroyed. This is the question that serious M&A advisory in Uzbekistan has to answer, and it is rarely the one a deal sponsor arrives with. Most arrive focused on price and pipeline, since that is where the visible activity sits, while the commercially decisive work begins only after the indicative offer, in the parts of the business that no teaser and no auction process will ever disclose.

This article is written for the decision-makers who carry the consequences of that gap: owners preparing to sell, foreign acquirers and mid-market investors building a position, boards approving capital, and the executives expected to run the asset on the first morning after completion. It sets out where mid-market cross-border deals in the country tend to break, why those failures are usually visible well before signing if the right questions are asked, and what an adviser should be doing across the full lifecycle rather than only at the point of transaction execution.

Why deal supply has stopped being the constraint

Uzbekistan has spent several years converting reform announcements into a visible deal pipeline, and the supply side now looks unusually active for a market of its size. Growth has been strong and sustained. The World Bank records average annual real GDP growth of around six per cent between 2017 and 2025, while noting that the economy has leaned heavily on capital investment rather than on broad-based private productivity. The World Bank's Country Economic Memorandum puts the trade-to-GDP ratio at 71.6 % in 2022 yet observes that only about six per cent of firms export, a combination that tells you the economy is opening faster than the average company inside it is becoming competitive. The same body estimates that accession to the World Trade Organization could lift GDP by up to seventeen per cent over time. That projected upside is part of what is drawing international acquirers, but it also reshapes the diligence problem, because a buyer is then underwriting a company whose future earnings may depend less on inherited protection and more on its ability to compete as the economy opens further.

The privatisation programme has added to that sense of momentum. According to the EBRD's transition report, a presidential resolution in April 2025 initiated the divestment of the state's holdings in twenty-nine state-owned enterprises through public auctions, alongside the planned listing of twelve enterprises through public offerings over the 2025 to 2028 period, with energy tariffs raised in mid-2025 as part of the same reform direction. This is a substantial supply of potential assets, and it is genuine. It is also, importantly, a programme that has been launched rather than delivered, and that distinction matters more than it first appears.

A pipeline creates access, not investability. An asset can be available, fairly priced and strategically attractive, and still fail every test that matters to a foreign owner: whether control can be secured against a concentrated local shareholder base, whether reporting can support governance from outside the company, whether licences and land-use rights survive a change of control, and whether management can operate under a different ownership model at all. Distinguishing the two is the central problem that M&A advisory for mid-market companies in Uzbekistan exists to manage, because the market now supplies activity far more readily than it supplies execution certainty. Reading availability as opportunity is therefore the first and most expensive error a buyer can make, and avoiding it is the first task of M&A advisory in Uzbekistan.

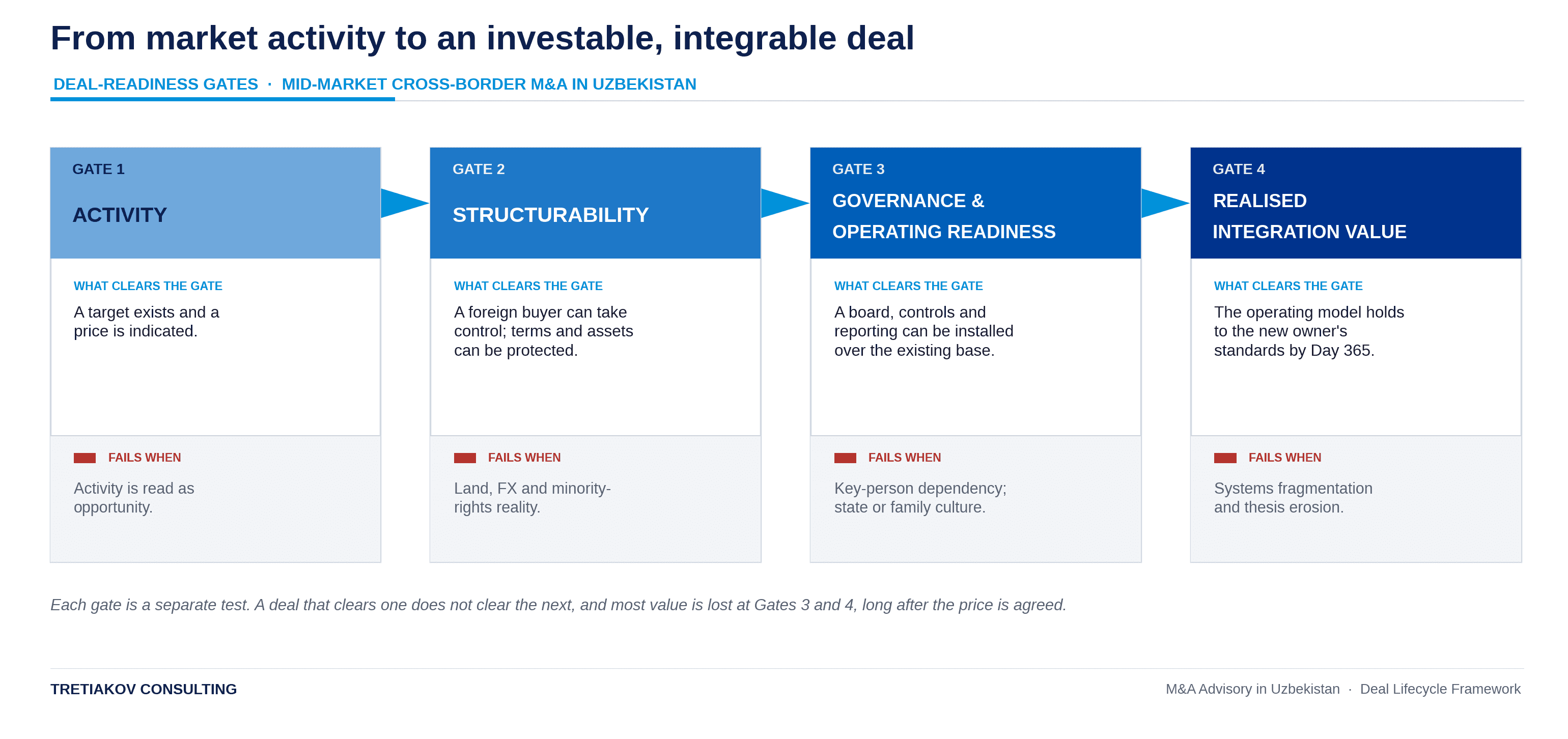

Figure 1. From market activity to an investable, integrable deal

Each gate is a separate test. A deal that clears one does not clear the next, and most value is lost at Gates 3 and 4, long after the price has been agreed.

Acquiring a company in Uzbekistan as a foreign buyer: the structuring reality

For a foreign buyer, the structuring of the deal is where reform progress and on-the-ground reality diverge. Investment has grown since liberalisation began in 2017, but it remains shallow and concentrated. The OECD's 2025 investment policy roadmap reports that foreign direct investment inflows were equivalent to about 2.1 per cent of GDP in 2024 and that the stock of foreign investment stood at roughly 14.6 per cent of GDP, modest by comparison with peer economies, with inflows clustered in manufacturing, energy and extractives and dominated by Chinese and Russian investors. For a mid-market acquirer operating outside those sectors and source countries, this means fewer precedents, thinner comparable transactions and far less institutional memory to draw on when structuring an acquisition in Uzbekistan.

The legal framework is being rebuilt rather than settled, and that is the operative condition for anyone acquiring a company in Uzbekistan as a foreign buyer. The OECD records that statutory restrictions on foreign direct investment are concentrated in real estate, and that limited foreign access to land carries consequences well beyond property, since it constrains any land-dependent operation. The principal instruments, the 2019 Law on Investment, the 2019 law on public-private partnerships and the 2020 special economic zones law, are recent, have already been amended, and a further investment law is in preparation. None of this is a reason to stay away, but it is a reason to treat legal and regulatory movement as a structuring variable rather than as background context. A buyer should assume that the rules as drafted at screening may not be the rules at completion, and the agreement therefore has to allocate that risk explicitly, through conditions precedent, staged consideration, termination triggers and warranties that carry practical recourse rather than decorative comfort.

In practice, cross-border M&A advisory for foreign investors in Uzbekistan turns on a small number of structuring questions that decide whether a deal is durable rather than merely signed. Can the buyer secure control rights that survive a concentrated local shareholder base? Can dividends, debt service and exit proceeds be repatriated on predictable terms? Are the assets that underpin the valuation, including land-use rights, licences, permits and key customer contracts, genuinely transferable, or at least economically controllable, after completion? Where any of these answers is uncertain, the discipline is to price the uncertainty and document it rather than leave it to post-closing goodwill, which is precisely how sound cross-border M&A advisory protects a buyer against the exposures a data room was never going to disclose.

Commercial due diligence in Uzbekistan: what acquirers consistently get wrong

The most common error in commercial due diligence in Uzbekistan is to read a target's reported market position as evidence of competitive strength, when historical revenue may instead reflect protected access, administrative allocation, state-linked demand, related-party flows or a legacy market structure rather than a franchise able to withstand open competition. The IMF's most recent Article IV report notes that state-owned enterprises remain dominant across strategic sectors and that, even where some restructuring has separated regulatory from operational roles, major state firms still occupy positions that allow them to exercise monopoly power. When a target's revenue rests on a protected position, an administrative allocation or a relationship with a state counterparty, its historical numbers describe a market that may not exist once that protection is withdrawn. The reported revenue may be entirely real, while the economic franchise that produced it is considerably weaker than the accounts imply.

This is why commercial diligence, done properly, is an exercise in testing the durability of earnings rather than confirming them. It asks what the business would earn under genuine competition, what share of its margin rests on related-party arrangements, and how much of the customer base would remain if pricing moved to a commercial basis. The IMF's analysis of reform sequencing is direct that the harder reforms, hardening budget constraints on state enterprises and improving corporate governance, are still in progress, which means the competitive environment a buyer underwrites today is itself a moving target.

Two operational realities consistently surprise acquirers. The first is key-person dependency. In owner-led and state-legacy businesses alike, critical relationships, approvals and commercial knowledge often sit with a handful of individuals and are embedded in neither systems nor contracts, so the asset a buyer pays for can simply walk out of the building. The second is the quality of the information itself. In many mid-market situations, management accounts are prepared primarily for tax, for a lender or for owner control rather than for an external board, and they rarely withstand the reporting discipline an institutional owner imposes once the deal closes. A buyer who does not test this during due diligence for a target company in Uzbekistan inherits the problem on Day 1, when the numbers used to justify the price turn out not to reconcile to anything that can be governed.

Environmental, social and governance exposure belongs inside this work rather than beside it. The OECD's roadmap highlights that occupational health and safety remains a real concern, particularly in construction and across the informal economy, where informal labour is widespread. For an acquirer, ESG due diligence in M&A in Uzbekistan is therefore a pricing and liability matter rather than a reporting formality, because undocumented labour practices, safety liabilities and environmental obligations all transfer with the company, and they are far cheaper to identify before signing than to remediate afterwards. Rigorous commercial due diligence and disciplined ESG review are the same instinct applied to different risks, namely a refusal to take the seller's story at face value.

Selling a family-owned business in Uzbekistan: the sell-side and succession problem

Many private companies of meaningful scale are still founder-led or family-controlled, and that ownership reality shapes the whole of the sell-side problem. Value is rarely lost in the negotiation. It is lost much earlier, in a lack of preparation that makes the business harder to underwrite than it needs to be. Selling a family-owned business in Uzbekistan exposes precisely the weaknesses that commercial diligence is designed to find: accounts arranged around the owner, assets and personal interests that are not cleanly separated from the company, and decision-making that has never been tested without the founder in the room.

For a seller, preparation should therefore begin well before a buyer is invited into the process. Accounts need to be normalised onto a basis an external board would recognise, related-party transactions identified and explained, owner-linked assets separated from those of the company, land, licence and permit positions documented, and the management team tested as a standalone operating unit rather than as an extension of the founder. These are not cosmetic steps. Each one removes a discount that a buyer would otherwise apply for uncertainty, and together they determine whether the company is sold as an institution with transferable value or as a dependency on a single individual.

Succession is increasingly the trigger for these transactions, as a first generation of post-independence owners begins to weigh exit and continuity. Here the sell-side problem and the governance problem are the same problem. A business that cannot demonstrate it will function without its founder will attract fewer credible buyers and a lower price, because the buyer is being asked to pay for an enterprise while underwriting the risk that the enterprise is, in reality, one person. Effective succession M&A advisory for family-owned companies in Uzbekistan therefore begins long before any sale process, by building the governance, reporting and management depth that allow the company to be sold as an institution rather than as a relationship. Owners who treat that work as administrative housekeeping rather than as value creation tend to discover the cost of the view in the final price.

Post-merger integration in Uzbekistan: where value is won or lost

In many cross-border deals, underperformance is not created at signing but revealed during the first year of ownership. The price can have been negotiated correctly and the thesis can be sound, yet the investment case still deteriorates if the buyer cannot install control, retain the people who hold the business together, reconcile reporting to a standard a board can actually use, and move the company onto an operating model that supports the new owner's requirements. Post-merger integration in Uzbekistan is where the assumptions made in diligence meet the practical reality of running the asset, and where the gap between a signed deal and a controlled one becomes both visible and expensive.

The mechanism is straightforward to describe and hard to manage. The acquired company has been run on an operating model, a culture and a set of controls that suited its previous owner, whether that owner was a founder or the state. Installing an external owner's governance over that base is not a formality. The IMF and the EBRD, which has spent years supporting corporate-governance reform in the country's state enterprises, both treat weak board independence and immature governance as structural features rather than isolated faults. In integration terms this translates into specific and recurring friction: reporting lines that do not produce reliable numbers, financial systems that cannot be consolidated without being rebuilt, decisions that still route informally to the former owner, and a management team that may never have worked under a genuine board. These are the post-merger integration challenges in Uzbekistan that decide whether the deal thesis survives contact with the asset.

A workable integration is sequenced rather than simultaneous. The first hundred days should secure control, meaning banking and cash, authorities and signatures, the key people who hold the business together, and a reporting baseline the new owner can actually trust. The harder work follows across the remainder of the year. It involves rebuilding the post-acquisition operating model so that the company can run to the acquirer's standards, and providing the corporate development support that turns a single acquisition into a platform rather than a stranded asset. This is also why dedicated post-merger integration consulting is treated as a distinct discipline, since the skills that close a deal are not the skills that make it work. For a foreign acquirer, this is where corporate development support for acquisitions in Uzbekistan becomes commercially decisive, because the buyer is no longer evaluating a deal but converting a newly acquired company into a controllable platform, and it is in that conversion that the difference between the price paid and the value realised is finally settled.

Table 1. The Uzbekistan deal lifecycle: where mid-market cross-border deals break

Deal stage | What looks ready | What is usually not ready | Primary execution or governance risk | Advisory intervention |

|---|---|---|---|---|

Sourcing and screening | A target exists and a price is indicated | Whether the market position is competitive or protected | Mistaking availability for opportunity | Screen for governability and integrability, not only strategic fit and price |

Commercial due diligence | Audited or management accounts | Durability of earnings under real competition | Related-party and monopoly-dependent revenue | Stress-test the franchise; separate earned margin from protected margin |

Structuring and negotiation | Headline terms and a valuation | Transferability of land, licences and control rights | Rules changing before completion; weak minority protection | Stage consideration; harden warranties and governance rights |

Signing and closing | A signed agreement | Operational readiness for new ownership | Key-person flight; control of cash and authority | Secure banking, signatures, key people and a reporting baseline |

Day 1 to 100 integration | Ownership transferred | Reliable consolidated reporting | Decisions still routing to the former owner | Install governance and a reporting line the owner can trust |

Day 101 to 365 value capture | The business is operating | The operating model brought to the acquirer's standards | Systems fragmentation; erosion of the deal thesis | Rebuild the operating model; build a platform, not a stranded asset |

How to choose the right partner for M&A advisory in Uzbekistan

The practical test of how to choose an M&A advisor in this market is simple to state and revealing to apply: does the adviser carry responsibility across the whole lifecycle, or does the engagement end at signature? Investment banks and large accounting firms play necessary roles in most transactions, but their mandates are typically organised around a narrower point in the lifecycle, whether execution, valuation, financial diligence or tax structuring, and the residual risk sits outside that scope. It surfaces after completion, when the buyer discovers whether the asset can actually be governed, reported, integrated and improved rather than merely owned. The structural weakness of conventional deal support is that it is organised around the moment of the transaction rather than around the value the transaction was meant to create, which is why M&A advisory for mid-market companies in Uzbekistan has to be defined by what happens after completion as much as by what happens before it.

This is the gap that lifecycle M&A advisory in Uzbekistan is designed to close. The point is continuity of judgement, so that the same understanding of a target's governance, operating model and integration risk runs from sourcing through diligence, structuring and into the first year of ownership, and a risk identified in diligence is actually managed in integration rather than rediscovered there. The country's institutions have moved in the same direction. The Asian Development Bank's 2024 to 2028 country strategy frames its own role around private-sector competitiveness and transaction advisory rather than financing alone, a recognition that capital without execution capability achieves very little. For a mid-market acquirer or a family seller, credible cross-border M&A advisory for foreign investors in Uzbekistan is the partner that owns the deal as a process, from first contact to realised value, not the one that owns the announcement.

What this means for buyers and sellers

The opportunity in Uzbekistan is real, and so is the distance between an available asset and an investable company. The next phase of the market will reward the buyers and sellers who treat sourcing, diligence, structuring and integration as a single transaction discipline rather than as separate workstreams handed from one adviser to the next, and who underwrite governance and execution with the same rigour they apply to price. That is the proper role of M&A advisory in Uzbekistan: to separate market activity from executable value, and to carry one continuous line of judgement from first screening through the first year of ownership. The pipeline will keep producing targets; whether those targets become value depends on the work that begins after the indicative offer, and on choosing a partner equipped to see it through.

If you are evaluating an acquisition, a disposal or an integration in the country, Tretiakov Consulting works across the full deal lifecycle, from sourcing and diligence through structuring and into the first year of ownership. Arrange a confidential conversation to scope a specific transaction or to test the readiness of a deal already in progress.

Frequently asked questions

What is commercial due diligence, and why is it more demanding in this market? Commercial due diligence is the assessment of whether a target's earnings are durable under real competition, as distinct from confirming that the reported figures are arithmetically correct. It is more demanding here because a great deal of historical performance has been generated in protected or state-influenced markets, so the central question is not whether the profit was earned last year but whether it can be earned once protection, related-party flows or administrative advantages are removed. A report that validates the past without stress-testing the franchise is of limited use to a buyer, and frequently masks the risk it was commissioned to find.

How should a board choose an M&A advisor for a cross-border deal here? The decisive criterion is accountability across the lifecycle rather than reputation at the point of execution. A board should ask whether the same team that prices the risk in diligence will be responsible for managing it through structuring and integration, because a deal handed between specialists at each stage tends to lose the very insights that protect value. Local knowledge matters, but it is most useful when it is connected to integration capability rather than offered as a set of standalone introductions.

What is the difference between buy-side and sell-side advisory? The distinction between buy-side versus sell-side advisory comes down to whose interests the adviser serves and what therefore drives the work. Buy-side advisory acts for the acquirer and concentrates on paying the right price for an asset that can genuinely be controlled and improved, which makes diligence and integration planning central. Sell-side advisory acts for the owner and concentrates on preparing and positioning the business so that credible buyers compete for it at full value. In a market of concentrated, family ownership, the sell-side task is often less about marketing the company and more about making it institutionally ready to be bought, which is where most of the eventual price is decided.

How long does post-merger integration take? The honest answer is that securing control should take the first hundred days, while genuine integration of the operating model, the systems and the governance typically runs across the remainder of the first year and frequently beyond it. Attempts to compress that timetable tend to fail, because the underlying constraints, the quality of reporting, the maturity of governance and the dependency on key people, cannot be resolved faster than the organisation can absorb change. A credible timeline is sequenced by those constraints rather than by the acquirer's reporting calendar.

Does the privatisation programme make this a buyer's market? Not in itself. A large supply of state assets coming to auction increases the number of opportunities, but it does nothing to change the underlying work of establishing whether any individual asset is governable and integrable. The volume of activity can in fact raise the risk, by tempting buyers to move quickly on availability rather than carefully on readiness. The programme is best read as a reason to be present and disciplined in the market, not as a reason to be fast.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.