Market Entry Consulting in the Netherlands for Foreign Mid-Market Companies

Why the Netherlands rewards companies that decide the country's strategic role before they incorporate, hire or sign a distributor, and penalises those that treat it as a generic "easy" European market.

Most foreign companies that run into trouble in the Netherlands do not fail at the point of registration. They fail several months later, once a subsidiary has been incorporated, an office leased, a first hire made and a distributor signed, and the assumption underneath all of those commitments turns out to have been untested. This is the specific problem that market entry consulting in the Netherlands is meant to address, because the country sets a quiet trap for foreign mid-market companies.

The formal mechanics of entry are so smooth that they disguise the strategic decision that should have come first. A Dutch private limited company, a payroll provider, an accountant and an English-speaking advisory market are all available within weeks, and the ease of those steps creates a false sense that the hard part is over. The hard part has not started. What determines whether the money committed in those first months earns a return is not the speed of incorporation but the clarity of one decision that most entrants never make explicitly, namely what role the Netherlands is actually supposed to play in the company's European strategy.

Why the Netherlands Is Attractive but No Longer an Automatic Entry Choice

The reasons companies are drawn to the Netherlands are concrete, and worth setting out in operating terms rather than as slogans. The OECD's 2025 Economic Survey describes a country with strong institutions, good infrastructure and a highly skilled workforce, and an economy that has stayed resilient through successive shocks because it is deeply integrated into trade and sits at the gateway of European supply chains. For an inbound operator that converts into real advantages. The logistics base around the Port of Rotterdam and Schiphol is genuine, the legal system is predictable, English is functional in commercial life, and the regulatory stance towards foreign investment has historically been comparatively lean, although scrutiny has tightened in knowledge-sensitive sectors such as semiconductors.

The difficulty is that these strengths are now priced into a more crowded and more constrained environment, and the cost of entering badly has risen accordingly. The EY Netherlands Attractiveness Survey, published in mid 2025, recorded that the country had slipped to tenth place among European destinations for foreign investment after years inside the top five, behind Belgium, Spain and Poland. That movement matters less as a league-table position than as a signal that the Netherlands now competes for capital on harder terms. Beneath it lie supply constraints that bear directly on operating cases. The OECD and the IMF both point to electricity grid congestion and persistent labour shortages as structural drags on activity, with the IMF's 2025 Article IV assessment naming grid and nitrogen bottlenecks explicitly. The United States Investment Climate Statement for the Netherlands is blunter still, reporting that companies have flagged shortages of housing and physical space, congestion on the energy grid and labour constraints, and that firms seeking to connect to or expand on the grid have been placed on waiting lists. Eurostat's data places the country among the highest labour cost economies in the European Union, which means any error in headcount or operating model is expensive to carry.

The conclusion to draw is not that the Netherlands has become unattractive. It is that the country has become less forgiving. Entry remains a sound choice for the right company with the right sequence, but the margin for an unsequenced, assumption-led entry has narrowed, and that is precisely where a disciplined entry strategy begins to earn its cost.

Define the Role of the Netherlands Before Choosing the Entry Mode

The single most useful discipline in any market entry strategy in the Netherlands is to refuse to choose an entry mode until the strategic role of the country has been settled. Mode should follow role, because the role determines almost everything that comes after it: the cost base, the kind of people hired, the partner logic, the governance model and the point at which capital becomes fixed. When the role is decided implicitly, by momentum rather than by analysis, the subsidiary, the partner and the team are all built for a purpose that was never agreed, and the cost of unwinding them later is far higher than the cost of deciding correctly at the start.

In practice the Netherlands can perform one of several distinct roles, and they are not interchangeable. It can be a standalone commercial market, in which case the priority is a local sales capability, pricing authority and customer relationships. It can be a coordination base or European headquarters, in which case the priority shifts to governance, management talent and the tax and legal interface rather than front-line selling. It can be a partnership market, where the decisive question is channel access and the right structure for sharing risk. It can be an acquisition platform, where the work is target screening, commercial due diligence and integration capacity rather than greenfield setup. And it can serve as a distribution and fulfilment role, which is where the country's reputation is strongest and also where the most expensive misjudgements occur.

The case of the Netherlands as a European distribution hub deserves particular care, because the logic is often accepted too quickly. A hub is not valuable because of where it sits on a map. It is valuable only when the physical location matches the geography of the customers being served, the service promise being made, the inventory model being run and the true cost to serve. In many cases the hub is intended to serve not only the Dutch market but the wider Benelux region, which makes the neighbouring Belgian market part of the same decision rather than a separate one. The same grid and space constraints reported by the OECD and the United States Investment Climate Statement turn an apparently administrative decision about warehousing into a strategic one, because connection timelines and the availability of suitable sites can determine whether the hub functions as planned. A company that commits to a hub role without testing those operational realities has not chosen a strategy but a cost.

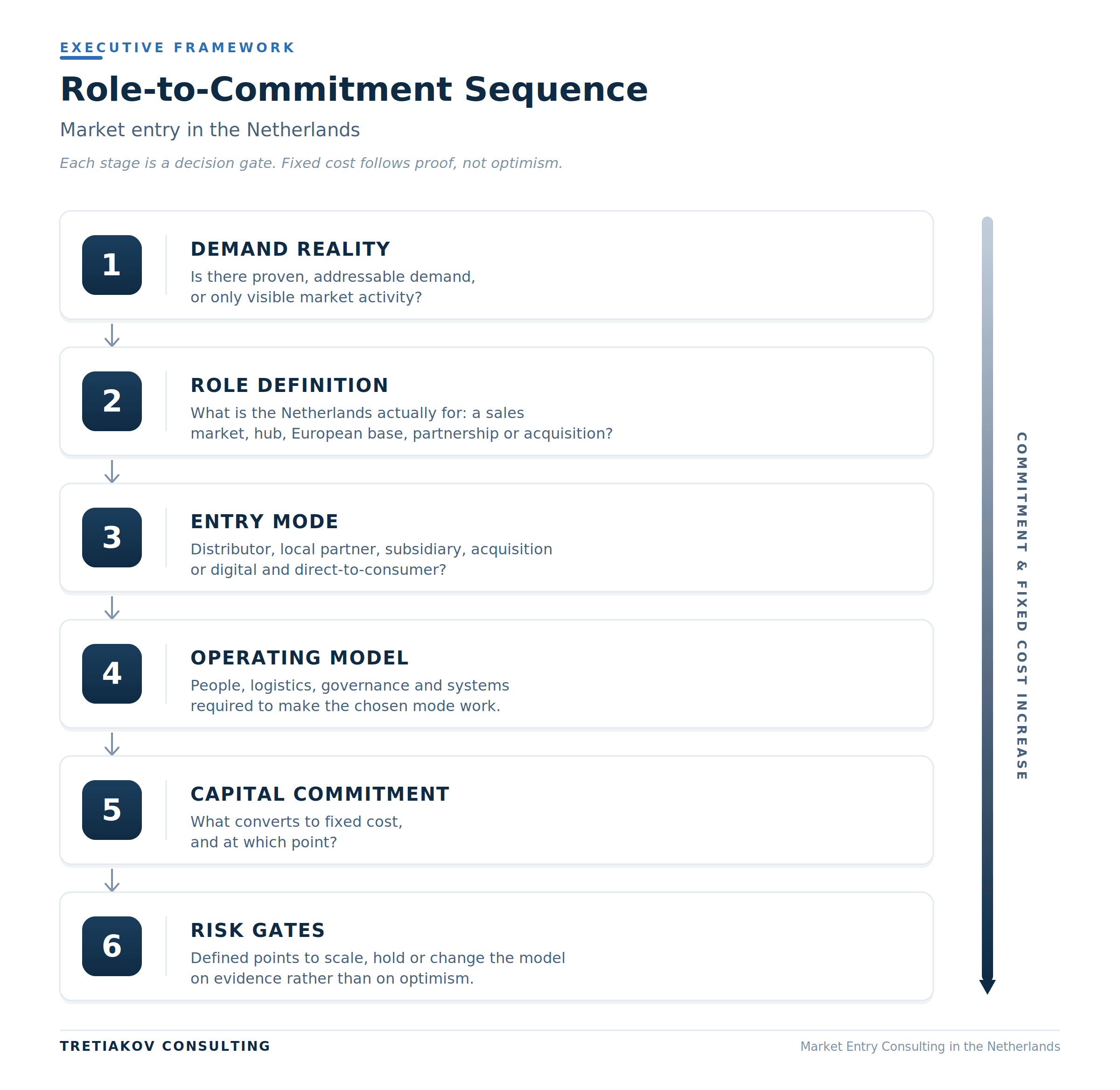

A Market Entry Strategy Framework: From Demand to Operating Commitment

A market entry strategy framework is only useful if it forces decisions in the right order and prevents capital from being committed before the evidence justifies it. The sequence below is the one we use, and it is deliberately built so that fixed cost follows proof rather than precedes it.

Role-to-Commitment Sequence (market entry in the Netherlands)

The framework matters because each stage controls a different category of cost, and skipping a stage transfers risk into the stages that follow. A market entry strategy for foreign companies in the Netherlands that begins at stage three, with the choice of mode, has already lost the ability to judge whether that mode is appropriate, because neither the demand nor the role has been established. The decisive relationship inside the sequence is the trade-off between control and commitment. More control over the market, through a subsidiary or an acquisition, brings better customer learning and stronger accountability but converts cost into fixed structure earlier. Less control, through a distributor or an agent, preserves flexibility and lowers the initial outlay but weakens the company's own understanding of the market and places the customer relationship in someone else's hands. The right position depends on how much proof the company has, how much control the strategy genuinely requires, and how much commitment the business can justify before the hypothesis is confirmed.

Subsidiary, Distributor, Partner or Acquisition: Choosing the Right Mode

The practical question most entrants ask first is whether to set up their own subsidiary or to work through a distributor, and the honest answer is that the question of subsidiary versus distributor in the Netherlands cannot be settled on its own merits. It can only be settled against the role and the level of proof established earlier. A distributor is the right instrument when the priority is to test demand quickly at low fixed cost, and the wrong one when the company needs to learn the market directly, because a distributor model tends to leave the entrant without customer data and with a shared margin. A subsidiary is the right instrument when control and direct learning matter, and the wrong one when it is created before demand has been demonstrated, because it converts a hypothesis into a standing fixed cost. The same logic governs the decision about entering the Netherlands through acquisition or partnership, where speed and acquired capability are weighed against integration risk and the dependence that a partnership creates.

The table below sets out the comparison in the terms that actually drive the decision, including the constraint that is specific to the Netherlands in each case.

Mode | Best when | Main risk | Netherlands-specific constraint |

|---|---|---|---|

Distributor | demand needs testing quickly | weak market learning and no direct customer data | shared margin in a high labour cost economy |

Local partner | access and credibility are decisive | misaligned incentives and channel conflict | partner may end up controlling the customer relationship |

Subsidiary | control and direct learning matter | premature fixed cost before demand is proven | high labour cost, a tight talent market and shifting expat cost assumptions |

Acquisition | speed and capability are needed | integration failure and value erosion | screening exposure under the Wet Vifo in sensitive sectors |

Digital and direct-to-consumer | demand is testable online | hidden unit economics across acquisition, returns and fulfilment | fulfilment space and service-level constraints |

The table shows there is no default answer. The mode that is cheapest to start rarely produces the best market understanding, and the mode that gives the most control is rarely the one that should be committed to first. The decision is a judgement about sequence, and the cost of getting it wrong concentrates in the modes that lock in fixed structure or external dependency before the company has learned enough to justify either.

Local Partner Search in the Netherlands: Access Is Not the Same as Control

A local partner is not a legal requirement for foreign companies operating in the Netherlands, and treating it as one is a common and expensive misunderstanding. The decision to bring in a partner is commercial, not regulatory, which means it should be justified by what the partner adds rather than assumed as a default step. A productive local partner search in the Netherlands does not begin with a list of candidate firms. It begins with a precise definition of the role the partner is expected to play, because only that definition makes it possible to judge whether a given partner is suitable. A partner may be needed for customer access, for distribution reach, for sector credibility, for logistics capability, for regulatory familiarity, for co-investment or for sharing operational risk. Each of those purposes implies a different kind of partner and a different contractual structure, and a search that has not specified the purpose tends to select for chemistry rather than for fit.

The risks in a partner-led entry are predictable and they follow a mechanism that is worth making explicit. When a partner holds the customer relationship, the foreign company sees the market only through the partner's reporting, which means its pricing, its demand signal and its understanding of customer behaviour are all mediated. Over time this can produce a company that has been present in the Netherlands for years without ever developing its own market knowledge, which is the opposite of what entry was supposed to achieve. Incentives drift apart as the partner optimises for its own portfolio rather than the entrant's growth, channel conflict emerges if the company later builds a direct presence, and an arrangement that was sensible at small scale becomes a constraint that is costly to exit. This is why a serious local partner search for foreign investors in the Netherlands should design learning rights, data access and exit options into the relationship from the beginning, rather than discovering their absence at the point when the company needs to take the market into its own hands.

Foreign Subsidiary Setup in the Netherlands: Legal Step or Operating Commitment?

The legal element of a foreign subsidiary setup in the Netherlands is the least demanding part of the decision. A Dutch private limited company, the BV, or a branch can be established without serious difficulty, and the choice between them is a question for tax and legal advisers that can be settled in a single conversation. Treating that step as the substance of the decision is where companies go wrong, because setting up a subsidiary in the Netherlands is far more an operating-model commitment than a legal one. The incorporation creates a structure that then has to be staffed, governed, funded and held accountable, and it is the weight of that structure, not the registration, that determines whether the subsidiary is an asset or a liability.

A subsidiary brings with it a set of standing obligations that begin the moment it is operational. Someone has to be hired and managed, a profit and loss account becomes the responsibility of named individuals, local decision rights have to be defined against what remains with headquarters, and a reporting rhythm has to be established and sustained. These commitments are precisely the territory of operating model redesign, because they determine how the entity is run rather than how it is registered, and they are where premature subsidiaries quietly accumulate cost. The Dutch context sharpens the point. With Eurostat placing the country among the highest labour cost economies in the European Union, every hire carries a heavier fixed burden than in many neighbouring markets, and recruitment is slower because of the labour shortages reported by Statistics Netherlands and the OECD. The talent calculation is also shifting, since the expat facility that has helped attract international staff, commonly known as the 30% ruling, is set to fall to a maximum of 27% from January 2027 according to the Dutch government's own guidance. The practical question is therefore not whether a Dutch subsidiary can be created, which it plainly can, but whether the business is ready to carry the cost, the decision rights and the reporting discipline that a subsidiary requires before its market hypothesis has been proven.

FDI Advisory and the Investment Climate: What Foreign Investors Should Actually Test

Discussion of foreign direct investment in the Netherlands tends to drift toward macroeconomic commentary, which is of little use to an operator. The question that matters for an investor is narrower and more practical: which of the country's constraints can actually change the operating case being underwritten. Framed that way, the relevant features of the investment climate for foreign investors in the Netherlands are not abstract attractiveness scores but concrete factors that affect timing, cost and feasibility. Grid connection timelines and permitting can delay a facility. Labour availability and cost can change the economics of a service operation. The availability of suitable physical space can determine whether a logistics plan is executable. These are the same supply constraints the OECD, the IMF and the United States Investment Climate Statement identify, and good FDI advisory work consists of testing them against the specific investment rather than reciting them in general.

There is also a regulatory dimension that has become more material and that any acquirer needs to assess early. The Netherlands now operates a national security screening regime under the Wet Vifo, the Act on Security Screening of Investments, Mergers and Acquisitions, which came into force in June 2023 and is administered by the Bureau Toetsing Investeringen. The regime is mandatory and suspensory for qualifying transactions in vital processes and sensitive technology, depending on the target's activities and the level of control or influence acquired, which means it can affect the timetable and the certainty of a deal, and it applies regardless of whether the investor is Dutch or foreign. For an acquirer this is a question of execution readiness rather than policy interest, and it sits alongside the transaction and holding-structure decisions that shape how an investment is held and governed. The essential discipline throughout is to distinguish reform from implementation and visible market activity from genuine investable readiness. A country can announce measures to relieve the grid while connections remain on a waiting list, and a market can look active while the conditions for a particular investment to perform are absent. The investor's job, supported by advisers, is to test which of those gaps applies to the case in front of them. Good market entry consulting in the Netherlands treats that test as the starting point of the investment case rather than as a check performed after the commitment has effectively been made.

How Market Entry Consulting in the Netherlands Reduces the Cost of a Wrong Entry

The value of market entry consulting in the Netherlands is easiest to see by looking at what it prevents rather than what it produces. A wrong entry is rarely a single dramatic mistake. It is usually a chain of reasonable-looking decisions made in the wrong order: a subsidiary created before demand was proven, a lease and a warehouse committed before the hub logic was tested, a partner given control of the customer relationship before the company understood the market, or an acquisition pursued for speed before integration capacity was assessed. Each of these converts a hypothesis into a fixed cost, and the combined effect is a standing structure that has to be funded whether or not the original assumption holds. The contribution of advisory work is to interrupt that chain at the points where cost becomes irreversible.

In practice it means a defined sequence of work before commitment, not after it. It means testing whether demand is real or merely visible, defining the role the country is meant to play, comparing entry modes against that role rather than against habit, and conducting a proper market entry risk assessment in the Netherlands that surfaces the partner, location and regulatory exposures before they are locked in. It means building a staged roadmap with explicit risk gates so that scaling, holding or changing the model becomes an evidence-based decision rather than a sunk-cost defence, and it means establishing the governance and reporting discipline that lets headquarters see what is actually happening in the new entity. Where an acquisition is on the table, it means commercial due diligence that examines the customer base and the integration path rather than only the financial statements. This is what market entry consulting for European companies in the Netherlands is for, and it is the substance behind the apparently simple question of how to enter the Netherlands market as a foreign mid-market company. The answer is not a checklist of legal steps. It is a sequence in which each commitment is justified by the evidence available at the point it is made.

Conclusion

The Netherlands will continue to reward foreign companies that decide what the country is for before they commit capital to it, and it will continue to expose those that mistake an easy registration for an easy market. The strengths are genuine and the formal steps are straightforward, which is exactly why companies commit fixed cost ahead of proof and treat a strategic choice as an administrative one. Sound market entry consulting in the Netherlands reverses that order. It begins with the role the country should play, lets that role determine the entry mode, the partner logic and the subsidiary decision, and stages the commitment so that the cost base grows only as the evidence does. Handled that way, the qualities that make the country attractive become the foundation of a profitable European position. Handled the wrong way, the same qualities become an expensive structure in search of a purpose, and the difference between the two outcomes is decided long before the first invoice is paid.

Considering an entry, expansion or acquisition in the Netherlands? Before committing to a subsidiary, a distributor or a transaction, test the role and the sequence first. Tretiakov Consulting works with owners, boards and investors on a structured market entry assessment that establishes the country's strategic role, compares the realistic entry modes and stages the commitment around defined risk gates.

Frequently asked questions

What is market entry consulting? Market entry consulting helps a company decide whether, why and how to enter a new country before it commits capital. In the Netherlands that means defining the country's strategic role, testing demand, comparing entry modes, weighing partner and subsidiary options, and sequencing investment around defined risk gates, rather than treating incorporation as the decision itself.

Is the Netherlands still a good place for a foreign mid-market company to enter Europe? It remains a strong choice for the right company with the right sequence, but it is no longer an automatic one. The EY Netherlands Attractiveness Survey recorded a fall to tenth place among European destinations for foreign investment in 2025, and the OECD and IMF point to grid congestion and labour shortages as real constraints. The advantages in logistics, law and talent are genuine, but the cost of an unsequenced entry has risen, so the decision should turn on how clearly the company has defined the country's role rather than on its general reputation.

Should we set up a subsidiary or work through a distributor first? The choice cannot be made in isolation. A distributor suits the testing of demand at low fixed cost but leaves the entrant without direct customer data, while a subsidiary gives control and direct learning at the price of standing fixed cost. The right answer depends on how much demand has been proven and how much control the strategy genuinely requires. Committing to a subsidiary before demand is demonstrated is the more common and more expensive error, particularly in a high labour cost economy.

Do foreign investors need a local partner in the Netherlands? No. A local partner is a commercial option rather than a legal requirement. It can accelerate access to customers, distribution and sector credibility, but it can also place the customer relationship and the demand signal in the partner's hands. The decision should follow from a precise definition of the role the partner is expected to play, with learning rights, data access and exit terms agreed at the outset rather than negotiated later under pressure.

How does the Wet Vifo affect an acquisition in the Netherlands? The Wet Vifo introduced a mandatory and suspensory national security screening regime that came into force in June 2023 and is administered by the Bureau Toetsing Investeringen. For acquisitions in vital processes or sensitive technology it can affect both the timetable and the certainty of completion, and it applies to Dutch and foreign investors alike. Where an acquisition qualifies as foreign direct investment in the Netherlands in a screened sector, that exposure belongs in the deal plan from the outset, because it is an execution-readiness issue rather than a policy matter to be considered afterwards.

What does the change to the expat ruling mean for staffing a Dutch entity? The expat facility known as the 30% ruling is set to fall to a maximum tax-free allowance of 27% from January 2027 under current Dutch government guidance, with transitional rules depending on the employee's start date. Combined with labour costs that Eurostat places among the highest in the European Union, it is a cost-planning factor that reinforces the case for proving demand before converting headcount into fixed structure.

What should a board ask before approving an entry into the Netherlands? A board should ask what role the country is meant to play, what evidence of demand supports that role, which entry mode follows from it and why, what converts to fixed cost and at what point, and what the defined risk gates are for scaling, holding or changing course. Those questions are the substance of any credible market entry strategy in the Netherlands rather than procedural detail, and if they cannot be answered clearly the proposal is not yet ready for approval.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.