Go-to-Market Strategy Consulting in Uzbekistan: Why Market Entry Is Not Market Access

Most foreign companies that examine Uzbekistan reach a similar conclusion at the first level of market screening. The population is large and young, the reform programme launched in 2017 has visibly opened the economy, and retail turnover has been rising at double-digit nominal rates. The market looks open, and in a formal sense it is. The difficulty that go-to-market strategy consulting in Uzbekistan is built to address is that legal entry, practical access and a defensible commercial position are three different things, and most entry plans treat them as one. A company can be legally permitted to sell, register an entity and appoint a national distributor, and still find a year and a half later that its product is not reaching the intended customer at a profit, because the binding constraint in this market is rarely demand. It is the executability of the commercial model, which turns on route-to-market, channel control, pricing and the discipline of the operating model rather than on the size of the population.

The commercial pressure: why Uzbekistan is on every mid-market shortlist

The pull is genuine, and it is worth stating precisely before qualifying it. Uzbekistan has a population approaching forty million, the largest in Central Asia, with a demographic profile weighted towards younger consumers who are forming brand preferences and entering their higher-spending years. Household consumption has grown, and the official figures published by the Statistics Agency under the President of the Republic of Uzbekistan show retail turnover expanding year on year. For a mid-market business in consumer goods, industrial products or distribution, that combination is exactly the structural demand that justifies a business expansion strategy in Uzbekistan rather than a purely opportunistic export relationship, and it is why serious work on market entry in Uzbekistan is back on so many shortlists. The World Bank Group's Country Private Sector Diagnostic reinforces that pull, identifying consumer-facing sectors such as retail and food and beverage among the areas where private investment can play a larger role, though a sector being flagged as an opportunity is not the same as that opportunity being immediately bankable.

The qualification matters more than the headline. The World Bank's Country Economic Memorandum for Uzbekistan, published in 2025, reads the same growth far less comfortably than a turnover chart suggests. It finds that per-capita output rose at an average of roughly 4.2 per cent a year between 2010 and 2022, but that the growth was driven largely by capital accumulation rather than by productivity gains, and that the private sector remains underdeveloped relative to the size of the economy. The same analysis notes that although the trade-to-GDP ratio more than doubled to around 71.6 per cent by 2022, only about six per cent of domestic firms actually export. That is not the profile of a mature, competitive commercial ecosystem. It is the profile of an economy that has opened its doors faster than its firms have learned to compete through them.

For a foreign entrant, the practical reading is more demanding than the headline, because the figures point in different directions once they are set against one another. A large, young population alongside double-digit nominal retail growth describes potential demand rather than serviceable demand, since most of that turnover still moves through channels a foreign company cannot easily reach or control. Rapid trade openness alongside an exporting base confined to a small minority of firms describes an economy that has opened faster than its companies have learned to compete. Growth that has leaned on capital accumulation rather than on productivity describes investment, not yet competitiveness. Taken together, the same indicators that build the investment case also mark its limit: demand exists, but the commercial infrastructure that normally converts demand into reliable revenue, meaning organised distribution, modern retail, competitive logistics and verifiable customer data, is thinner than the macro numbers suggest. Any growth strategy for companies entering Uzbekistan that treats the population figure as a proxy for an addressable market will overstate the opportunity and understate the cost of reaching it, which is the point at which a disciplined commercial strategy in Uzbekistan separates from an optimistic one.

What a go-to-market strategy actually has to solve here

It is worth being precise about what a go-to-market strategy is in this environment, because the term is used loosely and the looseness is expensive. A go-to-market strategy is best understood as a decision architecture rather than a slogan: it determines how a specific product reaches a specific customer at an acceptable cost, who physically moves and sells it, how it is priced along the chain, and how the company retains enough control to defend its margin and its customer relationship over time. A marketing strategy sits inside that architecture and addresses demand creation, positioning and communication. The difference between a go-to-market strategy versus a marketing strategy is commercial rather than semantic, because a company can run a capable marketing programme in Uzbekistan and still fail when the binding constraint sits in the physical and contractual path to the customer rather than in awareness.

That path is where the work concentrates. Route-to-market is the architecture by which goods and the commercial relationship travel from the company to the end customer, including the choice of importer, distributor, wholesaler, modern-trade account or direct model, and the terms that govern each link. In a market with deep, organised distribution, this architecture is close to a given. Here it is the principal design problem, which is why a route-to-market strategy in Uzbekistan deserves more board attention than the entity structure or the marketing budget that usually dominate entry discussions. For the same reason, a credible go-to-market strategy for foreign companies in Uzbekistan has to begin with the channel as it actually exists, not with the channel the company is accustomed to serving elsewhere.

A go-to-market strategy framework that survives the channel

A workable go-to-market strategy framework for this market forces four questions in sequence rather than in parallel. First, is the demand for the category real and, more importantly, reachable through a channel the company can actually use. Second, can the product physically reach that customer at a landed cost that leaves a defensible margin, which is the route-to-market question. Third, who will control pricing, customer data and the customer relationship once volume starts to flow. Fourth, will the resulting revenue convert into governed, repatriable margin rather than trapped working capital. The reason to sequence these, and the reason the question of how to build a go-to-market strategy is really a question of order, is that a failure at the second or third question cannot be rescued by effort at the first. Companies that begin with demand sizing and treat distribution as an implementation detail often find that the detail was, in fact, the strategy.

Route-to-market reality: distribution in a doubly landlocked, bazaar-led market

The physical reality of distribution here is shaped by two facts that no commercial plan can argue away. The first is geography. Uzbekistan is one of only two doubly landlocked countries in the world, meaning every import crosses at least two borders before it arrives, and the regional transport network it depends on is still being modernised. The Asian Development Bank's Country Partnership Strategy for 2024 to 2028 describes a sustained programme of investment in the road and rail corridors that connect the country through the Central Asia Regional Economic Cooperation framework, together with work on customs and trade facilitation. The important word in that description is programme. The corridors are improving, but improvement that is under construction is not the same as connectivity a company can rely on this quarter, and the World Bank's logistics performance work has long noted that landlocked economies cannot remove transit inefficiency through domestic reform alone. For a route-to-market strategy for industrial companies in Uzbekistan, where shipments are heavy, time-sensitive or temperature-controlled, this translates directly into longer lead times, higher safety stock, more expensive landed cost and a smaller set of regions that can be served economically at all.

The second fact is the structure of the selling channel itself. The official trade statistics show that small businesses and unorganised trade account for the overwhelming majority of retail turnover, in the order of four-fifths, while the number of large retail enterprises remains a few hundred against tens of thousands of small traders and microfirms. Modern organised retail, the format a European or Gulf brand is built to serve, is comparatively thin and concentrated in Tashkent and a small number of regional centres. This is the single most underestimated feature of the market. A distribution strategy in Uzbekistan that assumes shelf space can simply be bought, that listing economics resemble those of an organised grocery sector, or that point-of-sale data will be available, is designing for a channel that does not yet dominate. A distribution strategy for foreign brands in Uzbekistan has to be built for the bazaar and the small independent trader as the primary route, with modern trade as a secondary and growing one, rather than the reverse.

These two facts combine into the failure that recurs most often, and it is worth describing as a mechanism rather than a warning. Faced with fragmented coverage and difficult logistics, a foreign company appoints a single national distributor who promises reach. The distributor delivers volume quickly, which appears to validate the decision, and within a year controls the pricing to trade, owns the relationship with the customer, and holds the only reliable data on where the product actually sells. In effect, the company has bought coverage and ceded much of its commercial independence in the same contract. Recovering from that position is slow and expensive, because the distributor now has every incentive to keep the principal dependent. This is why retail strategy consulting in Uzbekistan, and any serious view of the retail market strategy in Uzbekistan, begins with channel control as a design constraint rather than as something to negotiate later. Sound sales channel optimisation in Uzbekistan is, at root, about retaining the right to reach the customer through more than one route from the outset.

The hidden friction: currency, the state's footprint and channel control

Beyond the physical channel sits a layer of friction that rarely surfaces in a market-sizing exercise and tends to surface only in the second year of operation. The first element is currency. Uzbekistan liberalised its foreign-exchange regime as part of the 2017 reforms, and the OECD's 2025 investment policy roadmap records substantial modernisation of the legal framework, including the reform of currency regulation and a more transparent law on investment. Liberalised, however, is not the same as frictionless. The International Monetary Fund's 2025 Article IV consultation describes an economy that is performing well, with real growth of around 6.5 per cent in 2024 and reserves at comfortable levels, but it also describes inflation that remained close to ten per cent in early 2025 and a monetary stance that the Central Bank of Uzbekistan has held deliberately tight in response. For a foreign company, the practical consequence is that exchange-rate management, the timing and mechanics of converting and moving funds, and the cost of holding local-currency receivables are not treasury afterthoughts. They are inputs to the commercial model that change pricing, payment terms and the cash cycle. A commercial strategy for foreign-owned companies in Uzbekistan that ignores them will report margins on paper that it cannot reliably realise in hard currency.

The second element is the continuing weight of the state in the economy. The European Bank for Reconstruction and Development's country strategy for 2024 to 2029 sets reducing that weight as a central objective, prioritising the transformation and governance of state-owned enterprises, privatisation and a better business climate, while the World Bank's Systematic Country Diagnostic identified the state's footprint as the principal structural constraint on private-sector growth. For a commercial entrant the relevance is concrete rather than ideological. In categories where state-owned or state-linked enterprises remain significant, they shape pricing, occupy parts of the distribution chain and influence which counterparties are available and on what terms. This is not an argument against entry. It is an argument for mapping, category by category, where the state still sits in the value chain before committing to a channel design that assumes a level competitive field.

Taken together, currency friction and state presence explain why a credible commercial strategy in Uzbekistan has to model the cash cycle and the competitive structure of each category, rather than relying on a single national assumption. They also explain why the most damaging errors are not made at entry but a year later, when a model that looked sound on a spreadsheet meets a payment delay, a receivable that is slow to convert, or a state-linked competitor that does not price the way a private one would.

From market activity to revenue: building a commercial operating model that executes

The shift that separates companies which build a real position from those which stall is the move from thinking about entry to thinking about a commercial operating model. This is the substance of commercial transformation in Uzbekistan, and the phrase deserves to be used precisely rather than as a label. Commercial transformation for mid-market companies in Uzbekistan means redesigning how the commercial engine is structured, staffed, governed and measured so that it can convert access into revenue under the specific conditions described above, rather than importing a model built for an organised European market and hoping it adapts.

Three operating realities tend to surface once volume begins. The first is key-person dependency. Early commercial success in this market usually rests on one local general manager or a single distributor relationship, and the knowledge of how the market actually works, meaning which trader pays, which route clears customs cleanly, which account is worth the credit risk, sits in that individual's head rather than in any system. That is a governance exposure, not a convenience, and it is precisely the kind of dependency that a buyer in a later transaction will price heavily. The second is reporting. Commercial data often arrives through the distributor, which means the company is steering by numbers it cannot independently verify, and sales transformation in Uzbekistan frequently begins with the unglamorous work of building a direct line of sight to sell-out and to customer-level performance. The third is the cash cycle, where extended terms, local-currency exposure and slow collection quietly consume the working capital that the growth case assumed would be available.

Addressing these is what commercial excellence actually means in practice. Commercial excellence is the disciplined, repeatable conversion of market access into governed and predictable revenue, and in this market it depends less on sophisticated demand generation than on control of channel, data and cash. The same logic underpins revenue transformation for B2B companies operating here, where the durable gains come from pricing discipline, channel design and collection rather than from volume alone. A useful way to hold the whole picture together is to separate, deliberately and honestly, the market signals that attract entrants from the operational realities beneath them.

Signal that attracts entrants | Operational reality beneath it | Implication for the go-to-market model |

|---|---|---|

A large, young and growing population | Demand is concentrated geographically and served largely through informal channels | Reachability, not population, sets the realistic revenue ceiling |

Visible reform and liberalisation since 2017 | Reform announced is not the same as reform implemented at the level of a single firm | Plan for residual friction, not for a finished market |

Double-digit nominal retail growth | Nominal figures are inflated by high inflation; real volume growth is lower | Build the forecast on real volume, never on nominal turnover |

An open and modernised investment regime | Currency is liberalised but not frictionless | Treat foreign exchange and repatriation as commercial inputs to pricing and the cash cycle |

Distributors offering immediate national coverage | Coverage is bought at the cost of pricing control, data and the customer relationship | Design channel control before any partner is appointed |

Read down the third column and the design brief becomes clear. The work is not to chase the signal but to build the operating model that the reality requires, which is precisely where a credible operating model redesign connects commercial ambition to execution on the ground.

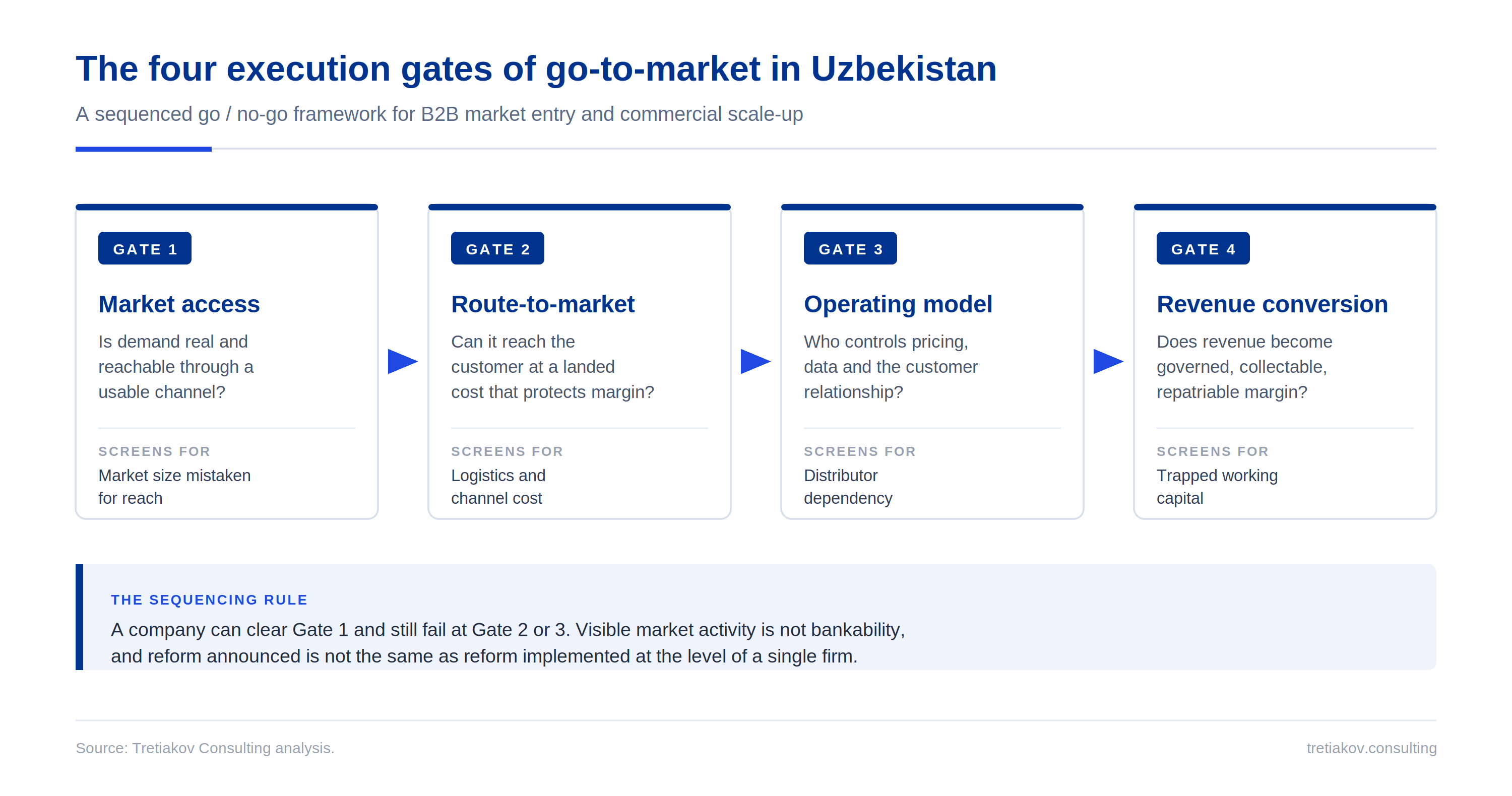

A practical assessment framework for go-to-market strategy consulting in Uzbekistan

This is where go-to-market strategy consulting in Uzbekistan earns its place, because the value is not a market report but a sequence of decisions taken in the right order, with the right evidence behind each one. The framework we apply treats entry as four execution gates rather than as a single go decision, and the discipline lies in refusing to pass a gate until the prior one has genuinely cleared.

The discipline lies in the sequence. Each gate is a genuine go or no-go decision, and the order cannot be rearranged. A company can clear market access comfortably and still fail on the second gate, where the realities of a doubly landlocked, bazaar-led channel determine whether a route-to-market strategy in Uzbekistan can actually deliver margin, or on the third, where pricing, data and the customer relationship are won or lost. That is the reason visible market activity must never be read as bankability, and the reason a weakness at the second or third gate cannot be recovered by additional effort at the first. Used in this way, the sequence is what makes commercial transformation in Uzbekistan executable rather than aspirational.

This gated logic is what turns growth strategy consulting from commentary into something a board can act on, and it is the backbone of any serious B2B growth strategy in Uzbekistan. It is also what the more durable growth strategy examples have in common across markets like this one: they are sequenced, they test the hardest constraint early, and they treat channel control and cash conversion as first-order design choices rather than as later refinements.

For an investor or an acquirer, the same four gates double as a diligence lens, which is why this analysis sits naturally alongside the questions foreign capital should ask before investing in Uzbekistan: whether a commercial story rests on a defensible model or on a single relationship, and whether reported revenue would survive the loss of one distributor or one general manager. A company already present in the market and recognising itself in the failure modes above is usually a candidate for a focused B2B growth strategy in Uzbekistan, rebuilding its distribution around channel control, verified data and pricing discipline before it chases further volume.

Conclusion

The opportunity in Uzbekistan is real, and so is the direction of reform, which is precisely why the market rewards discipline rather than enthusiasm. The companies that build durable positions are the ones that treat go-to-market strategy consulting in Uzbekistan as the design of an executable commercial model, sequenced through the gates above, rather than as the announcement of an entry. They size demand by what they can actually reach, they settle route-to-market and channel control before they scale spend, and they treat currency and cash conversion as commercial inputs rather than as treasury details. The next two to three years represent a positioning window, because modern distribution remains thin and defensible channel positions are still available to those willing to build them properly, whereas they will become more expensive to secure once organised retail and logistics mature. Firms that move with that sequence in mind will hold positions worth defending, while those that mistake an open market for a finished one will spend the same period discovering why the two are not the same. The most useful first step is to test the commercial model against these realities before capital is committed, and that assessment is where our work with new entrants most often begins.

Frequently asked questions

We can see the demand. Why do experienced operators still treat Uzbekistan as a difficult market to execute in? Because demand is not the binding constraint, and the structural reasons that go-to-market strategy consulting in Uzbekistan exists do not resolve with a single strong year. Organised distribution is thin, the country is doubly landlocked and still dependent on transport corridors that are being upgraded, most retail moves through bazaars and small traders, currency is liberalised but not frictionless, and the state retains weight in several categories. Each of these sits between the company and the customer, so the difficulty lies in reaching and serving demand profitably while keeping control of the relationship, not in finding demand.

What is route-to-market, in practical terms, and why is it the decision that matters most here? Route-to-market is the architecture that carries both the product and the commercial relationship from the company to the end customer, including who imports, who distributes, who sells, and on what terms. It matters most because the wrong design is the hardest mistake to reverse. A company that appoints a single national distributor for speed of coverage usually surrenders pricing, data and the customer relationship in the same agreement, and the distributor then has every incentive to keep it dependent. The decision looks like logistics; it is actually about who owns the customer.

How does a go-to-market strategy differ from a marketing strategy when the channel is this fragmented? The difference is consequential rather than semantic. A marketing strategy creates and shapes demand; a go-to-market strategy decides how that demand is served, controlled and converted into governed revenue. In a market with thin modern retail, the go-to-market strategy versus marketing strategy distinction becomes a question of value capture, because excellent demand creation feeding a channel the company does not control simply transfers that value to the intermediary. The marketing spend performs, and the principal still loses the economics it created.

What is commercial excellence in a market with limited organised retail and real currency friction? It is the disciplined and repeatable conversion of access into predictable, collectable, repatriable revenue. In more developed markets commercial excellence leans heavily on demand generation and sophisticated marketing. Here it leans on control of the channel, independent visibility of sell-out data, pricing discipline through an informal chain, and active management of the cash cycle. The companies that achieve it are rarely the ones with the largest marketing budget; they are the ones that designed for control before they scaled.

How should an investor read the reported revenue of a target already operating in Uzbekistan? With particular attention to what the revenue depends on. Strong reported numbers that rest on a single distributor relationship, a single general manager, or data the company cannot independently verify are fragile in ways that a standard model will not capture, and they should be priced accordingly. The right test is whether the commercial model would survive the loss of any one of those dependencies. That is the same logic that governs an investment-readiness assessment and a serious commercial due diligence, and it is why visible market activity should never be read, on its own, as evidence of a bankable position.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.