Commodity Trading Governance in Switzerland

Switzerland still retains most of the functions that made it one of the leading global hubs for physical commodity trading. Trade finance is structured along Lake Geneva, large counterparties are managed from Geneva, Zug, Lugano and Lausanne, and the supporting cluster of banks, lawyers, surveyors, insurers and arbitrators remains deep and rehearsed. What has changed since February 2022 is the regulatory and reputational perimeter around that activity. SECO is using enforcement tools it had held for years, the supply-chain perimeter has widened across Swiss and European law, and Dubai has matured into a credible alternative for the more mobile parts of the trading model. Commodity trading governance in Switzerland is no longer a back-office discipline organised around a single sanctions officer and an annual compliance review. Board oversight in Swiss commodity trading houses has had to catch up faster than internal architecture allows, leaving a governance gap that owners cannot close by hiring another compliance manager.

Sanctions exposure is now a first-order board risk

The legal framework is not new. The Federal Act on the Implementation of International Sanctions (Embargo Act, SR 946.231) has been in force since 2003, and the Ukraine Ordinance has implemented Russia-related restrictions since the first week of the war. What is new is the operational posture of the State Secretariat for Economic Affairs. On 21 November 2022 SECO issued its first summary penalty order under the Ukraine Ordinance, and in February 2024 referred two commodity trading investigations to the Office of the Attorney General with a third still open. These are not headline fines on the European scale, but they signal a clear change in posture.

Under Article 9 of the Embargo Act, intentional breaches expose individuals to a custodial sentence of up to one year combined with a monetary penalty under the Swiss Criminal Code, rising to five years in serious cases. Article 10 misdemeanours, including refusal to cooperate with SECO, carry fines of up to CHF 100,000, reduced to CHF 40,000 for negligence. Legal entities can be prosecuted under Article 102 of the Criminal Code where organisational failings prevent attribution to an individual. The CHF 540,000 figure that circulates in industry commentary derives from the Criminal Code's daily-penalty-unit formula rather than a statutory cap, and should be treated accordingly.

The Anti-Money Laundering Act adds a layer that is often misunderstood. Switzerland does not licence physical commodity trading and the Swiss Financial Market Supervisory Authority does not supervise traders as such. AMLA applies only where the trader performs financial-intermediary activity on a professional basis, at which point FINMA authorisation or affiliation to a recognised self-regulatory organisation becomes mandatory. The indirect bite matters more: Swiss trade-finance banks apply Wolfsberg-style know-your-counterparty and source-of-funds standards through the entire transaction chain, and a trader that cannot meet those expectations loses access to the credit lines that underwrite its business model. Sanctions screening, beneficial-ownership tracing on counterparties and vessels, price-cap attestation flows and group-level reviews of foreign subsidiaries now sit on the board agenda. Effective sanctions compliance for commodity traders in Switzerland begins with a control-environment diagnostic, not a policy refresh.

The supply-chain perimeter has moved beyond the Swiss border

The Swiss layer is operationally settled. Articles 964j to 964l of the Swiss Code of Obligations, together with the Ordinance on Due Diligence and Transparency in relation to Minerals and Metals from Conflict-Affected Areas and Child Labour, have applied since 1 January 2022, with first reports filed in 2024 for financial year 2023. Scope covers 3TG minerals (tin, tantalum, tungsten and gold) placed in free circulation or processed in Switzerland from conflict-affected or high-risk areas, and any company offering products or services where a reasonable suspicion of child labour exists. SME exemptions limit the child-labour limb below DDTrO thresholds for balance sheet, turnover and employees, while conformity with the OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas provides an Article 964j paragraph 4 exemption from the Swiss reporting limb. Article 325ter of the Criminal Code criminalises false statements in the report, with fines of up to CHF 100,000 attaching to the responsible board members.

The European layer is more often misrepresented than understood. The Corporate Sustainability Due Diligence Directive(Directive (EU) 2024/1760), as amended by Directives 2025/794 and 2026/470, does not apply automatically to every Swiss trader selling into the European Union. After the 2026 amendments, direct application to non-EU groups requires more than EUR 1.5 billion of net turnover generated in the Union, with substantive obligations from 26 July 2029. For most Swiss commodity traders the meaningful exposure is contractual rather than direct, because in-scope EU customers will cascade supplier code, audit and remediation obligations through purchase agreements long before the directive itself reaches the trader. Supply chain due diligence for Swiss commodity traders is therefore shaped by procurement clauses as much as by statute.

What stays in Switzerland, what migrates to Dubai

The Geneva–Dubai conversation becomes useful only once it is disaggregated. Some functions are difficult to relocate, others are mobile by design.

Structured trade finance is the function most firmly anchored in Switzerland. The bank-syndication ecosystem along Lake Geneva, with its borrowing-base structures and transactional facilities, has been built over decades and is not replicated quickly. Swiss contract law, the predictability of arbitration under the Swiss Rules and the depth of the specialised bar give counterparties to large physical contracts a certainty that few alternative jurisdictions match. Insurance, inspection, collateral management and the senior advisory layer remain concentrated in the Geneva and Zug clusters, and complex counterparty management with sovereign and state-owned producers continues to draw on Swiss neutrality as a commercial asset. Governance in Geneva and Zug commodity trading hubs depends on these anchored functions, which is why most owners do not relocate the entire group.

The mobile layer is different. Booking entities for Russia-linked flows moved faster than institutional functions: by July 2023 the share of Russian crude purchased by Swiss-registered traders had fallen from 47 per cent to 5 per cent, with UAE-registered non-state traders accounting for 51 per cent and Hong Kong-registered entities for a further 30 per cent. Talent has followed, with around 750 to 1,000 new commodity-sector roles created in the UAE since 2020 and mid-office, operations and trade-technology functions increasingly moving with the front office. The Dubai Multi Commodities Centre has reported a 30 per cent rise in Swiss company registrations over two years, taking the total above 400 Swiss-incorporated businesses in its free zone. The Geneva to Dubai migration of commodity trading functions is therefore not a clean relocation story; it is a redistribution of activities across two control environments.

A Swiss-domiciled group is therefore increasingly likely to run a dual-hub operating model: one booking centre in Switzerland and another in Dubai, two regulatory perimeters, two compliance cultures and a single consolidated board accountable for both. This is the governance problem that hides behind a tax or HR conversation, and the one our work on operating-model redesign and interim management is most frequently asked to address.

Geneva–Zug and Dubai: where the functions sit

Function | Geneva, Zug, Lugano | Dubai (DMCC, DIFC) |

|---|---|---|

Structured trade finance | Deep bank syndication, established borrowing-base practice | Growing, smaller correspondent ecosystem |

Trader and mid-office talent | Senior commercial leadership, institutional memory | Mid-career inflow; 750–1,000 new sector roles since 2020 |

Legal infrastructure | Swiss contract law, Geneva and Zurich arbitration | DIFC common-law courts, arbitration developing |

Arbitration | Swiss Rules and ICC seat in Geneva, mature practice | DIFC common-law base, DIAC (succeeding DIFC-LCIA) |

Banking relationships | FINMA-supervised trade-finance banks | Regional and international banks, lighter regime |

Compliance burden | EmbA, AMLA via banks, Art. 964j ff. CO, CSDDD cascade | UAE AML/CFT, UBO reporting, no automatic EU alignment |

Tax structures | Cantonal regimes, competitive effective rates | 0% on qualifying free-zone income, 9% federal CIT |

Counterparty management | Established for sovereign and state-owned producers | Growing for regional flows |

The table is descriptive rather than prescriptive. It shows where each function currently has the strongest centre of gravity.

The governance gap inside Swiss trading houses

Operating model pressure on Swiss trading firms is now visible in the gap between trading capability and oversight capability. The internal architecture of many Swiss groups still reflects the firm they used to be rather than the firm they have become. Founder-era or banker-heavy boards often lack the trading-risk literacy needed to oversee value-at-risk, mark-to-market exposure, counterparty concentration and physical-logistics risk. Swiss commodity trading risk management remains anchored in the judgement of the CEO, the head trader or a small inner circle, rather than in systematic limits, real-time exposure dashboards and a segregated risk veto authority. Compliance programmes designed for an earlier oil-and-metals product mix are now stretched across LNG, power, biofuels, carbon, agricultural commodities and mineral concentrates without a proportionate increase in capability.

Counterparty credit risk governance for commodity traders is where the gap turns commercial. Large physical positions, off-take prepayments and structured trade finance create exposures that are not always priced, limited or reported with the discipline expected of a bank trading book. Concentrations in sanctioned-adjacent jurisdictions are particularly exposed, and the dual-hub model multiplies the surface area without automatically multiplying the controls. The recurring failure modes are familiar: a weak risk committee, risk reports that read as activity logs rather than exposure analyses, no scenario or stress framework worth the name, no independent directors with sector expertise, and sanctions and supply-chain reporting that climbs through general counsel rather than into the board through a defined committee. The pattern is familiar from our work on independent oversight in high-stakes decisions.

A framework for commodity trading governance in Switzerland

A workable response has four reinforcing components rather than a sequenced plan. Board composition needs at least two independent non-executive directors with trading-risk literacy across physical commodities, derivatives hedging, structured finance and sanctions practice, recruited from outside the firm's banking and audit relationships so that genuine challenge is preserved. A risk committee with real authority needs a charter, an independent chair and a direct line to the chief risk officer, with explicit mandate over market, credit, counterparty, sanctions, AML and supply-chain risk, and must receive exposure data rather than narrative comfort. A multi-jurisdictional compliance infrastructure must cover the Swiss layer (Embargo Act, AMLA where it applies, Articles 964j ff.), the European layer (CSDDD cascade, EU sanctions, the Deforestation and Forced Labour Regulations), the United States layer (OFAC and the oil price cap) and the UAE layer (DMCC and DIFC AML and UBO requirements), with one shared taxonomy and one escalation path. An operational risk function needs counterparty and vessel screening, beneficial-ownership tracing, real-time exposure monitoring and an internal-audit cycle that tests controls rather than documenting them. Together these four components turn Swiss commodity trading risk management from individual judgement into a system, and signal to banks, insurers and regulators that the firm has moved past founder-era governance.

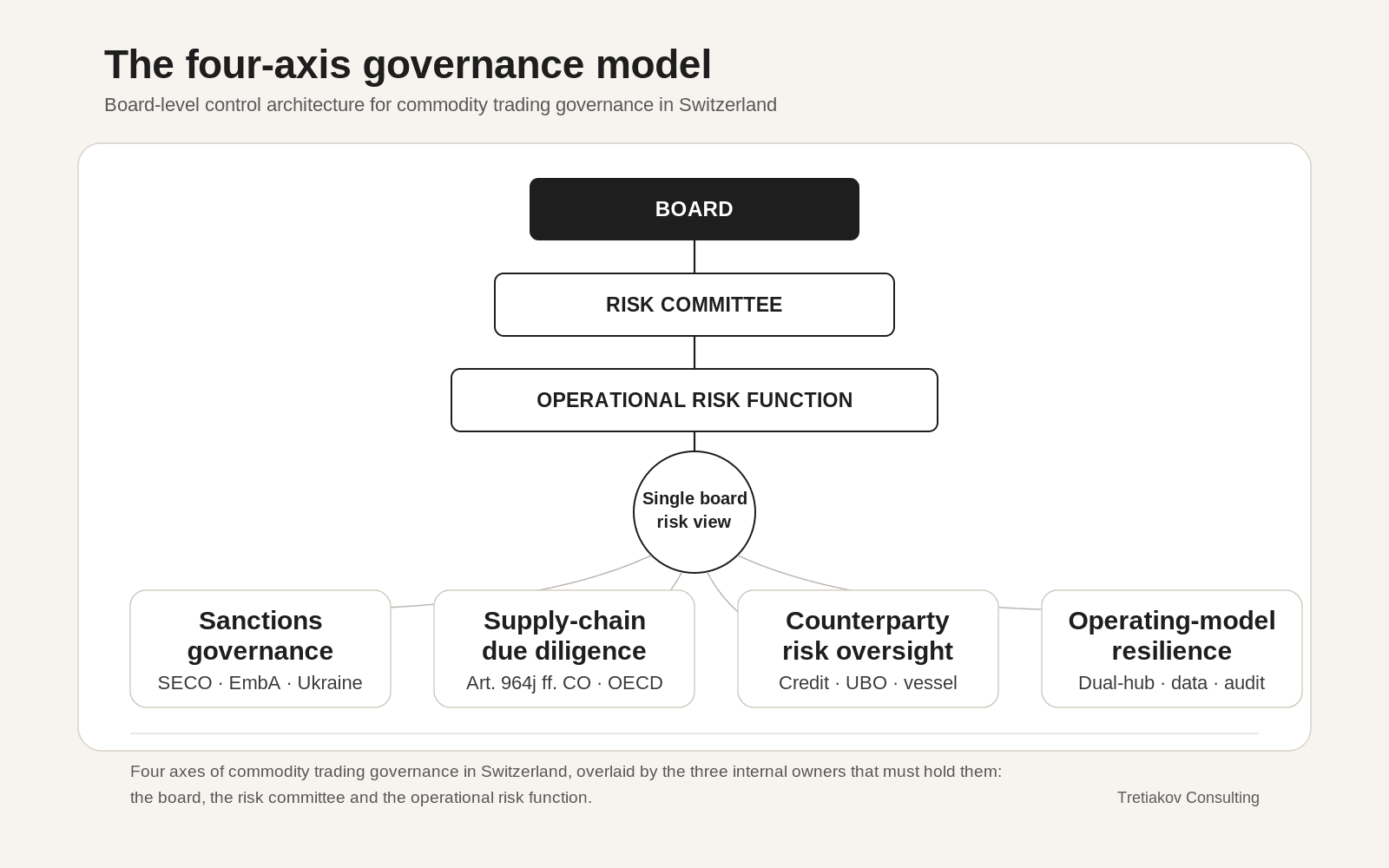

The four-axis governance model

The four axes of governance sit beneath three internal owners, monitored on their own metrics and feeding a single board-level view of the risk surface.

The board-level question

The question facing owners and chairs of Swiss commodity trading companies is not whether to remain in Switzerland. The structural advantages that matter for complex physical trading remain in Geneva, Zug, Lugano and Lausanne, and the substitutes are partial. The harder question is what the Swiss-based group needs to look like to operate confidently across Switzerland and Dubai simultaneously, under a regulatory perimeter that has widened and a counterparty environment that has hardened. Strengthening commodity trading governance in Switzerland before SECO, the trade-finance banks or an in-scope European customer forces the change is the cheaper option, and the one that preserves optionality for ownership and for any future transaction.

Our board advisory and governance support team works with owners, chairs and CEOs of Swiss-based trading groups on exactly this transition, alongside our broader Switzerland practice.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.