Business Optimisation for Swiss Manufacturing Companies

Capacity utilisation in the Swiss machinery, electrical and metals industry now sits at 80.7 percent, well below its long-term mean of 86.2 percent. Machine tool exports to the United States fell by 43 percent in a single quarter of 2025, and the franc has remained strong against both the euro and the dollar. The State Secretariat for Economic Affairs has revised Swiss GDP growth for 2026 to 1.0 percent. Business optimisation for Swiss manufacturing companies has, in this environment, stopped being a margin discussion. It has become an operating model decision.

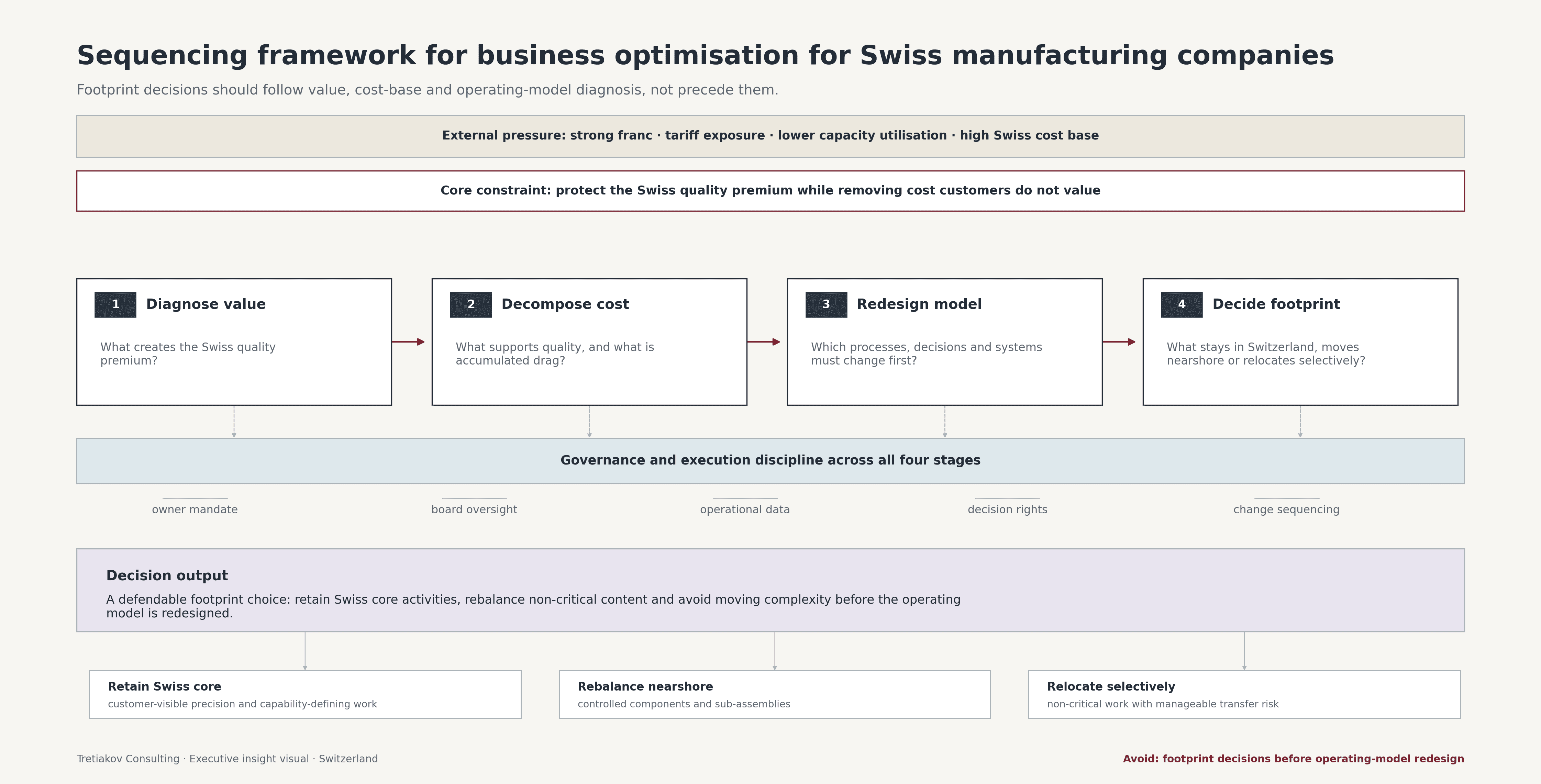

What follows is a framework for owners, boards and chief executives who need to protect the Swiss quality premium while removing the cost that has accumulated around it. The same precision customers pay extra for has, over decades, been wrapped in process layers, supplier relationships and overhead structures that no longer earn their place. Swiss manufacturing efficiency, in this reading, is less about running faster than about removing what the business no longer needs to carry.

The pressure is structural, not cyclical

The tariff path on Swiss goods illustrates the difficulty of treating any of this as a cycle. The 39 percent additional duty imposed on 7 August 2025 was reduced to 15 percent under the framework deal of 14 November, retroactive to mid-November. That brought Swiss exporters back into line with European competitors, but it did not unwind the damage already booked. Swissmem reports tech-industry exports to the US ended 2025 down 7.6 percent, with the fourth quarter alone falling 18 percent. The Federation of the Swiss Watch Industry closed the year at CHF 25.6 billion, a second consecutive annual decline.

The State Secretariat for Economic Affairs projects 1.0 percent GDP growth in 2026, below the long-term Swiss average of 1.8 percent, and the IMF in its most recent Article IV consultation treats persistent franc strength as a structural feature of the Swiss external position rather than a temporary deviation. When capacity utilisation runs this far below its long-term mean for an extended period, fixed-cost absorption deteriorates faster than variable savings can compensate. That is the mechanism converting what looks like a cyclical slowdown into a structural margin problem, and the point at which cost and performance optimisation for Swiss industrial businesses under tariff and FX pressure stops being optional.

Decomposing the Swiss cost base: what the customer is actually paying for

The first analytical step is to separate the cost base into three categories rather than treat it as a single number to be reduced.

Cost category | Examples in Swiss precision manufacturing | Customer value | Optimisation treatment |

|---|---|---|---|

Quality-supporting | Material grade selection, precision tooling, calibration regimes, final inspection, skilled-operator hours that directly produce tolerance | Directly visible in the product the customer pays a premium for | Protect; invest selectively |

Structurally necessary | Regulatory compliance, IP architecture, brand and certification investment, apprenticeship pipeline, governance | Indirectly visible; underpins long-term capability | Maintain; restructure, do not reduce |

Accumulated drag | Process complexity, redundant approvals, SKU sprawl, supplier proliferation, legacy systems, engineering specials without commercial rationale | Invisible to the customer | Remove; this is where the recoverable margin sits |

The pattern in most Swiss optimisation programmes is to attack categories one and two because they are visible and measurable, leaving category three largely intact because it is politically harder and operationally diffuse. The result is a thinner version of the same business rather than a redesigned one. The OECD economic survey of Switzerland makes a related point in its productivity diagnosis: structural improvement requires changing how work is organised, not simply doing less of it. Swiss production cost competitiveness moves only when the third category is genuinely addressed.

Business optimisation for Swiss manufacturing companies: the operating model levers that work

Four levers move the line, but only when applied in sequence rather than in parallel. This is where operating model redesign for Swiss industrials departs from generic cost programmes.

Automation calibrated to high-mix low-volume

Imported high-volume automation playbooks fail on Swiss shop floors because batch sizes are too small and the binding constraint is changeover discipline rather than run rate. The Swiss robotics and machine-vision ecosystem, anchored by ABB, Stäubli and a deep university spin-out base from ETH Zurich and EPFL, is a real enabler. The condition for success is sequence. Capital deployed into an unimproved process locks the inefficiency in steel.

Lean adapted, not imported

Lean works in Swiss precision when adapted to high-mix low-volume cadence. SMED, cellular flow and visual management retain their value; takt-time logic borrowed wholesale from automotive does not. The most common failure mode is a Swiss plant applying a template from a 50,000-unit run to a batch of 47 components with five engineering revisions in process. Precision manufacturing optimisation requires templates designed for the cadence in the building, not adapted from a different industry.

Supply chain rebalancing without quality erosion

The sourcing decision worth making is between intrinsically Swiss content, including specific surface finish, in-house calibration and tolerance regimes that depend on adjacent Swiss capability, and content sourced locally only by inertia. In well executed programmes a meaningful share of non-critical machined parts and sub-assemblies can be moved without the end customer noticing. The screening protocol matters more than the savings target.

Overhead and process simplification

Swiss overhead carries deep functional expertise alongside slow decision cycles, parallel reporting and IT architecture layered over twenty years. The lever is rarely headcount. It is decision rights and process design. Headcount reductions that follow process redesign hold; those that precede it return within eighteen months. Swiss manufacturing efficiency improves only when the process improves first.

The harder question: Swiss footprint or distributed footprint?

A component or assembly becomes a candidate for production outside Switzerland when three conditions hold: the precision requirement can be matched at the candidate site with controlled investment, the customer does not value or perceive Swiss content for that element, and the transfer can be executed without disrupting the Swiss-side capability that anchors the brand.

The realistic options sit on a familiar spectrum. EU-adjacent sites in Germany, France, Czechia or Poland offer short logistics and established quality cultures with a euro cost base. Romania and Hungary deliver materially lower labour cost at the price of a longer ramp-up. The United States has been reshaped by the November 2025 framework agreement, under which Swiss companies pledged approximately USD 200 billion of direct investment by the end of 2028. That commitment is producing real pharmaceutical capacity, but for mid-sized industrials the question is whether American production presence is a tariff hedge or a strategic distraction.

The failure pattern is not the offshoring decision itself. It is the absence of a sustained mechanism to hold quality across multiple sites: supplier audits, calibration discipline, retained Swiss-side engineering authority and transfer-pricing architecture that survives both audit and litigation. The early 2026 Swissmem survey reports that 88 percent of tech-industry companies invested in Switzerland in the past three years and 81 percent plan to invest there in the next three. Footprint expansion at home and selective offshoring abroad are sequenced badly more often than they are decided badly. Footprint decisions for Swiss manufacturers facing margin compression therefore belong inside the operating model conversation, alongside industrial investment and scale-up projects where capital and operating model questions must be answered together.

Where Swiss manufacturers fail at optimisation, and why

Sequencing is the first failure. Companies launch automation projects before process redesign, and capital expenditure precedes operating model clarity. The result is faster execution of an unchanged process.

Governance friction is the second. Family-held Swiss industrials often combine an engaged owner, a professional CEO and a technically experienced board where decision authority on the operating model is ambiguous. Programmes stall not at analysis but at the moment of cross-functional commitment. Swiss production cost competitiveness erodes invisibly during that pause.

Key-person dependency is the third. Decades of in-house craftsmanship concentrate critical knowledge in a small number of operators and engineers. Programmes that fail to map and protect this dependency create execution risk that no spreadsheet captures.

Systems fragmentation is the fourth. ERP, MES, PLM and quality systems often run in parallel with limited integration. Real-time visibility of cost-to-serve at SKU level is rare. Optimisation that runs on monthly closes rather than daily data flow misses targets consistently.

The fifth is harder to name. It is the senior engineer who explains, in good faith and with technical authority, why a lever that worked in Germany or Sweden cannot work in Switzerland. The explanation is sometimes correct. More often it signals an assumption inside the operating model that has accumulated authority no longer surviving scrutiny. Precision manufacturing optimisation depends on identifying which of these explanations is which.

The role of external advisory

The value an external adviser brings into Swiss precision manufacturing is not best-practice benchmarking. Swiss leaders already know their numbers and their competitors. The value is operating-pattern comparison across other industries and jurisdictions, applied to test assumptions internal teams cannot test alone. It is the discipline of decomposing the value proposition before touching the cost base, and the governance neutrality required to put the footprint question on the table without political cost inside the family, the board or the executive committee. Programmes that combine internal operational depth with external comparative judgement deliver materially better results than either alone, particularly across industrials and manufacturing where institutional memory is deepest and where operating model redesign for Swiss industrials therefore meets the most resistance.

Conclusion

The Swiss manufacturers that come through 2026 to 2028 with their quality premium intact will be those that decomposed the cost base before touching it, redesigned the operating model before deploying capital, and made footprint decisions deliberately rather than reactively. Pricing actions, FX hedges and short-time working will remain available, and none changes the underlying structure. Business optimisation for Swiss manufacturing companies is, at its core, the act of separating what the customer actually values from what the business has accumulated around it, then organising the operating model around the first and removing the second. Improving efficiency in Swiss precision manufacturing operations is, in practice, a sequence of decisions, each of which has to survive the next. The companies that hold that discipline will keep the position they spent decades building. Those that delay it will find the market has done the work for them, on terms they would not have chosen. This is the substance of business transformation and operating model redesign work in Switzerland at this point in the cycle.

Tretiakov Consulting works with Swiss industrial owners, boards and chief executives on operating model reviews, footprint decisions and transformation sequencing. If a programme of this kind is on your agenda, we are open to a confidential preliminary conversation.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.