Banking Sector Transformation in Uzbekistan

Banking sector transformation in Uzbekistan is moving the country's financial system away from a state-directed lending model towards a more commercially disciplined banking market. The reform agenda is no longer primarily about regulatory architecture or even ownership change; it is about whether individual banks can convert reform pressure into governance discipline, risk-based lending, operational efficiency and credible investor readiness. For banking executives, board members and international investors, the decisive question is not whether reform is happening, but whether each institution is being rebuilt from the inside in a way that justifies capital, partnership or acquisition. This article reads that change at the level of governance, operating model and execution rather than at the level of policy headlines.

Why banking sector transformation in Uzbekistan matters now and to whom

The current cycle of banking reform in Uzbekistan has moved well beyond an early-stage opening. The IMF's 2025 Article IV consultation called for enhanced bank supervision, a stronger commercial orientation and corporate governance for state-owned banks, the phasing out of directed and preferential lending, and expedited privatisation. The Central Bank of Uzbekistan now publishes detailed banking-sector indicators showing a system that has scaled rapidly in assets, credit and deposits, with 35 commercial banks active by early 2026. Scale, however, is not the same as quality, and that distinction is the work ahead.

Three audiences should read this transition closely. For banking executives, the operating environment is shifting from policy-set lending to commercial competition, which changes what good performance looks like at portfolio, branch and product level. For boards, fiduciary expectations are rising in line with the standards expected of any system undergoing financial sector modernisation in Uzbekistan. For international investors and financial institutions, the practical question is which Uzbek bank can be relied on to behave commercially after a transaction — rather than which is formally available for sale. The reform creates a market, but a selective one.

The real transformation challenge within state-owned banks

The most useful diagnostic of the underlying challenge is the first IMF–World Bank Financial Sector Assessment Program for Uzbekistan, completed in 2025. It describes a system in which state-owned commercial banks still account for around two-thirds of banking-system assets and roughly half of deposits, and where directed and preferential lending stood at about 24 per cent of total bank lending at end-2024, having fallen from 39 per cent in 2020. The direction of travel is right; the gap to genuinely commercial banking is still material.

Beneath those headline figures, the assessment identifies the issues that determine whether bank privatisation in Uzbekistan generates value. Asset classification rules do not yet fully align with international standards, so reported non-performing loan ratios are materially lower than IFRS Stage 3 equivalents. Provisioning is limited relative to the underlying credit risk. Governance structures in state-owned commercial banks have historically been shaped by lending priorities rather than risk-adjusted return. Workforce capability in credit risk, product development and customer analytics lags the demands of competitive banking.

This is where the difference between digitalisation and transformation becomes operational. If legacy credit logic is automated rather than redesigned, transformation risk goes up rather than down. Serious banking advisory in Uzbekistan therefore starts not with platforms but with decision rights, credit policy and the way risk is owned at board and management level.

What bank privatisation in Uzbekistan requires beyond a change of ownership

The World Bank's Uzbekistan Financial Sector Reform Project, approved in 2022, treats bank privatisation and restructuring in Uzbekistan as one sequenced exercise rather than a stand-alone transaction. Its largest component supports the modernisation, commercialisation and privatisation of state-owned commercial banks together, in line with the 2020–2025 Banking Reform Strategy. The framing matters: ownership change without operational change is not transformation.

For an investor evaluating an acquisition, strategic partnership or minority stake in an Uzbek bank, the relevant due-diligence agenda goes well beyond capital structure. It includes the independence and competence of the supervisory board; the effectiveness of the risk committee and its access to unfiltered portfolio data; the discipline of related-party transaction monitoring; the rigour of an asset quality review under conservative classification rules; the realism of provisioning; the structure of management incentives; the clarity of customer segmentation and product profitability; and the credibility of the post-investment transformation plan.

Boards on the seller side face a parallel agenda. Investor readiness is not a presentation, it is a state. It requires transparent reporting, a coherent risk culture, and a management team that can defend its credit and pricing decisions on commercial grounds. For sellers and acquirers alike, this is the work to which board advisory and governance support for banks and financial institutions is most directly relevant.

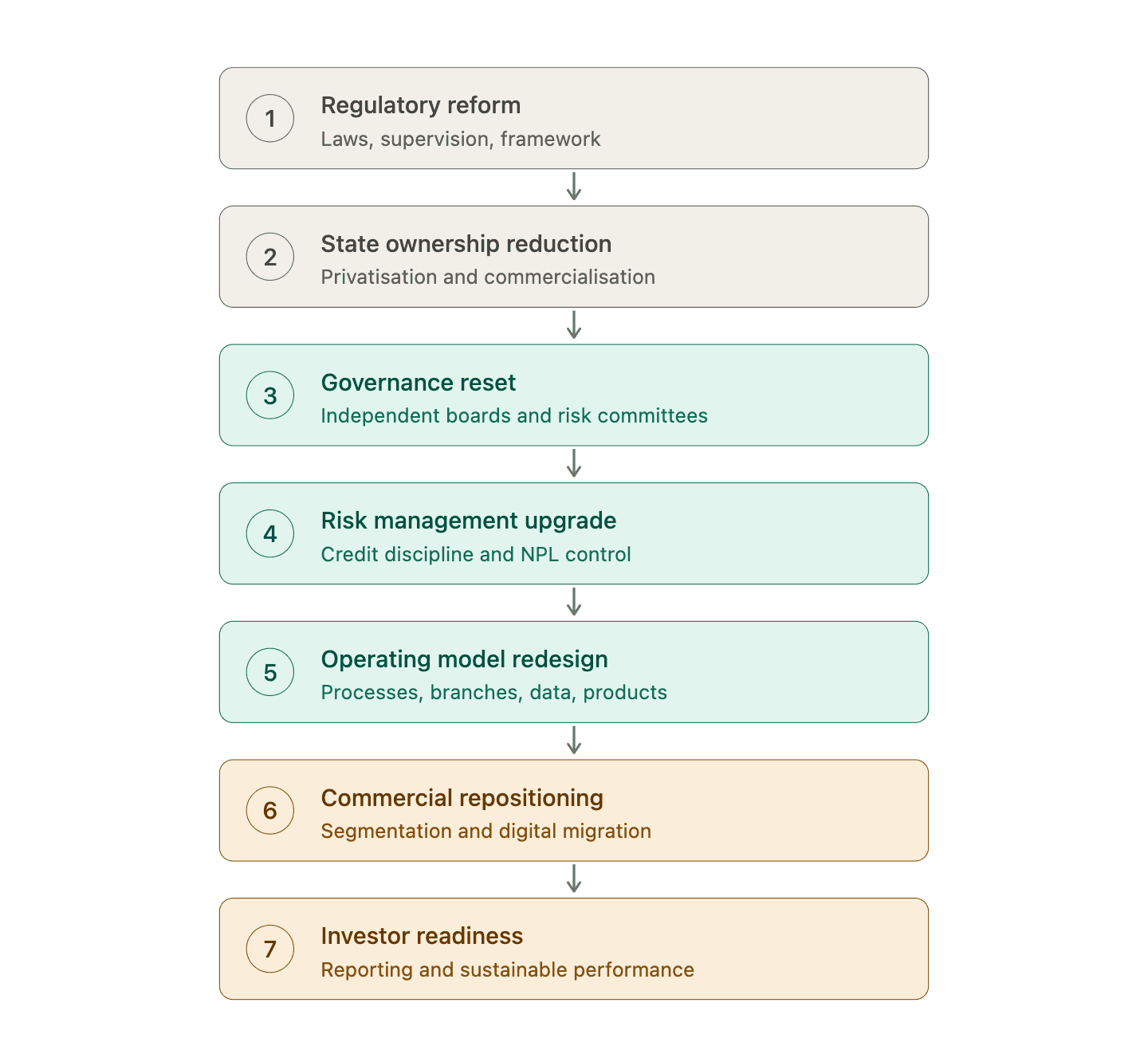

A practical framework for banking modernisation in Uzbekistan's banks

Advisory for banking modernisation in Uzbekistan is most useful when it is sequenced rather than thematic. The four areas below are not independent workstreams; they are stages of the same transformation.

Governance restructuring

Board independence is the first lever. Independent directors with banking and risk credentials, a functioning risk committee with direct access to credit management information, audit and compliance oversight that is not subordinate to commercial lines, clear decision rights between board, CEO and credit committee, and a disciplined approach to related-party transactions are the minimum for genuine governance and operating model reform in Uzbekistan's banks. Without these, every downstream initiative becomes contingent on individuals rather than institutions.

Risk management upgrade

The 2025 FSAP makes the supervisory priorities unambiguous: align asset classification with international standards, address NPL definition and forbearance rules, strengthen on-site inspections and operationalise NPL workout units. At bank level this translates into credit scoring fit for SME and consumer lending, portfolio monitoring with early-warning indicators, provisioning discipline, stress-testing built into capital planning rather than added on top, and a workout function with real authority to restructure or exit problem exposures.

Operating model redesign

Operating model work covers the architecture beneath the strategy: branch-network rationalisation aligned with actual customer behaviour, back-office process automation, customer segmentation that drives product design, product-level profitability analysis, a sequenced digital migration plan, and a data architecture that allows risk and commercial teams to work from the same view. This is the domain of business transformation and operating model redesign in complex financial institutions, and it is where most of the value of privatisation is ultimately captured or lost.

Strategic repositioning

The final layer is commercial. Each Uzbek bank in transition must decide which customer segments - SME, retail, mid-corporate, large corporate as it is genuinely built to serve, what fee income and product mix is realistic, how to deploy fintech partnerships without delegating credit judgement, and how capital is allocated between segments. This is also where partnership with international banks and international financial institutions becomes more than ceremonial.

Advisory opportunities in Uzbekistan's evolving banking sector

The EBRD's Uzbekistan Country Strategy 2024–2029 identifies the transformation and privatisation of state-owned enterprises and banks as a named priority, alongside continued credit-line work with partner banks and pre-privatisation engagement. The presence of an active multilateral with direct equity appetite confirms that banking sector transformation in Uzbekistan is producing concrete advisory situations rather than abstract reform momentum. In practice, banking sector transformation and reform in Uzbekistan creates a defined sequence of moments where senior external judgement is commercially decisive.

Several of those moments are now live. State-owned banks preparing for privatisation need governance and reporting brought to a level that investors will accept. Banks with legacy directed-lending exposure need an asset quality review and credit-process redesign before any meaningful investor conversation. Banks transitioning to a commercial model need customer segmentation, product profitability and operating-model work. Investors assessing acquisition need commercial due diligence connected to a realistic transformation roadmap, not a generic market scan. Once a transaction closes, post-investment transformation is where the value case is proved or lost. In each situation, the role of a senior advisor is to connect strategy, governance, risk and execution so that decisions made in one part of the bank do not undermine another.

This is the working terrain of financial services and banking advisory in a transition market, and it is the reason advisory support for owners, boards and senior management teams is structured around the institution as a whole rather than around a single function.

Where banking advisory in Uzbekistan becomes commercially relevant and to whom

Client type | Typical issue | Advisory response |

|---|---|---|

State-owned bank preparing for privatisation | Governance and reporting are not investor-ready | Board and governance advisory |

Bank with legacy loan portfolio | Asset quality and credit discipline concerns | Risk management and portfolio review |

Bank shifting to a commercial model | Weak customer segmentation and product profitability | Strategy and operating model redesign |

Investor assessing bank acquisition | Unclear governance, risk and transformation cost | Commercial due diligence and transformation roadmap |

Bank modernising operations | Fragmented IT, inefficient processes and costly branch network | Operating model transformation |

From state-directed banking to commercially disciplined banking in Uzbekistan's banks - phased transformation pathway, shown below.

Conclusion

How Uzbekistan is transforming its banking sector will ultimately be judged not by the count of privatised institutions but by the depth of change inside each one. Banking sector transformation in Uzbekistan succeeds where boards exercise real authority, risk discipline is built into credit and capital decisions, operating models are redesigned rather than digitised, and reporting is credible enough to support investment. For banks, investors and boards, the practical agenda is clear: treat reform as the start of an operating model transformation, not the end of an ownership question. The institutions that internalise that distinction are the ones that will create durable value.

For banks, investors or boards assessing transformation, governance or privatisation-related questions in Uzbekistan, Tretiakov Consulting provides senior-level advisory support across strategy, operating model redesign and board-level decision support. To discuss a banking transformation or governance mandate, please get in touch.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.