Pharma and Life Sciences Advisory in Switzerland

On 14 November 2025, the United States, Switzerland and Liechtenstein signed a joint memorandum of understanding capping Section 232 pharmaceutical tariffs at 15%. The framework followed the 7 August 2025 imposition of a 39% reciprocal tariff and included a Swiss commitment to encourage and facilitate at least USD 200bn of US investment over five years. The intervening period rewrote the operating logic of the sector. Pharma and life sciences advisory in Switzerland is no longer a discussion about whether the franchise is durable. The export base is: Interpharma reports CHF 105.5bn in pharma exports and 40.5% of total Swiss goods exports. The question is how rapidly the Swiss pharma operating model can be reconfigured around a materially larger US production footprint without weakening the European intellectual-property anchor that underwrites Switzerland's position as a global life sciences hub. Roche's USD 50bn US capex commitment of 22 April 2025 and Novartis's USD 23bn commitment of 10 April 2025 have already made the question concrete. The work is now execution, not rhetoric.

Why the Swiss life sciences sector is now the country's most exposed asset

The structural numbers are strong, and that is precisely why political exposure has risen. Interpharma reports pharmaceutical exports of CHF 105.5bn, equivalent to 40.5% of total Swiss goods exports, a direct contribution of 5.8% to GDP, and 50,600 direct jobs. The BAK Economics study commissioned by Interpharma puts the total direct and indirect value-added effect at CHF 74.5bn, almost one Swiss franc in ten generated along the sector's value chains. Concentration of that magnitude produces a bilateral imbalance. SECO quantified the 2024 figure at around USD 38bn, and that imbalance provided the political justification for the original 39% reciprocal tariff.

Beneath the headline strength, warning signals are visible. Interpharma data show foreign direct investment into Switzerland in decline since 2017, and biotech start-up funding falling from close to half of all Swiss start-up investment in 2017 to 31% in 2024. Switzerland slipped to third place in the BAK Economics Global Industry Competitiveness Index 2025, tied with Denmark on a score of 117, behind the United States on 128 and Ireland on 118. The EFPIA W.A.I.T. Indicator 2024, cited by Interpharma, shows Switzerland dropping from sixth to seventh place. The export franchise is intact. The framework conditions around it are not.

Tariff exposure and the operating-model rewrite

Federal Council communications of 7 August 2025 confirmed a 39% reciprocal tariff on Swiss imports into the United States, a level at which the margin structure of Swiss-manufactured US-bound biologics came under immediate pressure. The 14 November 2025 framework reduced the ceiling to 15%, against a Swiss commitment to encourage and facilitate USD 200bn of US investment, of which USD 67bn is earmarked for 2026. SECO has been explicit that the framework is a non-binding joint memorandum of understanding. On 14 January 2026, the Federal Council adopted a final negotiating mandate for a legally binding agreement still in negotiation.

The operational consequences arrived faster than the legal text. Roche's USD 50bn US capex commitment, announced on 22 April 2025, covers new and expanded manufacturing across multiple US sites. Novartis's USD 23bn commitment, announced on 10 April 2025, will build seven new US facilities and shift production of key Novartis medicines for US patients onto US soil. The practical consequence is a rebalancing of fill-finish and biologics capacity towards the US, a corresponding renegotiation of CDMO procurement contracts, and a structural gap between announced investment and operational capacity. Greenfield pharmaceutical manufacturing routinely runs to five to ten years from groundbreak to FDA-inspected commercial throughput.

For large-cap groups the pressure surfaces through direct US capex. For mid-caps, biotechs, medtech suppliers and CDMOs, the same pressure surfaces through partner selection, CDMO contracting, regulatory sequencing and investor expectations. The physical footprint may not move, but the commercial posture does. The Swiss pharma operating model is no longer defined by headquarters location alone. It is defined by the allocation of manufacturing, IP, regulatory and capital commitments across jurisdictions. That rebuild is the substantive content of operating model redesign work in 2026.

M&A in 2025: what the deal flow actually says

Three transactions define the 2025 vintage and the contours of Swiss biotech M&A advisory in the period. On 26 October 2025, Novartis announced the acquisition of Avidity Biosciences at USD 72.00 per share in cash, valuing the company at approximately USD 12bn fully diluted, a 46% premium to the 24 October close. The transaction closed on 27 February 2026, with Avidity's early-stage cardiology programmes carved out into a SpinCo retained by legacy shareholders. On 18 September 2025, Roche entered a definitive merger agreement to acquire 89bio at USD 14.50 per share in cash, an equity value of approximately USD 2.4bn, plus a non-tradeable contingent value right of up to USD 6.00 per share on milestones, for total potential consideration of approximately USD 3.5bn. The Partners Group-led consortium acquired Techem on 14 July 2025 at an enterprise value of EUR 6.7bn, closing on 7 October 2025.

Three execution realities follow. Big Pharma is paying late-stage premia driven by patent-cliff arithmetic rather than synergy modelling, as the 46% Avidity premium demonstrates. Swiss outbound M&A is compensating for tightening domestic biotech conditions. Integration risk sits where boards have least bandwidth: SpinCo carve-out mechanics, multi-jurisdiction antitrust clearance, CVR-trigger drafting on milestones extending years forward, and retention of the chief scientific officers who anchor RNA-platform leadership.

The shift this implies for Swiss biotech M&A advisory is a discipline of execution sequencing rather than target selection. The targets are visible. The harder work is modelling integration, carve-out and retention risk before the auction premium is paid. That is where the differentiated value of post-deal integration shows: SpinCo separation, CVR milestone governance, and retention of scientific leadership whose departure would invalidate the deal thesis. For most Swiss boards, this is also where operating model and M&A advisory for Swiss pharma companies needs to demonstrate execution discipline rather than transaction enthusiasm.

Supply chain positioning in the Swissmedic, EMA and FDA regulatory environment

Switzerland's regulatory architecture remains its most underappreciated structural asset. The Swissmedic and FDA Mutual Recognition Agreement on Good Manufacturing Practice was signed on 12 January 2023 and entered into force on 27 July 2023, covering human and veterinary medicines, with vaccines identified by Swissmedic as the next scope-expansion priority. Swissmedic also operates under the EU and Switzerland MRA on GMP, a 2015 confidentiality arrangement with the EMA, participation in the EMA OPEN framework, and founding membership of the Access Consortium.

The operational implication is that Swiss manufacturing sites are globally inspectable with low duplicate-inspection overhead, one of the few structural advantages to survive the 2025 tariff reset. Pharma supply chain strategy Switzerland should therefore be built around regulatory leverage, not production-cost optimisation alone, because the cost advantage has been narrowing for a decade while the regulatory advantage compounds. This is why operating model redesign in regulated industries should begin with inspection reliance, authorisation pathways and reimbursement friction before manufacturing location is treated as a cost question.

Where boards misread the architecture: MRAs reduce inspection cost but do not confer commercial market access, which requires separate authorisation and reimbursement processes. Medtech subsidiaries underestimate the cost of EU MDR and IVDR alignment. For cell and gene therapies, companies also need to distinguish regulatory authorisation from commercial availability: Swissmedic approval, pricing decisions and reimbursement pathways can create separate timing risks that are often compressed into one board-level assumption. Pharma supply chain strategy Switzerland also has to distinguish inspection reliance from market authorisation, which are often conflated in board-level discussions.

Board governance, capital allocation and the execution gap

The typical Swiss life sciences board is being asked to approve three classes of decision simultaneously, each with a different reversibility profile. The first is capital reallocation towards the US at a scale, Roche USD 50bn, Novartis USD 23bn and the broader USD 200bn aggregate, that is not practically reversible once construction begins. The second is an M&A programme whose target valuations are a function of FDA approval timelines and CVR milestone mechanics that boards do not directly control. The third is supply chain reconfiguration whose tax, transfer-pricing and IP-holding implications interlock with OECD Pillar Two and the Swiss federal corporate-tax reform agenda.

Execution fails in predictable places. Governance bandwidth is the most common failure point, because a board that meets six to eight times a year cannot exercise meaningful oversight of three concurrent transformation programmes. Key-person concentration around individual chief scientific officers turns retention risk into deal risk. Post-deal integration leadership is routinely under-resourced relative to the diligence team that closed the transaction. Management forecasts that assume tariff stability under a non-binding instrument are an analytical category error.

In this context, life sciences transformation Switzerland is not a programme label. It is a board-level sequencing problem. That is why board governance and oversight sits ahead of execution support in the proper order of advisory work. For boards, life sciences transformation Switzerland now means deciding which commitments can still be staged and which have already become structurally irreversible. That decision is made at the board table before it reaches the operating teams.

What pharma and life sciences advisory in Switzerland must now solve

Pharma and life sciences advisory in Switzerland for boards and investors must separate decisions that can be revisited from those that cannot, and match the depth of analysis to the irreversibility of each commitment. The table below maps five strategic levers against the three risk axes that have proved decisive in 2025 and 2026.

Strategic lever | Tariff and policy risk | Regulatory and integration risk | Governance and execution risk |

|---|---|---|---|

Operating model footprint (US versus Basel and Lemanic anchor) | Section 232 reactivation under a non-binding MoU; MFN reference pricing leakage | Pillar Two and transfer-pricing realignment of IP-holding structures | CFO bandwidth on capex sequencing; reversibility of US site decisions |

Therapeutic-area M&A | Tariff-driven distortion of US-asset valuations | Ex-US regulatory divergence on CGT and RNA platforms | CVR-trigger renegotiation if integration slips; CSO retention risk |

Supply chain reconfiguration | US Section 232 review cycles outside the 15% ceiling | Vaccines still outside the Swissmedic and FDA MRA scope | CDMO concentration on fill-finish and sterile injectables |

R&D capital allocation | MFN pricing leakage from low Swiss list prices into US baskets | EU Clinical Trial Regulation drift; data-package alignment cost | Key-person dependency in scientific leadership |

Governance and board capability | Audit committees not composed for tariff-scenario modelling | Compliance scope creep across Swissmedic, EMA and FDA filings | Weak separation of strategy oversight from execution oversight |

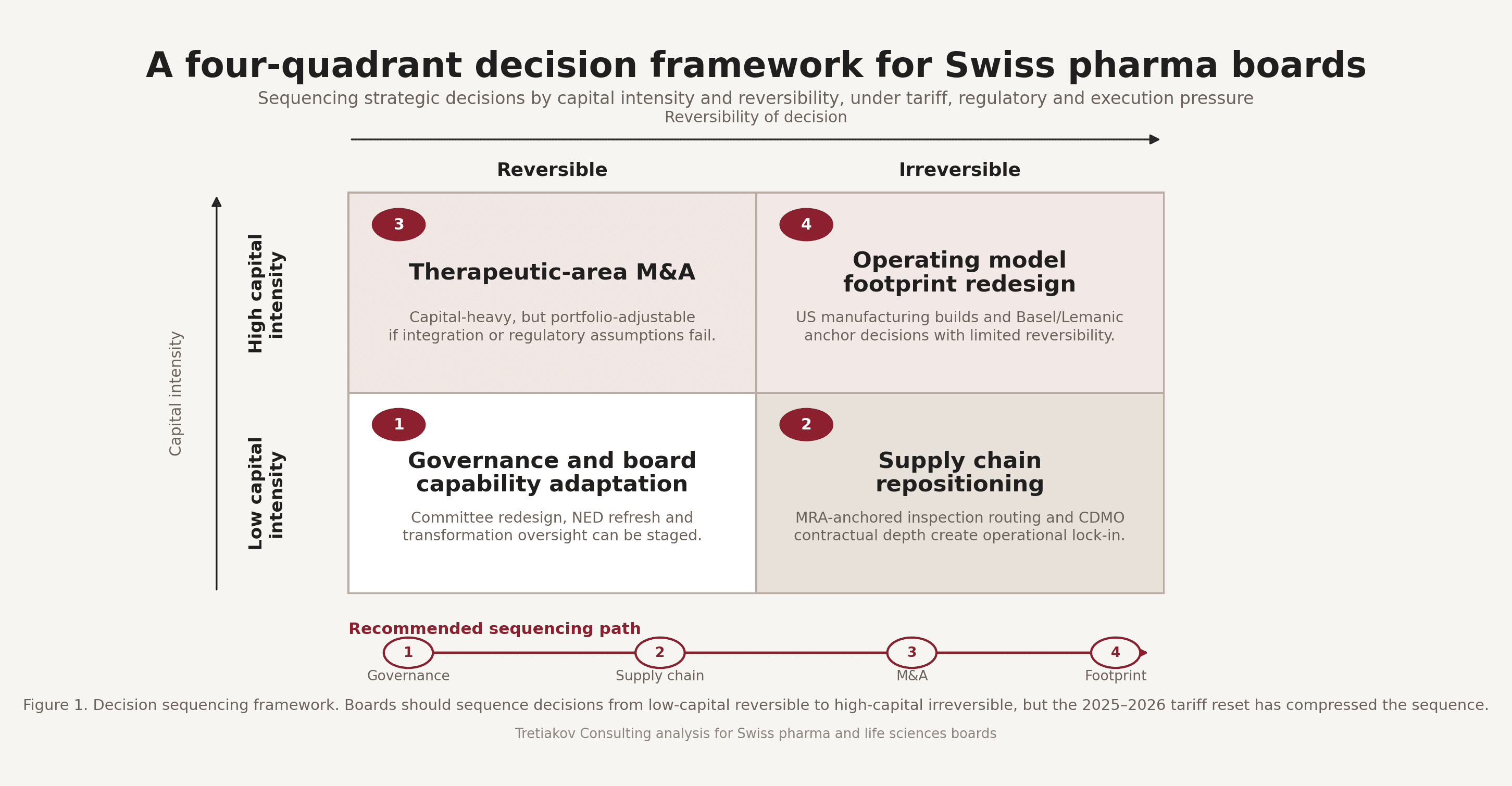

The same logic resolves into a sequencing framework that places capital intensity on one axis and reversibility on the other.

The sequencing logic is straightforward. Fix governance first, the cheapest and most reversible lever, and the one that conditions every subsequent decision. Anchor the supply chain second, because CDMO contracts and Swissmedic and FDA MRA-leveraged sites involve relatively modest absolute capital but become contractually irreversible once committed. Address therapeutic-area M&A third, high capital but portfolio-adjustable, since assets can be divested if the integration thesis fails. Resolve operating-model footprint last and most deliberately, because once a US biologics line is operational the European footprint loses its strategic optionality. One recurring failure mode in 2025 was the inversion of this order. Boards approved footprint redesign before fixing governance, and then asked the same audit committee to oversee both.

Closing perspective

The question for Swiss life sciences boards is not whether the operating model will change. It already has, in the months between 7 August 2025 and the Federal Council's 14 January 2026 negotiating mandate. The remaining question is whether the sequencing of irreversible commitments will reflect the structural logic of the franchise or the political tempo of the tariff cycle. Pharma and life sciences advisory in Switzerland, properly understood, is the discipline of helping boards sequence irreversible decisions under simultaneous regulatory and capital pressure. That is the strategic positioning for Swiss life sciences under tariff and supply chain pressure that the current environment now requires. Boards weighing footprint, M&A and supply chain decisions in parallel are invited to a confidential conversation with Tretiakov Consulting's Swiss life sciences advisory team.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.