From Swiss Reputation to Defensible Economics: Business Management and Strategy Consulting in Switzerland

A Swiss business can be admired, profitable and well run and still find that the advantages which once made it successful are quietly working against it. The franc converts a record export order into a thinner margin than the year before; a regional headquarters placed in Zug for reasons that once included tax now faces a global minimum rate it cannot opt out of; a respected family firm approaches a succession it has never formally prepared, with no agreed governance to carry it through. None of this reflects weak management or a weak economy, and that is precisely why it is so often misread. It is where business management and strategy consulting in Switzerland earns its place, because the work is no longer to defend a position the market handed the company but to rebuild the operating model, the footprint and the governance that a harder environment now demands.

The Swiss reputation for stability, quality and a benign business climate remains real. What has changed is that the favourable part has stopped being automatic. For a generation, a strong currency, a premium brand, deep talent and an attractive tax position did much of the strategic work on a company's behalf, and a board could set direction at the top while the operating model evolved gently beneath it. That settlement is no longer reliable, and it has weakened on three fronts at once. The questions that now keep Swiss owners and boards awake are concrete rather than abstract: whether a premium cost base can still be defended by productivity rather than price, whether a Swiss headquarters has any substance beyond the tax rate it was built around, and whether a family business is genuinely transferable once the founder steps back. Stability is not the same as strategic resilience, and the distinction is becoming expensive.

Why the Conditions That Made Swiss Success Almost Automatic Are Narrowing

The first thing a board has to accept is that the wider environment no longer carries the business the way it used to. The State Secretariat for Economic Affairs forecasts growth of 1.0% for 2026 and 1.7% for 2027, both described as below average against a long-run rate closer to 1.8%. Slower growth on its own is manageable, but it removes the cushion that once disguised a weak operating model, because demand no longer rises fast enough to absorb inefficiency. The structural picture reinforces the point. The OECD places Switzerland among the most productive economies in its membership, yet it also points to productivity growth that has slowed markedly over three decades and to persistent administrative and internal-market frictions that weigh on competition and resilience. For a board, the implication is direct: in a low-growth, high-cost, strong-currency economy, returns now come from the quality of the operating model rather than from a rising tide.

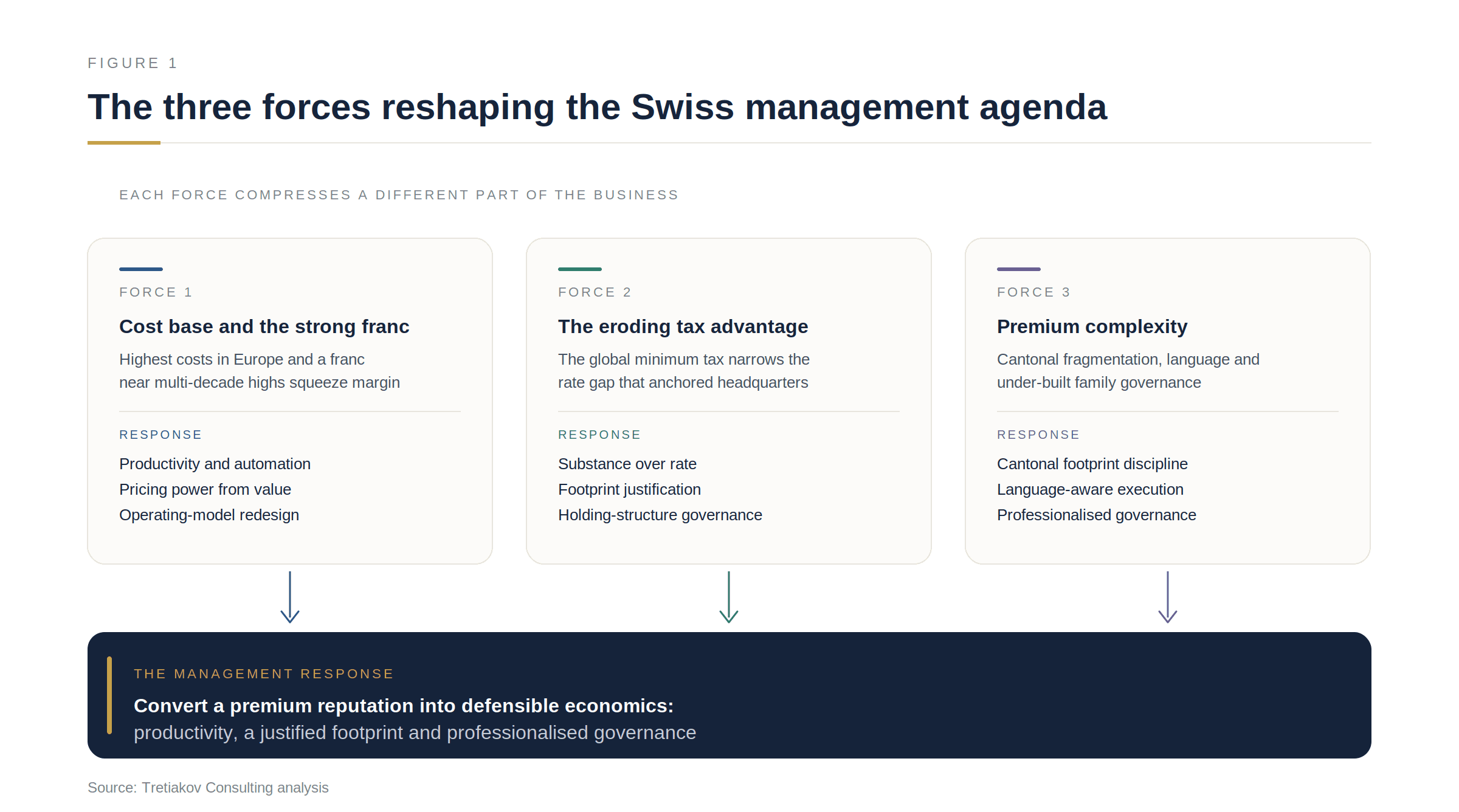

Three forces are doing most of the work behind this, and they are best understood together rather than in isolation. The cost base and the franc punish anything that is not genuine productivity or genuine premium value. The tax advantage that anchored a large part of the headquarters economy is eroding under the global minimum tax. And beneath the reputation for order, cantonal fragmentation, multilingual federalism and under-built governance in family and mid-market firms make execution considerably harder than the brand suggests. The rest of this analysis takes each force in turn and then sets out where external advice is genuinely useful.

The Strong Franc and the Cost Base: Why Price Competition Is Not an Option

The franc is the most visible of the three pressures and the one most often mishandled. The Swiss National Bank cut its policy rate to 0% with effect from June 2025, the sixth consecutive reduction since early 2024, and has held it there through its subsequent assessments, with sight deposits above a threshold remunerated at minus 0.25%. Even at a zero rate, the currency has continued to strengthen, trading near multi-decade highs against both the euro and the dollar. A strong franc is a vote of confidence in the country, but for an exporting or import-competing business it operates as a slow and continuous tax on margin. The franc does not create weak margins; it exposes operating models that were never built to defend them.

The mechanism matters more than the headline. A company that earns revenue in euros or dollars and carries its cost of goods, wages, rent and overhead in francs experiences the appreciation twice. The first effect is translational: foreign revenue converts into fewer francs, so reported earnings fall even when volumes and local prices hold. The second is transactional and more damaging, because the real cash margin on each unit narrows as the currency moves, and the domestic cost base does not move with it. Swiss costs are sticky for a reason. The country is, on the Eurostat measure, the most expensive of the 36 European countries surveyed in 2024, with consumer prices at roughly 184% of the EU average, and the Federal Statistical Office reports a median gross full-time wage of CHF 7,024 a month in 2024. Those costs are part of what makes Swiss output excellent, and they cannot simply be cut without dismantling the very quality that justifies the premium.

This is why hedging, although necessary, is not a strategy. Currency hedging changes the timing of the pain and protects a budgeting horizon, but it cannot offset a structural appreciation that runs for years, and a board that treats its treasury desk as the answer to a franc problem is buying time rather than solving anything. The durable response is operational. When price competition is not available, margin has to be defended through productivity, pricing power earned by demonstrable value, automation that takes labour cost out of the unit economics, and a deliberate move up the value chain, so that the customer is paying for something a cheaper supplier cannot replicate. In this environment a weak operating model rarely fails dramatically; it concedes a point or two of margin at a time until a premium business no longer earns a premium return. That is a question of redesigning the operating model rather than trimming it, and it is the substance of serious operating model advisory in Switzerland. The detailed mechanics of this, from product complexity to plant footprint, are set out in our optimisation work with Swiss manufacturers, where the recurring finding is that the margin is usually recoverable, but only structurally.

The Headquarters Economy After the Global Minimum Tax

The second force reaches a different constituency: the holding companies, regional headquarters and multinational functions that chose Switzerland partly for its tax position. That position is changing in a way that is now enacted rather than speculative. Swiss voters approved the constitutional basis for the OECD and G20 minimum tax in June 2023 with 78.5% in favour and the support of all 26 cantons, and the Federal Department of Finance brought the Qualified Domestic Minimum Top-up Tax into force from the start of 2024 and the Income Inclusion Rule from the start of 2025, while leaving the Undertaxed Profits Rule deferred. The first information returns under the global rules fall due in mid-2026. A board should be precise about what this does and does not mean. It does not abolish the Swiss tax advantage, and the language of "the end of low-tax Switzerland" is wrong. What it does is narrow the rate gap, because a group entity in a low-tax canton that previously paid an effective rate well below 15% now faces a top-up toward that floor, and the arbitrage that once anchored the structure shrinks accordingly.

The revenue question illustrates why caution is needed when this is discussed. The Federal Council initially estimated additional receipts of CHF 1 to 2.5 billion, later raised toward CHF 1.5 to 3.5 billion once the Income Inclusion Rule applied, and these remain estimates rather than outcomes. Independent analysis of the largest listed groups has found the amounts actually paid in the first year to be materially smaller and heavily concentrated in a handful of companies, which is a useful reminder that a rate change and a behaviour change are not the same thing. The more consequential signal sits in the capital data. The Swiss National Bank recorded net disinvestment of foreign direct investment of CHF 83 billion in 2024, with the withdrawals once again concentrated in the finance and holding company category, a pattern that has run since 2018. This is not a wholesale exit, and the inward FDI stock remained around CHF 926 billion. Disinvestment concentrated in holding and finance entities can reflect intra-group balance-sheet restructuring, treasury flows and entity rationalisation rather than operational relocation, but it is consistent with a wider trend in which holding structures are being reviewed and the question of why a function should sit in Switzerland is being asked in earnest.

The governance consequence is the part that boards underestimate. A structure designed around a tax logic now needs an operating-model and substance logic. Once the rate advantage narrows, the justification for a Swiss footprint has to rest on something both the tax authorities and the group's own capital allocators will accept, namely genuine decision-making, real talent, proximity to an ecosystem and the governance quality that makes the location defensible. The global minimum tax does not remove Switzerland's relevance; it removes the lazy explanation for being there, and a footprint that cannot explain its substance will increasingly read as cost without strategic logic. The question for a headquarters is shifting from where the rate is lowest to where the management substance is real enough to justify the structure. This is where advisory for headquarters and holding companies in Switzerland becomes concrete rather than theoretical, and it frequently runs straight into transaction questions, because footprint rationalisation, entity simplification and the relocation or consolidation of functions are corporate transactions in all but name. The governance discipline involved is the same one we examine in our work on cross-border M&A and footprint governance. For a foreign investor, the calculation is the same in reverse, and business consulting for foreign investors in Switzerland now has to lead with substance and operating logic rather than with a headline rate that is converging on everyone else's.

Premium Complexity: Cantonal Fragmentation, Language and Under-Built Governance

The third force is the one the Swiss brand most effectively conceals. Stability at the national level coexists with genuine complexity at the operating level, and a company that mistakes the calm surface for simple execution tends to discover the difference at the worst possible moment. The country runs through 26 cantons and more than 2,100 municipalities, each with its own administrative texture, and tax is only the most measurable expression of that fragmentation. The KPMG Swiss Tax Report for 2025 puts the average ordinary corporate tax rate at 14.4%, ranging from 11.85% in Zug to 20.54% in Bern, and notes that several low-tax cantons have raised rates in connection with the minimum tax. A spread of that size across a country smaller than many single regions elsewhere means that footprint decisions, incentive negotiations and even hiring economics differ materially from one canton to the next.

Language compounds this. Switzerland operates in German, French and Italian, with German spoken by around 62% of the population, French by about 23% and Italian by roughly 8%, and the cultural and commercial divide known as the Röstigraben is a real factor in how a business sells, recruits and runs change across the country rather than a piece of folklore. A go-to-market model or a transformation programme that works cleanly in Zurich does not transplant unchanged to Geneva or Lugano, and a management team that assumes it will is underestimating its own execution risk.

The deepest complexity, though, is structural and demographic. The Federal Statistical Office and SECO record that small and medium-sized enterprises make up more than 99% of Swiss firms and provide about two-thirds of all jobs, and a large share of these are family-owned. Many of them combine genuinely sophisticated operations with governance that has never been built out beyond the founder, which is sustainable until it is suddenly not.

Research by the University of St. Gallen and UBS expects more than 100,000 Swiss family businesses to undergo a generational transition by 2030, and separate work has found that a large proportion of owners have taken no concrete preparatory steps. The issue is not only the number of transitions but the readiness gap behind them, because a family firm can look entirely stable from the outside while being economically non-transferable inside. Succession in a Swiss family firm is therefore not a family event but an enterprise-risk event. The financial signature of this is specific and avoidable: where decision-making, client relationships and institutional knowledge sit with one or two people, the business carries a key-person dependency that depresses its valuation at transmission, raises the risk of a distress sale, and threatens continuity precisely when a buyer or a bank is looking most closely. This is why strategic advisory for family-owned companies in Switzerland is rarely about importing a listed-company template and far more often about professionalising board and family governance just enough to make the business transferable and resilient. The same logic underlies strategy consulting for mid-market companies in Switzerland, where the value of an external view lies less in analytical capacity, which most capable boards already possess, than in the independence and seniority needed to raise questions an internal hierarchy will not.

Where Business Management and Strategy Consulting in Switzerland Must Connect

These three forces share a feature that determines how they should be addressed: none of them is contained within a single management discipline, and each cuts across strategy, operations and governance at the same time. The common thread is easy to miss. Many Swiss operating models were built for a period in which the location advantage absorbed a degree of managerial imprecision, and that period is ending, so the premium now has to be earned operationally rather than inherited reputationally. That is why business management and strategy consulting in Switzerland is most valuable where the three layers are designed to work as one system rather than bought separately and stitched together afterwards.

In the Swiss context, strategy consulting is useful only when it resolves the economics of the premium itself: where the company can still win when price is not a lever, which activities genuinely justify a Swiss cost base, and which functions should remain in Switzerland once tax is no longer the deciding argument. This is the proper domain of strategic advisory in Switzerland, concerned with capital allocation and the deliberate closing of options rather than with the production of plans, and it connects directly to the work of commercial growth and strategic direction.

Management consulting becomes decisive when that direction has to be turned into unit economics, decision rights, automation, footprint and a governance cadence the board can actually see. It redesigns the operating model so that productivity and value capture defend the margin the strategy assumes, and it sequences change so that it can be absorbed across cantons and languages without overwhelming the organisation. The value of management consulting in Switzerland lies in its insistence that a strategy is only as good as the system built to deliver it.

Business advisory services in Switzerland connect both layers to the commercial, transactional and governance reality that surrounds them, from footprint and substance decisions under the minimum tax to succession structuring and the conduct of an eventual transaction. It is at this level that the difference between an attractive idea and an executable one is established. The Swiss advisory market is mature and concentrated, dominated by a small number of large firms alongside a long tail of specialists, but what matters for a board is not the size of the market but the fit of the firm, and that is examined below.

Figure 1. The three forces reshaping the Swiss management agenda

The three forces converge on a single management response: productivity, a justified footprint and professionalised governance. A company that delivers all three converts its premium reputation into something defensible, while a company that delivers none of them is relying on advantages that are quietly disappearing.

A Swiss Operating-Model and Footprint Framework for Boards and Owners

The framework below is the practical expression of how business management and strategy consulting in Switzerland should operate in current conditions. It is organised around the questions a board should be able to answer, the reason each carries weight in the Swiss context, and the kind of output required to address it. It is framed around decisions rather than functions, because the pressures described above are failures of decision-making before they are failures of execution.

The question the board must answer | Why it matters in Switzerland | The output required to close the gap |

|---|---|---|

Can we defend margin without competing on price? | The highest cost base in Europe and a franc near multi-decade highs compress margin through translation and transaction effects | A pricing-power review, a productivity and automation roadmap and an operating-model redesign |

Why should this function or headquarters sit in Switzerland? | The global minimum tax narrows the rate advantage that anchored many holding and headquarters decisions | A substance and footprint review with a function-by-function location logic and a governed holding structure |

Are we optimising across the cantons, not only within one? | Corporate tax ranges from about 11.85% to 20.54% across cantons, alongside differing administrative regimes | A cantonal footprint and incentive review and a rationalisation of sites and entities |

Is our governance built for the business we have become? | Family and mid-market firms are more than 99% of companies and often run on informal governance and key-person dependency | Board effectiveness work, governance professionalisation and key-person risk mitigation |

Are we ready for succession or transmission? | More than 100,000 family businesses are expected to transition by 2030, and many are unprepared | A succession framework, a separation of ownership and management, and valuation readiness |

Is the portfolio and transaction logic still right? | A strong franc, the minimum tax and footprint pressure change the buy, build and sell calculus | A portfolio review, M&A and integration support, and divestment readiness |

How to Choose the Right Consulting Firm in Switzerland

The question of how to choose a consulting firm in Switzerland is best answered by matching the firm to the mandate rather than to the strength of its brand, because each category of adviser is suited to a particular kind of problem and poorly suited to others. The most expensive mistakes are made when a board engages the wrong category for the problem it actually has.

The global strategy houses are well suited to a board that needs a defensible direction, scale benchmarking and the analytical authority of a recognised name, although their distance from execution and their reliance on leveraged delivery mean that senior attention can become less present once the engagement moves from the proposal to the work itself. The large multidisciplinary firms bring scale and reach across audit, tax and technology, which makes them effective on broad transformation and on the tax-adjacent questions the minimum tax now raises, although delivery can become process-heavy where the mandate calls for judgement under uncertainty, and a firm that also audits or advises on tax may face boundaries on what it can take on. Swiss boutiques offer genuine depth in a single sector or function and a close knowledge of cantonal and linguistic reality, which is valuable when the problem is well bounded, though their reach can be limited when a mandate spans strategy, operations and governance at once. Senior-led business consulting in Switzerland can be effective where the binding constraint is not analytical capacity but judgement, discretion and continuity between diagnosis and execution, and the defining characteristic of a consulting firm for complex business mandates in Switzerland is that the people who frame the problem remain accountable for resolving it. It is not the right model for every mandate, and in particular not for those that require large-scale programme staffing across dozens of parallel workstreams, where scale rather than seniority is the real requirement.

Firm type | Typical strengths | Typical limitations | Best-fit Swiss mandate |

|---|---|---|---|

Global strategy house | Brand, analytical depth and access at board level | Distance from execution and leveraged delivery, so senior time can thin after the pitch | Direction, portfolio and benchmarking at group level |

Big Four or large multidisciplinary firm | Scale and reach across audit, tax and technology | Delivery can become process-heavy; independence boundaries where the firm also audits | Broad transformation and tax-adjacent footprint questions |

Swiss boutique | Sector depth and close cantonal and linguistic knowledge | Limited reach when a mandate spans strategy, operations and governance | A bounded, well-defined functional or sector problem |

Senior-led independent | Continuity of senior judgement from diagnosis to delivery, with owner and board alignment | A smaller bench, which requires the mandate to be scoped to where seniority is the constraint | An integrated, execution-sensitive mandate where seniority, not headcount, decides the outcome |

The most useful question an owner or board can put to any of the business consulting firms in Switzerland is a simple one: who, by name, will work on the engagement once the proposal has been signed?

When Companies Should Seek External Strategic and Management Advisory

The right moment to seek external strategic and management advisory is rarely a crisis, and the companies that engage well are usually those that recognise a pattern before it becomes an emergency. For an owner or board weighing the question of when should you hire a strategy consultant, the more useful test is to identify the point at which the cost of deciding without independent challenge exceeds the cost of the advice itself. This is the point at which business advisory services in Switzerland move from a discretionary cost to a form of risk management.

In the Swiss context those triggers are specific. They include a sustained compression of margin from franc strength that cost-cutting can no longer offset, a holding or headquarters structure that needs to be re-justified on substance once the minimum tax narrows the rate advantage, an approaching succession or transmission in a family-owned business, an acquisition or disposal where the strategic case is sound but the integration cost is underestimated, and a footprint that has accumulated entities and sites faster than it has rationalised them. Each of these carries a cost of waiting that is operational rather than abstract, whether in margin conceded, value lost at transmission or capital tied up in a structure that no longer earns its place. Where any of these patterns is present, the practical next step is a focused review of where strategy, footprint and governance currently disconnect, and that is the basis on which we structure our advisory engagement model. This is the working remit of business management and strategy consulting in Switzerland, which addresses not a single decision but the system within which a sequence of consequential decisions is made.

Conclusion

The Swiss brand will remain valuable, and nothing in the current environment changes the underlying quality of the country's companies, talent or institutions. What has changed is that the favourable conditions no longer do the strategic work on their own. The franc and the cost base reward only genuine productivity and genuine premium value, the global minimum tax requires a Swiss footprint to be justified by substance rather than rate, and the complexity behind the stable facade makes governance and execution harder than the reputation implies. The advantage in this environment goes to the companies that have converted reputation into a defensible operating model, a justified footprint and professionalised governance, and that is the work of business management and strategy consulting in Switzerland, which is not the production of another plan but the construction of the management system that allows a sound plan to be carried through the cost, tax and execution conditions that now define the Swiss market. For owners and boards weighing the role of a Swiss business within a wider European or global structure, the practical starting point is an honest assessment of where those three responses currently fall short, and it is the basis of how we work across Switzerland.

Frequently Asked Questions

What is the difference between management consulting and strategy consulting?

Strategy consulting is the discipline a board turns to when it has to decide what the business should become, where its capital should be placed and which options it should deliberately close, which in the Swiss context includes the role a site or headquarters should play once tax is no longer the deciding factor. Management consulting in Switzerland becomes valuable when that direction has to be turned into an operating model, a governance rhythm and the execution discipline that delivers it. The two are often bought separately, but the pressures facing Swiss companies cut across both, which is why engaging one without the other tends to leave a sound strategy without a system to carry it.

When should a company engage strategic advisory in Switzerland?

A company should engage strategic advisory in Switzerland when it faces a decision under uncertainty with capital attached and the cost of getting it wrong exceeds the cost of independent challenge. The clearest Swiss triggers are a margin under sustained pressure from the franc that cost reduction can no longer fix, a holding or headquarters structure that has to be re-justified under the global minimum tax, an approaching succession, and an acquisition or disposal. The trigger is the weight of the decision rather than a general wish for more analysis.

What does a business consultant do for a company in Switzerland?

The work usually begins by separating the visible problem from the operating constraint beneath it. A margin that is falling may be a currency effect, but it may equally be a question of product complexity, pricing discipline, plant footprint or a cost base that has never been restructured, and each requires a different intervention. A senior business consultant identifies which mechanism is actually driving the result, including where the answer lies in footprint and substance rather than in commercial activity, before recommending any change, because acting on the wrong diagnosis is more expensive than the original problem.

How should an owner choose a consulting firm in Switzerland?

The decision should follow the mandate rather than the brand. A group-level question about direction may suit a global firm, a tax-adjacent footprint question may suit a large multidisciplinary firm, a bounded sector problem may suit a Swiss boutique, and an integrated, execution-sensitive mandate usually requires senior-led advisory in which the people who diagnose the problem remain to resolve it. Among business consulting firms in Switzerland the most reliable test is to establish, before any engagement is signed, exactly who will be accountable for the work once delivery begins.

How does the global minimum tax affect Swiss headquarters and holding structures?

The minimum tax narrows rather than removes the Swiss advantage, and that is the point most boards miss. Once a top-up brings a low-tax canton toward the 15% floor, the rate gap that originally justified placing a holding company or a regional headquarters in Switzerland shrinks, and the structure has to be re-justified on substance, namely real decision-making, talent, proximity to the relevant ecosystem and demonstrable governance. The practical consequence is that footprint and entity decisions which were once treated as tax questions are now operating-model and transaction questions, and they should be governed as such.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.