Operational Turnaround in Kazakhstan for Acquired Assets

When an investor closes an acquisition in Kazakhstan, the expectation is that integration will follow a planned sequence and the acquired business will begin performing in line with the investment case. In practice, operational turnaround in Kazakhstan becomes the real agenda within weeks of completion. The gap between what was modelled during due diligence and what actually exists at the operational level can be substantial. According to Bain & Company research on M&A integration, integration problems are at the root of deal failure in 83% of cases, and many acquirers do not begin serious integration work until after the deal is signed. In Kazakhstan, where acquired assets frequently carry years of deferred maintenance, informal management structures and overstated financial performance, this delay can be particularly damaging. The question facing the new owner is not whether problems will surface but how quickly they can be identified, contained and reversed before value erosion becomes structural.

Kazakhstan remains the largest economy in Central Asia with GDP exceeding $260 billion and a stated ambition to reach $450 billion by 2029. The EBRD's country strategy for Kazakhstan emphasises fostering private sector competitiveness, improving connectivity and strengthening economic governance as central priorities. For international investors, strategic buyers and holding companies evaluating or completing acquisitions, this macro context creates both opportunity and a specific execution risk: the institutional environment is improving, but the operational reality at the level of an individual acquired asset may lag far behind national reform ambitions.

Why operational turnaround in Kazakhstan often starts after acquisition

The typical pattern is recognisable. An investor acquires a manufacturing facility, a logistics platform, a building materials producer or an energy services business. The due diligence identified some risks, provisions were made and the deal closed at what appeared to be a reasonable valuation. Within the first 60 to 90 days the acquirer discovers that the asset is materially weaker than the investment case suggested.

There are several recurring reasons. First, many businesses sold in Kazakhstan have been underinvested for years before the transaction. Capital expenditure was deferred, preventive maintenance was skipped and equipment condition deteriorated while reported production numbers were maintained through informal workarounds. Second, management quality often erodes during the sale process itself. Key people become uncertain about their future, decision-making slows and the outgoing owner may withdraw operational attention months before formal completion. Third, financial performance may have been supported by arrangements that do not survive the ownership change: below-market procurement through the seller's personal network, revenue recognition timing that flatters short-term results or cost structures that omit necessary reinvestment.

The World Bank's assessment of Kazakhstan's development trajectory highlights the importance of private sector led recovery, institutional strengthening and sustainable growth. These are real structural trends. But they operate at a macro level and do not insulate a specific acquired asset from the operational problems that were embedded before the transaction. The investor who assumes that a generally improving business environment will naturally lift the performance of a poorly managed acquired asset is making a dangerous assumption.

A further dimension is that the transition phase itself creates disruption. Customers become uncertain about continuity. Suppliers renegotiate terms. The workforce watches for signals about restructuring and job security. Local authorities in the region where the asset operates pay attention to any changes that might affect employment or tax contributions. In combination, these dynamics mean that even an asset that was genuinely stable before the sale can deteriorate quickly if the post-acquisition period is not managed with both speed and discipline.

Where investors misread the condition of an acquired asset

The most frequent mistake is treating reported EBITDA as a reliable indicator of operational health. In post-acquisition turnaround situations in Kazakhstan, the underlying operating baseline is often materially different from the financial picture presented during the transaction. Revenue may include contracts that are not sustainable under new ownership. Cost structures may exclude deferred maintenance, environmental remediation obligations or informal workforce arrangements that will need to be formalised. Working capital may be under pressure in ways that statutory accounting does not make visible.

Production capacity utilisation is routinely overstated. An asset may have a nameplate capacity of 200,000 tonnes per year but actual sustained throughput might be 55 to 65% of that figure once equipment downtime, quality rejects, raw material inconsistency and seasonal demand patterns are accounted for. Maintenance backlog is often the most underestimated liability. When preventive maintenance has been deferred for three to five years, the cost of catching up is not incremental. It can represent 15 to 25% of the asset's book value and may require production shutdowns that further reduce near-term revenue.

According to PwC's Worldwide Tax Summaries for Kazakhstan, the standard corporate income tax rate is 20% and the regulatory framework includes specific requirements around transfer pricing, social contributions, customs duties and sector licensing. For an acquirer restructuring the operations of a newly acquired business, tax exposure, historical compliance gaps and the interaction between operational changes and fiscal obligations must be mapped early. Environmental compliance is similarly important: Kazakhstan's updated environmental legislation introduces stricter requirements for emissions, waste management and industrial site obligations, and an acquired asset may carry undisclosed or underestimated exposure in these areas.

What experienced operators recognise is that the first 90 days after completion are decisive. During this window the investor either establishes genuine visibility and control or falls into a reactive pattern where problems compound faster than they can be addressed. The former director of the acquired business may remain the informal authority figure even after formal handover. Employees, suppliers and local officials may continue to treat the previous management as the real decision-makers unless the new governance model is made visible, credible and enforceable. This is not a theoretical risk. It is a pattern that repeats across M&A transactions and post-deal integration situations in Kazakhstan with striking regularity.

What the first operational diagnosis should cover

Business recovery in Kazakhstan begins with establishing the real operating baseline, not the version that was presented during the transaction. The diagnosis must be structured, rapid and designed to deliver actionable findings within three to six weeks of completion.

Cash position is the starting point. This means daily cash visibility, not monthly summaries. It includes mapping restricted cash, identifying supplier arrears, understanding the ageing profile of receivables and quantifying the gap between reported working capital and the amount actually available for operations. In many acquired businesses in Kazakhstan, payment discipline from key customers may have been deteriorating before the sale without being flagged, and the acquirer inherits a receivables book that is softer than it appears.

Customer analysis must go beyond revenue figures. The top ten customers should be assessed individually: open orders, contract terms, churn risk, relationship dependency on the previous owner and willingness to continue under new management. Losing one or two major customers during transition can shift the economics of the entire turnaround.

Production and asset condition require a physical assessment. Actual throughput versus nameplate capacity should be measured over a representative period, not taken from management presentations. Equipment condition, overdue preventive maintenance, availability of critical spare parts and the reliability of utility supply all feed into a realistic view of what the asset can actually produce today, not in a plan but in reality.

Workforce capability is assessed through observation and operational evidence rather than organisational charts. Key supervisors must be identified together with absenteeism patterns, resistance points, critical skill gaps and the informal power structures that determine how work actually gets done on the factory floor. The OECD's public governance review of Kazakhstan highlights broader institutional reforms including strengthened accountability frameworks and improved government efficiency. At the enterprise level, the parallel challenge is establishing management accountability and operational discipline within the acquired organisation itself.

Operational improvement in Kazakhstan must account for compliance exposure across labour law, environmental regulation, tax and licensing. These are not theoretical considerations. Labour law constraints limit the speed and method of workforce restructuring. Environmental obligations may require capital expenditure that was not in the original investment case. Tax arrears or historical misreporting by the previous owner can create liabilities that surface only after closing. Decision rights and escalation routes must be clarified simultaneously: without knowing who has authority to commit expenditure, approve supplier payments, authorise production changes or escalate safety issues, the diagnosis remains an academic exercise.

The diagnostic framework should produce a dashboard covering cash, customers, production, maintenance, workforce, reporting quality and compliance that allows the investor to establish a genuine baseline from which the turnaround can be planned and measured.

Turnaround leadership and governance in Kazakhstan

Performance turnaround in Central Asia is ultimately determined by the quality of leadership deployed to the asset and the speed with which governance is established. Advisory reports can identify problems. Strategy presentations can outline priorities. But in an acquired business where the management team is uncertain, the workforce is resistant and the investor is geographically distant, what determines the outcome is whether credible operational leadership is present on the ground making decisions every day.

This is where many turnarounds fail. The investor appoints a financial controller or sends periodic monitoring visits but does not place someone with genuine operational authority and turnaround experience into the asset. The result is that the local team continues operating as before, reporting improves cosmetically but not substantively and the window for effective intervention narrows. Turnaround leadership in Kazakhstan requires the ability to work across cultural boundaries without alienating the local organisation. The workforce in many acquired businesses has operated under a particular management culture for years. Resistance to change is often rational: people do not trust the new owner's intentions, they are uncertain about job security and they have seen previous reform initiatives come and go without lasting effect. Building credibility requires consistent behaviour, visible presence, demonstrated competence and the willingness to address problems directly rather than through layers of consultants and translators.

Engagement with local authorities and communities is a practical requirement, not a diplomatic nicety. In regions outside Almaty and Astana, the acquired business may be a significant employer and taxpayer. Regional government officials pay close attention to restructuring decisions that affect employment, production continuity or community services. Managing these relationships while executing operational changes requires experience in stakeholder communication and an understanding of how local decision-making works in practice.

Governance must be rebuilt practically through the introduction of reporting routines, KPI discipline, weekly operational reviews, cost-to-complete logic for improvement initiatives, defined escalation protocols and real-time visibility for the investor into the metrics that matter: cash, production output, quality, customer retention and workforce stability. Sustainable performance management cannot depend on a single individual. It must be embedded in a business transformation and operating model redesign that creates repeatable processes and governance rhythms capable of functioning after the turnaround leader has completed their mandate.

For investors who need direct interim management and operational leadership in pressured business situations, the critical variable is how quickly a capable person can be placed into the asset with clear authority and a defined mandate. Tretiakov Consulting works with acquired assets where the investor requires hands-on operational involvement during post-acquisition recovery to move from stabilisation through diagnosis to sustainable performance.

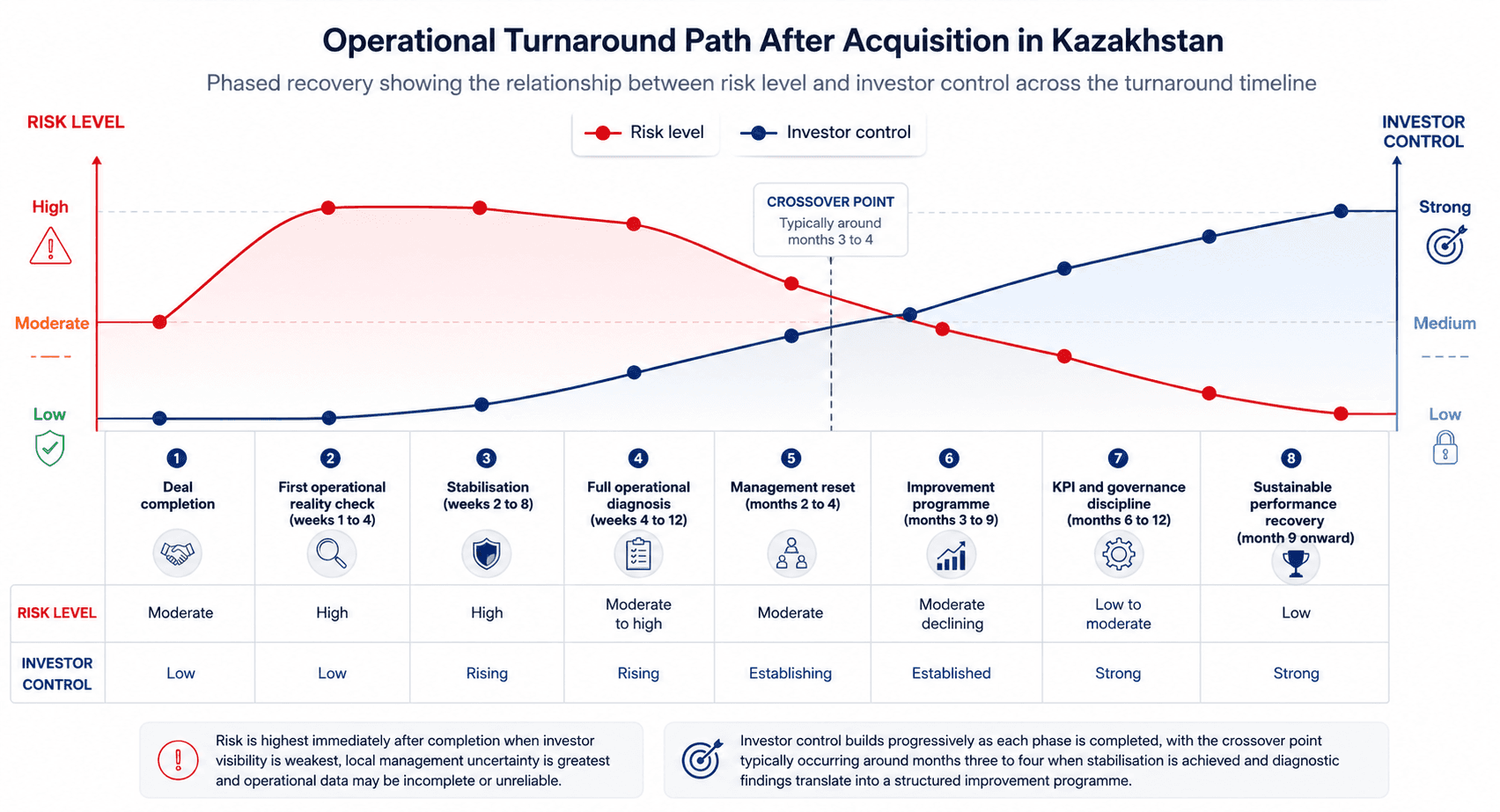

Practical turnaround framework for acquired assets in Kazakhstan

The following framework reflects the sequence that applies to most operational turnaround for acquired assets in Kazakhstan. Each phase builds on the previous one and the table is designed as an operational reference for investors and management teams navigating the post-acquisition period.

Turnaround phase | What must be done | Why it matters in Kazakhstan |

|---|---|---|

Stabilisation | Secure daily cash visibility, protect key customers, stop operational leakage, identify urgent safety and compliance risks | The investor needs immediate control and reliable information before launching broader initiatives |

Operational diagnosis | Assess actual capacity utilisation, maintenance backlog, workforce capability, reporting accuracy and regulatory exposure | Reported performance frequently does not reflect the real condition of the acquired asset |

Management reset | Clarify decision rights, replace or support weak managers, establish escalation routines and introduce reporting discipline | Local teams need clear authority and credible leadership to function during transition |

Improvement programme | Address production bottlenecks, rationalise cost structure, strengthen procurement, implement quality systems and close productivity gaps | Operational improvement in Kazakhstan must be anchored in practical constraints rather than theoretical targets |

Workforce alignment | Communicate priorities transparently, manage resistance, identify and retain critical staff, build individual accountability | Turnaround fails when the workforce perceives change as external pressure disconnected from operational reality |

Sustainable performance management | Implement KPIs, management cadence, governance routines, owner-side oversight and structured review cycles | Recovery must become repeatable and embedded in process rather than dependent on emergency intervention |

Conclusion

Investors dealing with operational turnaround in Kazakhstan should act before performance problems become structural. The first priority is to establish a reliable operational baseline, restore cash visibility, protect the customer base, stabilise the local organisation and create a governance rhythm that enables the acquired asset to move from reactive crisis management to sustained recovery. Post-acquisition turnaround in Kazakhstan requires a combination of diagnostic speed, cultural intelligence, investor-side oversight and credible leadership deployed directly to the asset. How to turn around underperforming businesses in Kazakhstan is not a question answered by strategy documents produced at a distance. It is answered by the quality of operational leadership present on the ground, the rigour of the diagnostic process and the discipline of the governance framework that follows. Hands-on turnaround support in Kazakhstan must be treated as an investment in protecting the value of the acquisition, not as an overhead to be deferred until the situation deteriorates further.

If an acquired asset requires stabilisation, performance recovery or credible operational leadership on the ground, explore our approach to interim management and operational leadership or begin a focused discussion about stabilising an acquired asset before the window for effective intervention narrows.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.