Governance and Compliance for Foreign-Owned Businesses in Kazakhstan

Owning an entity in Kazakhstan is not the same as controlling it. As of January 2025, the stock of foreign direct investment in Kazakhstan totalled $166 billion, spread across energy, manufacturing, logistics, financial services and infrastructure. The volume of international capital operating through local subsidiaries, joint ventures and acquired businesses continues to grow. Yet for many foreign investors the critical gap is not in the legal structure of ownership but in the practical governance of what they own. Governance and compliance for foreign-owned businesses in Kazakhstan is the challenge that determines whether a subsidiary functions as a transparent, controllable part of an international group or operates as a semi-autonomous local entity where decisions, risks and informal practices remain largely invisible from headquarters. The foreign parent may hold 100% of the shares, appoint the director and approve the charter, while the actual flow of material decisions, compliance exposure and risk escalation inside the entity runs through channels that headquarters neither designed nor monitors.

Why governance and compliance for foreign-owned businesses in Kazakhstan cannot remain formal

The standard approach for many international companies follows a predictable sequence: register the entity, appoint local management, adopt the parent group's compliance policies in translated form, file statutory reports and assume that the subsidiary will operate within the framework set by headquarters. In practice, the distance between this assumption and local operating reality can be significant and can remain undetected for years.

Corporate governance in Kazakhstan has advanced considerably in recent years. Kazakh Invest describes corporate governance as "a key tool for improving performance, ensuring transparency and accountability, strengthening its reputation and reducing costs." The Law on Joint Stock Companies and the Entrepreneurial Code define structural requirements for various entity types, board composition rules and shareholder protections. Kazakhstan's privatisation programme aims to reduce state participation in the economy to 15%. As of March 2025, the government has sold 989 out of 1,776 organisations subject to privatisation, and a newly established National Privatisation Office has identified 461 additional public entities for inclusion in the comprehensive programme. These reforms are real. But governance standards at the national or institutional level do not automatically translate into governance discipline inside a specific foreign-owned subsidiary. The local director may operate with broad autonomy that was never formally delegated. Material procurement decisions, hiring commitments, tax positions and customer terms may be taken without escalation to the board or the parent company.

The OECD's 2025 Integrity Review of Kazakhstan provides concrete recommendations to "improve the effectiveness of internal control, risk management and external oversight" and to "enhance transparency and integrity in decision making." While this analysis focuses on public sector institutions, the structural weaknesses it identifies apply with equal force to private foreign-owned entities where internal control is underdeveloped, risk management is informal and oversight from the parent company is limited to periodic financial reporting. The OECD further notes that "core anti-corruption institutions remain vulnerable to undue interference" and that some integrity bodies are still too recent to be fully operational. For a foreign investor, the governance question is not whether the entity is legally registered but whether anyone at headquarters or board level can reliably answer three questions: what decisions are being made locally, what risks are accumulating and whether the entity would withstand regulatory or reputational scrutiny.

In the context of M&A transactions and post-deal integration, this governance gap becomes particularly acute. Newly acquired entities often carry legacy decision patterns, informal supplier relationships and compliance gaps that the new owner inherits but does not fully understand until months after completion.

Where foreign investors misread local governance risk

The most common governance failure is the assumption that financial reporting equals governance visibility. A foreign parent may receive monthly P&L statements, balance sheets and budget variance reports from its Kazakh subsidiary. These reports may be accurate in accounting terms but reveal nothing about the quality of local decision-making, the state of regulatory compliance, the management of related-party arrangements or the informal practices that shape how the business operates daily.

Several specific risk areas are routinely underestimated. Delegation of authority is frequently unclear. The local director's actual signing authority, expenditure limits, contract approval thresholds and hiring autonomy may never have been formally defined beyond what appears in the entity's charter. Without a written delegation of authority matrix specifying who can commit the company to what level of financial obligation, decisions default to local management discretion and headquarters discovers problems only after commitments have been made.

Anti-corruption exposure deserves particular attention. Kazakhstan scored 38 points out of 100 on the 2025 Corruption Perceptions Index reported by Transparency International, a decline from 40 in 2024 — a reminder that progress is not linear. The global average score was 43, while in the Eastern Europe and Central Asia region the average was 35. Kazakhstan ranked 96th out of 180 countries. While this position reflects improvement over the longer term, the year-on-year decline underscores the gap between institutional reform and operating-level outcomes. Foreign-owned entities face dual exposure: local anti-corruption legislation and the extraterritorial reach of the UK Bribery Act, the US Foreign Corrupt Practices Act and similar frameworks in the investor's home jurisdiction. The OECD Anti-Corruption and Integrity Outlook 2026 makes this point directly: across OECD countries, the average gap between the strength of integrity regulations (63%) and implementation (44%) is 19 percentage points, compared to a 26 percentage-point gap in partner countries. For a foreign-owned business in Kazakhstan, this means that the existence of anti-corruption policies on paper provides limited comfort if the entity has not adapted its controls to local interaction patterns, procurement practices and authority-facing engagement.

The 2025 U.S. Investment Climate Statement on Kazakhstan provides further context. Amendments to the Entrepreneurial and Administrative Codes enacted in January 2025 prohibit government agencies from inspecting selected investors' activities and applying restrictive and prohibitive measures without the Prosecutor's approval. This is a positive development for investor protection. But despite institutional and legal reforms, corruption, excessive bureaucracy, arbitrary law enforcement and limited access to a skilled workforce in certain regions and sectors continue to present challenges. Regulatory compliance in Kazakhstan is evolving, and entities that have not been actively monitoring changes to tax, environmental and labour legislation risk accumulating exposure that surfaces in the form of audits, penalties or reputational damage.

The biggest governance risk is often invisible: the gap between formal compliance documentation and actual decision flow. A subsidiary may appear compliant while material risks are handled informally, conflicts of interest go unaddressed and the foreign investor receives reports that are technically accurate but not useful for governance decisions. The first 90 days after any ownership change, management transition or regulatory shift are decisive in determining whether the investor gains genuine control or merely inherits a reporting structure that obscures as much as it reveals.

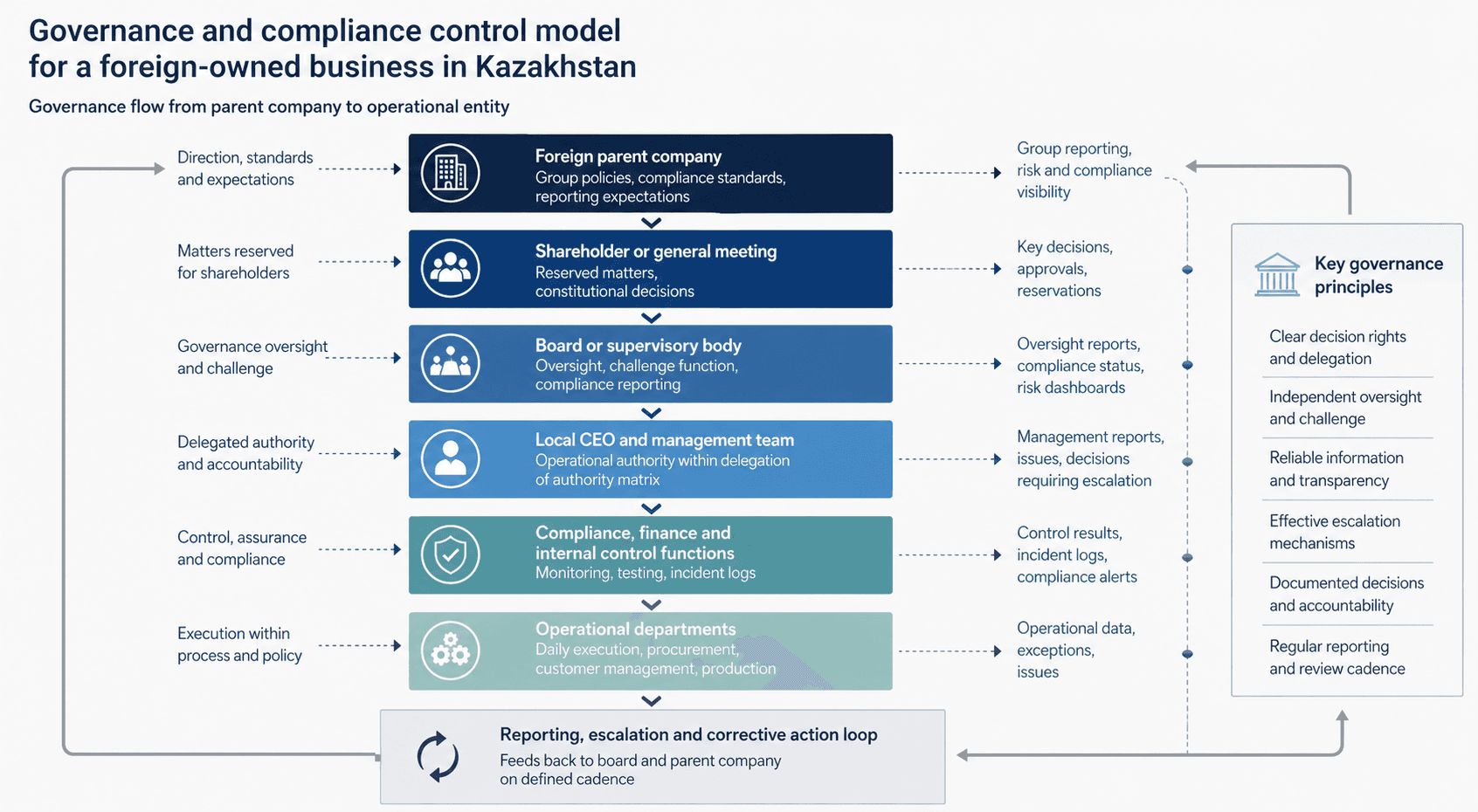

What an effective governance framework should include

Governance for foreign companies in Kazakhstan must connect the legal structure of the entity with practical oversight mechanisms that allow the parent company or board to understand, direct and control local operations. The Baker McKenzie guide to doing business in Kazakhstan presents an overview of the legal system and business regulations for companies operating in or considering investment into Kazakhstan, providing a comprehensive reference for the corporate, tax and regulatory framework. For governance purposes, the critical point is that legal structure alone does not produce compliance outcomes, and the compliance function must be operationally active, resourced to investigate and capable of escalating findings independently of local management.

The board or supervisory body is the starting point. Whether the entity has a formal board depends on its legal form, but even where a board is not legally required, establishing an oversight body with defined responsibilities strengthens both control and corporate memory. This body should hold reserved matters authority over capital expenditure above defined thresholds, related-party transactions, material contracts exceeding a specified value, senior appointments and dismissals, litigation decisions, regulatory responses, asset disposals and financing commitments. SOEs are present in at least 20 out of 30 sectors of Kazakhstan's economy and account for approximately 6.2% of national employment, and the governance practices expected of state-owned entities are increasingly benchmarked against international standards, which means that foreign-owned businesses operating in the same sectors face rising expectations as well.

Compliance advisory in Kazakhstan must address ownership of the compliance function. In many foreign-owned subsidiaries, compliance responsibility is fragmented across legal, finance and operations without a single point of accountability. An effective compliance structure assigns clear ownership for anti-corruption, tax, transfer pricing, labour law, environmental compliance and data protection. It includes practical controls: a gifts and hospitality register, third-party due diligence procedures, a public officials interaction log, conflict-of-interest declarations for management, procurement approval workflows that separate decision from payment and a whistleblowing channel accessible in local language. The OECD Integrity Review recommends that Kazakhstan strengthen its framework for "managing conflict of interest" and for "strengthening the framework for whistleblowing", which mirrors precisely what foreign-owned entities should be embedding at the company level.

Reporting discipline connects the local entity to the parent company's governance expectations. This means not only statutory financial reports but a structured board pack delivered monthly: management accounts, cash and working capital position, tax and compliance status, related-party transactions, legal disputes, regulatory correspondence, major contracts, exceptions to delegation of authority, incidents and whistleblowing reports and overdue corrective actions. The quality of reporting determines the quality of oversight. If headquarters receives only what local management chooses to share, governance is notional rather than effective.

Internal control and internal audit logic should follow the three lines model: management responsibility for daily controls, a risk and compliance function that monitors and challenges and an internal audit capability that provides independent assurance. The OECD notes that Kazakhstan can "strengthen its internal control system by clearly defining the roles of each stakeholder" and references the Institute of Internal Auditors' Three Lines Model as the applicable framework. For smaller foreign-owned entities where a full three-lines structure is disproportionate, the minimum requirement is clear separation between operational management and compliance oversight, with independent advisory involvement in governance-sensitive situations where the parent company needs an external perspective on risk.

Building compliance culture and headquarters visibility

Compliance culture cannot be copied from headquarters through a translated policy document and a mandatory training presentation. Effective compliance in a foreign-owned business requires adaptation to local context: understanding how procurement relationships work in practice, where anti-corruption risk concentrates in authority-facing interactions, how labour law constraints affect restructuring decisions and where environmental compliance obligations create reporting requirements that may differ from what the parent company expects.

For companies in energy, infrastructure, logistics, financial services or regulated manufacturing, corporate governance in Kazakhstan must also cover sector-specific authority-facing interactions, licensing, permits, procurement processes and local content expectations. There are approximately 7,000 quasi-government entities in Kazakhstan, and the boundary between public and private sector activity is not always clearly delineated. Foreign-owned businesses that interact with state entities through supply contracts, regulatory approvals or joint ventures need governance mechanisms that track and document these interactions systematically.

The challenge extends to information flow. Many foreign investors discover governance problems not through their reporting systems but through external triggers: a tax audit, a customer complaint, an employee dispute or a media inquiry. By the time these signals reach headquarters, the exposure has already accumulated. Building reliable information channels requires multiple inputs: management reports, compliance incident logs, whistleblowing mechanisms, periodic site reviews and independent board or advisor input that reduces blind spots. Finding qualified independent oversight capability in Kazakhstan remains a practical constraint, and the pool of experienced independent directors with both international governance standards and deep local knowledge is limited.

For foreign-owned companies where the parent or board needs board advisory and governance support for complex business situations, the question is whether the current governance structure provides genuine oversight or merely formal documentation. Tretiakov Consulting works with foreign-owned businesses where the investor requires strengthened governance architecture, compliance redesign and independent perspective on risk, not as a separate legal overlay but as an integrated part of how the entity is managed and controlled.

Practical governance and compliance framework for foreign-owned businesses

The following framework outlines the governance and compliance architecture that foreign-owned entities in Kazakhstan should establish. Each area requires both structural definition and ongoing management attention to function as a working system rather than a documentation exercise.

Governance area | What must be defined | Why it matters in Kazakhstan |

|---|---|---|

Board and supervisory oversight | Role of the board, reserved matters, reporting duties and challenge function | Formal ownership does not automatically create effective oversight over local decisions |

Delegation of authority | Approval thresholds, decision rights, signing authority and escalation rules | Local management needs operational autonomy but headquarters needs visibility and control over material commitments |

Compliance ownership | Responsibility for anti-corruption, tax, transfer pricing, labour, environmental and sector-specific regulatory compliance | Compliance fails when responsibility is fragmented across legal, finance and operations without clear accountability |

Reporting discipline | Monthly management accounts, operational dashboards, compliance reports, board materials and incident logs | Headquarters needs decision-quality information not only statutory reporting |

Internal control and audit | Internal audit logic, control testing, incident tracking and corrective actions with defined timelines | Weak controls allow informal practices to continue until they become regulatory or reputational issues |

Parent-company interface | Alignment between Kazakh entity governance, group-level policies and international regulatory obligations | Foreign investors need local governance that satisfies both Kazakhstan requirements and international standards including FCPA, UK Bribery Act and IFRS |

Conclusion

Foreign investors managing governance and compliance for foreign-owned businesses in Kazakhstan should look beyond formal legal structure and policy documentation. The practical question is whether the local entity produces reliable information, escalates risk early, follows clear decision rules and allows the parent company or board to intervene before compliance, tax, labour or reputational issues become expensive. Regulatory compliance in Kazakhstan is a moving target as the legislative framework continues to modernise, environmental rules tighten and anti-corruption enforcement develops in line with OECD recommendations. Entities that treat compliance as a static document rather than an active management function accumulate exposure that can be difficult and costly to reverse. Governance is not an overhead for a foreign-owned business. It is the mechanism through which the foreign investor protects the value, reputation and long-term viability of its local operation.

If your foreign-owned business in Kazakhstan requires stronger governance architecture, compliance oversight or independent board support, explore our approach to board advisory and governance support or begin a focused discussion about governance and compliance control.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.