Go-to-Market Strategy Consulting in Belgium for B2B Mid-Market Companies

Most foreign commercial plans for Belgium come undone at the same point, which is the assumption that a single plan can serve a single country. A mid-market industrial supplier or a B2B brand signs off a national launch built on one channel structure, one price list, one sales team and one set of marketing assets, and then watches it stall within two or three quarters as pipeline accumulates on one side of the country and refuses to form on the other. A distributor that performs in Flanders shows little traction in Wallonia, the accounts in Brussels behave like neither, and revenue settles well below the figure that underwrote the investment, usually without any single line in the management accounts explaining the gap. The shortfall is seldom a demand problem and rarely a product problem; it is the predictable cost of treating a structurally fragmented market as a homogeneous one, and it is precisely the problem that go-to-market strategy consulting in Belgium exists to solve, which is seldom the problem that foreign boards believe they are buying.

Belgium is not a smaller version of France or the Netherlands, and it does not reward a translated copy of a plan that worked elsewhere. It is a federal, multilingual market in which commercial behaviour, channel structure, regulation and the language of the buyer divide along regional lines, and in which a substantial share of demand moves quietly across the border before any domestic competitor is considered. The companies that perform best tend to treat the country as a problem of channel architecture and sequencing rather than as an exercise in localisation. What follows sets out the operating mechanics behind that distinction, what the available data actually supports, and what a defensible commercial strategy has to account for before the first sales hire is made.

One country, three commercial markets

The first thing any go-to-market strategy has to absorb is that Belgium's federal structure is not administrative detail but the operating logic of the commercial market. The Dutch-speaking Flanders region in the north, the French-speaking Wallonia region in the south and the bilingual Brussels-Capital Region function as three distinct demand environments, with different languages, different media, different distribution density and materially different economic conditions. The labour market makes the point most clearly. According to the US State Department's 2024 Investment Climate Statement, regional unemployment in 2023 stood at around 3.5 per cent in Flanders against 8.3 per cent in Wallonia and close to 10 per cent in Brussels. A country with that internal spread does not present one buyer, one cost base or one route to the customer, and a plan that assumes it does is mispriced from the outset.

The same divide runs through where commercial activity actually concentrates. The US Department of Commerce Country Commercial Guide reports that of the country's record 63,867 online stores in 2024, roughly 72 per cent sit in Flanders, 19 per cent in Wallonia and 9 per cent in Brussels. Foreign investment shows the same gravity. EY's Belgian Attractiveness Survey for 2025 recorded 210 FDI projects in 2024, of which approximately 137 landed in Flanders against 44 in Brussels and 29 in Wallonia. The commercial centre of gravity is therefore unambiguous, yet a route-to-market strategy in Belgium that serves only that centre forfeits roughly a third of the country together with most of its public-sector and institutional demand. The recurring error is the conflation of national market activity with executable reality inside each region, and that distinction is the one a serious commercial strategy for foreign-owned companies has to hold from the beginning.

What the investment numbers say, and what they conceal

The macro case for Belgium is genuinely strong, which is precisely why it can mislead. IMF figures cited in the Country Commercial Guide put Belgian GDP at approximately 664.6 billion US dollars in 2024 with real growth of around 1 per cent, a modest but stable economy with high and relatively evenly distributed purchasing power. UNCTAD's World Investment Report 2024 records Belgium among the world's larger recipients of foreign direct investment, with an inward FDI stock of roughly 577.9 billion US dollars, while the EY survey places the country eighth in Europe for the number of investment projects. Manufacturing and logistics drove investment in 2024, with 55 and 53 projects respectively, which reflects Belgium's role as a continental distribution gateway rather than only an end market.

At face value those figures argue for speed, but read with an operator's eye they argue for a far more sceptical investment thesis. Belgium's headline FDI position is shaped in part by its role as a holding-company and intra-group financing location, so a large share of the recorded stock reflects financial structuring rather than the kind of operating investment a mid-market entrant could contest, and it says very little about whether such an entrant can win customers on the ground. The country's business dynamism is also weaker than the investment narrative suggests. Eurostat's business demography data put Belgium's share of high-growth enterprises at 5.4 per cent in 2023, among the lowest in the entire European Union. A market can attract substantial capital and still be structurally difficult to grow inside, and the line between an attractive destination and an investable commercial opportunity is the one that honest growth strategy consulting has to draw before any capital is committed.

The trend that matters most for a B2B or consumer entrant is cross-border leakage, and on this measure Belgium is among the most internationally porous consumer markets in Europe. The Commercial Guide, citing Cross-Border Commerce Europe, reports cross-border sales of around 5.5 billion euros, close to 35 per cent of total e-commerce volume, with more than half of Belgian online shoppers buying from foreign sites in a typical year. The cause is structural rather than promotional, because Dutch-speaking Belgians gravitate towards Dutch-language platforms that are often based in the Netherlands, while French-speaking Belgians gravitate towards French-language platforms that are often based in France. The same language line that divides the country internally routes a predictable slice of demand outward, which means a national-average market-size model can overstate the addressable opportunity for a foreign brand, particularly in categories where language, channel and cross-border buying behaviour weigh heavily on the purchase.

The cost base that disciplines every commercial strategy in Belgium

Belgium's cost base does not permit a relaxed commercial model, and understanding why is more useful than knowing that it is expensive. Eurostat's labour-cost data for 2024 put the average hourly labour cost in Belgium at 48.2 euros, the third highest in the European Union after Luxembourg and Denmark and well above the EU average of 33.5 euros. The structural drivers compound the headline, because Belgium also recorded the highest tax wedge on low-wage labour in the Union in 2024, at 45.8 per cent according to Eurostat, and its long-standing system of automatic wage indexation links pay to inflation. The OECD's Economic Outlook of late 2025 was explicit that past wage increases have eroded Belgium's price competitiveness and left the economy more exposed to any trade slowdown. These pressures are better read as a direction of travel than as a fixed level, because the OECD's Economic Survey of Belgium records that labour productivity, although still among the highest in the OECD, slowed markedly through the past decade before firming again from 2021, which means the productivity advantage that historically offset high Belgian wages has proved considerably less dependable than the country's prosperity implies. For a commercial entrant the practical reading is that the margin between price and cost is narrower than the headline wealth of the market suggests, and that it cannot be assumed to widen of its own accord.

The commercial consequence follows directly and is regularly underestimated. A high and indexation-driven cost base means that a direct, headcount-heavy sales model carries fixed costs that a low-margin or slow-ramp plan cannot absorb, which pushes serious entrants towards leaner channel-led or hybrid structures and raises the required level of commercial productivity from the first month. This is where commercial excellence stops being a slogan and becomes an economic requirement, because where the average hourly labour cost is around 48 euros the gap between a sales organisation that converts at benchmark efficiency and one that does not is the difference between a viable entry and a loss-making one. Sales channel optimisation in Belgium is therefore not a refinement applied after launch but a precondition of the business case. The same logic governs revenue transformation for companies that already operate in the country but underperform, because many foreign-owned subsidiaries are not failing on product or price; they are carrying a commercial cost structure designed for a larger and cheaper market and applied to a small, expensive and fragmented one. Repairing that is closer to operational redesign than to marketing, and it is the substance of genuine revenue transformation for B2B companies here.

Distribution and route-to-market: where the channel splits

If the cost base sets the constraint, the channel sets the architecture, and a distribution strategy for foreign brands in Belgium has to begin from the fact that no single national channel performs uniformly. The regional and linguistic divide that fragments demand also fragments supply, because distributors, buying groups, retail banners and B2B intermediaries tend to be regionally rooted, with strength on one side of the language line and limited reach on the other. A single distributor appointed for the whole country is, in practice, often strongest in one region while offering far thinner coverage elsewhere, and that weakness tends to surface only when the second year's numbers arrive.

For consumer and retail entrants, a credible retail market strategy in Belgium has to contend with a concentrated grocery and specialty landscape, intense cross-border price comparison and consumers who treat foreign-language platforms in neighbouring countries as part of their normal consideration set. Retail strategy consulting in Belgium that overlooks this porousness tends to over-index on domestic shelf presence and to under-price the true competitive reference point, which is frequently a Dutch or French seller offering the same item in the shopper's own language. For industrial and B2B players the route-to-market strategy for industrial companies in Belgium turns on the gateway logic visible in the investment data, because the country's value lies substantially in its function as a continental distribution and logistics hub anchored by Antwerp-Bruges. Many industrial commercial models in Belgium are in reality regional or pan-European models with a Belgian node rather than standalone country plays, and designing the channel without that distinction produces a sales structure that is over-built for domestic demand and under-built for the cross-border flows that actually justify a Belgian presence.

The table below sets out how the headline reading of the market diverges from the operating reality across the dimensions that decide a commercial plan.

Dimension | The headline reading | The executable commercial reality |

|---|---|---|

Market unit | One national market of about 11.8 million people | Three regional markets across Dutch-speaking Flanders, French-speaking Wallonia and bilingual Brussels |

Demand size | National GDP and consumer wealth imply a large addressable base | Around 35 per cent of e-commerce demand leaks across the border, so national models overstate the reachable market |

Channel | A single Belgian distributor covers the country | Distributors and retail banners are regionally rooted, so a single national appointment often delivers strong coverage in only one region |

Cost base | A wealthy and productive European economy | Hourly labour cost of 48.2 euros, third highest in the EU, kept rising by indexation |

Growth | Strong investment inflows signal an easy market to grow in | A high-growth-firm share of 5.4 per cent, among the lowest in the EU |

Investment signal | High FDI stock indicates a strong opportunity | Much of the stock is holding-company and intra-group flow rather than operating demand |

Sources: Eurostat (hourly labour costs and business demography); UNCTAD World Investment Report 2024; EY Belgian Attractiveness Survey 2025; US Department of Commerce Country Commercial Guide.

From go-to-market to revenue: designing an executable model

It is worth being precise about terms, because the failures usually begin with a category error. A go-to-market strategy is the decision architecture for how a company reaches, wins and keeps customers in a defined market, covering segmentation, value proposition, channel, pricing, coverage and the sequence in which they are deployed, and it is not interchangeable with a marketing strategy. Marketing strategy sits inside the go-to-market design and governs demand generation and positioning, while the go-to-market layer governs the harder commercial questions of who sells, through which channel, at what cost and in what order. The common confusion between a go-to-market strategy and a marketing strategy is what produces well-translated campaigns sitting on top of a broken channel, and it is the most expensive misunderstanding in foreign-entry planning.

A workable go-to-market strategy framework for Belgium answers four questions in a fixed order, and the order is itself the discipline. The first is segmentation by region and language as well as by industry, because a Belgian segment is never simply a vertical. The second is channel architecture for each region, because the answer in Flanders is rarely the answer in Wallonia. The third is commercial economics, stress-tested against the cost base described above, which decides between direct, indirect and hybrid coverage. The fourth is sequencing, meaning which region, channel and segment to enter first and what evidence should trigger the next move. Most generic growth strategy examples invert that order by moving straight to hiring or to appointing a distributor, which locks in the cost before the structure has been proven. Building a go-to-market strategy properly means resisting that instinct.

This is also where commercial excellence and sales transformation do their real work. Commercial excellence is the systematic management of the commercial engine, covering pricing governance, sales productivity, channel performance and account management, so that revenue is the product of structure rather than of individual effort. In a fragmented and high-cost market it is the mechanism that keeps the economics intact as the business scales across regions. Sales transformation in Belgium typically follows once a subsidiary has grown organically into a structure that no longer fits the market, whether through being too direct, too centralised or too dependent on a handful of relationships. Rebuilding that structure is a B2B growth strategy in the precise sense, because growth then comes from the model rather than from heroics, and it is the difference between a business expansion strategy in Belgium that compounds and one that merely consumes budget.

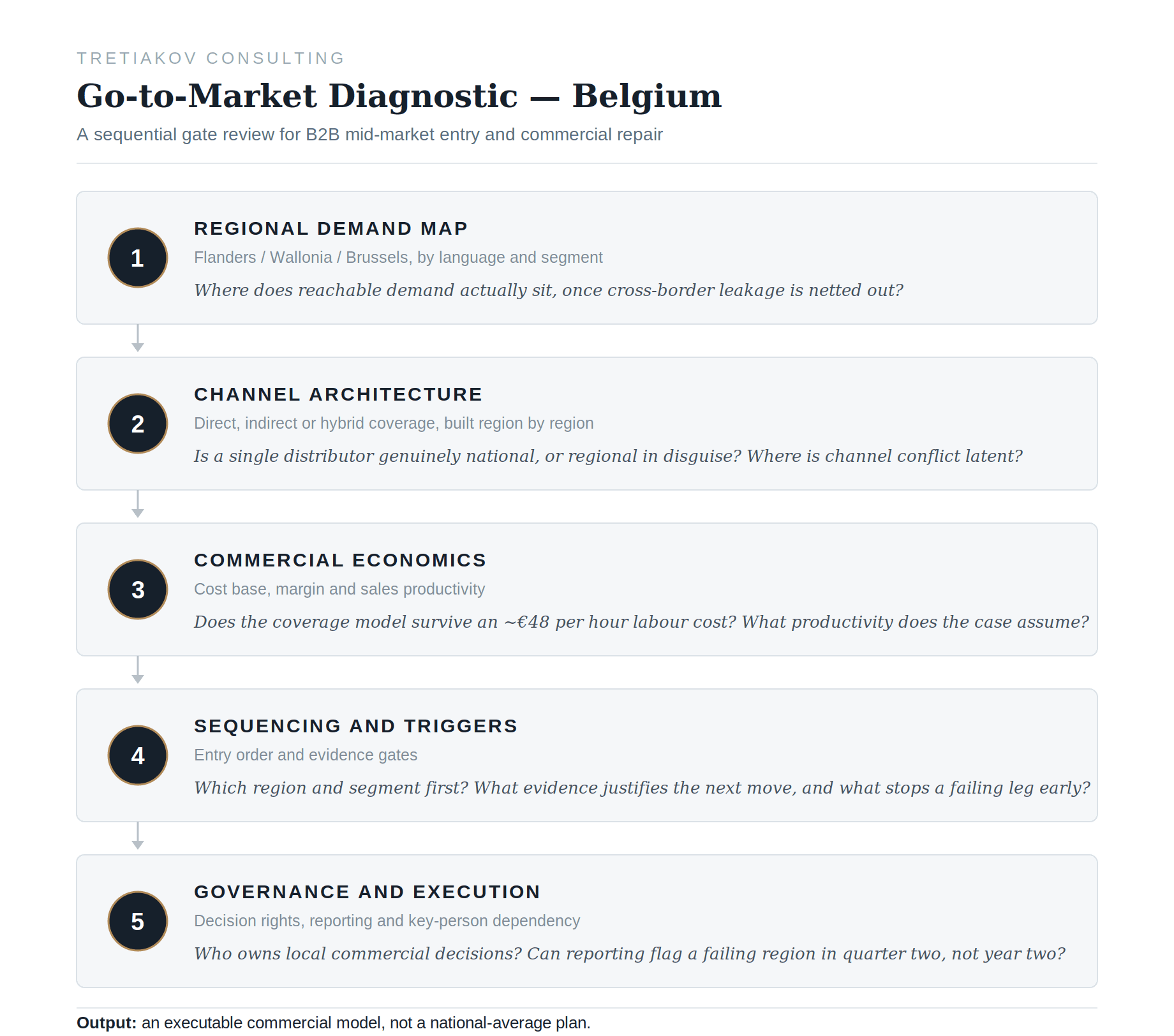

A diagnostic framework for go-to-market strategy consulting in Belgium

The framework below is the assessment logic we apply before recommending any commercial structure. It is deliberately sequential, so that each stage acts as a gate and a weakness at an earlier stage invalidates the work done later. The purpose of go-to-market strategy consulting in Belgium is to expose the failure points in this sequence before capital is committed to them rather than after.

Running the diagnostic in this order exposes the two errors that destroy most plans early. The first is a channel decision taken before the demand map exists, where a distributor is appointed because one is available rather than because the regional analysis demanded it. The second is a commercial economics assumption that is never written down, namely the sales productivity required to make a direct model pay at Belgian cost levels, which is usually heroic once it is surfaced. A go-to-market strategy for foreign companies in Belgium that clears all five gates is uncommon, and it is uncommon precisely because the market penalises the shortcuts the framework forces into the open.

Where mid-market commercial strategies fail

Commercial transformation for mid-market companies in Belgium tends to fail in a small number of recognisable ways, and the causes are structural rather than tactical. The first is the national-channel illusion already described, where a single distributor or sales team is treated as national coverage when it is in practice regional, a weakness that becomes visible only when the second-year numbers fall short. The second is cost-base denial, where a coverage model imported from a larger or cheaper market is never re-costed against Belgian labour economics, so the business runs at a structural loss that is blamed on demand rather than on design. Owners and boards working through these questions will find the operating mechanics set out in more detail in our analysis of commercial growth for Belgian SMEs, which addresses the same productivity problem from the perspective of established local businesses.

The third pattern is under-investment in language and content, where assets are localised into Dutch and French as a translation task rather than as a channel requirement, which reads as foreign to buyers who can easily choose a seller that speaks to them natively. The fourth and most damaging is governance and execution failure. Foreign-owned subsidiaries frequently concentrate commercial knowledge in one or two long-tenured individuals who hold the distributor relationships, the pricing logic and the key accounts, which is acute key-person dependency and remains invisible on a healthy revenue line until the person leaves. The same fragility is common in family-controlled businesses, and the mechanisms are examined in our note on governance challenges in Belgian family businesses. Weak local decision rights compound the problem, because when commercial decisions for a fragmented market are taken centrally and slowly, a company cannot respond to an underperforming region until the annual review, by which point a year of pipeline has been lost. None of these are marketing problems and no campaign resolves them, which is why commercial transformation in Belgium so often has to begin with the operating model of the commercial function, a sequence we set out in our work on business transformation in the Belgian mid-market. For industrial entrants weighing the gateway logic against domestic demand, the trade-offs are developed further in our industrial investment advisory for Wallonia and Flanders.

The strategic read for boards entering Belgium

For a foreign B2B mid-market company the decision is not whether Belgium is attractive, because on purchasing power, logistics and continental access it plainly is. The decision is whether the commercial model on the table has been built for one market or for three, for a labour cost of 33 euros an hour or for the 48 the market actually charges, and for domestic demand or for the cross-border flows that genuinely justify a Belgian presence. A growth strategy for companies entering Belgium that gets those three judgements right produces a high-quality and defensible position and a credible springboard into the wider region, while one that gets them wrong turns the country into a slow and expensive lesson in the difference between market activity and executable revenue.

That distinction is the entire purpose of go-to-market strategy consulting in Belgium, which is to design the commercial model against the market that exists rather than the one described in the investment brochure, and to find the failure points in the regional demand map, the channel architecture and the commercial economics before they are funded. The companies that do this do not grow faster because they spend more. They grow because their structure matches the market, which in Belgium is the only commercial strategy that survives contact with the second-year numbers.

For companies still at the entry stage, our market entry and business expansion service sequences the regional demand, channel and operating-economics questions before the first commitment is made. If you are repairing an underperforming Belgian operation, our commercial transformation and strategic growth practice rebuilds the route-to-market, channel structure and commercial economics for the market as it actually operates. You can speak to us directly about your Belgian entry or commercial turnaround.

Frequently asked questions

What is a go-to-market strategy, and how does it differ from a marketing strategy? A go-to-market strategy is the full commercial design for reaching and converting customers in a defined market, covering segmentation, channel, pricing, coverage model and the sequence in which they are deployed. A marketing strategy sits inside it and governs positioning and demand generation. The practical reason the distinction matters in Belgium is that a strong marketing strategy applied through the wrong channel structure will still fail, because the market punishes channel error more severely than messaging error. Boards that treat the two as interchangeable tend to fund campaigns long before the channel question has been answered.

How should a foreign company build a go-to-market strategy for Belgium? The sequence matters more than any single decision. A company should first map reachable demand by region and language, net of the cross-border leakage that removes a meaningful share of nominal demand, then design channel architecture region by region, then test the commercial economics against a labour cost among the highest in the European Union, and only then sequence its entry and set the evidence that will trigger each subsequent move. The frequent mistake is to begin with hiring or with a single national distributor, which fixes the cost base before the structure has been validated.

What is commercial excellence, and why does it carry more weight in Belgium? Commercial excellence is the disciplined management of the commercial engine, including pricing governance, sales productivity, channel performance and account management, so that revenue is produced by structure rather than by individual effort. It carries more weight in Belgium because the cost base leaves no room for inefficiency. When the marginal sales hour is expensive and indexation keeps raising it, the gap between benchmark and below-benchmark productivity decides whether the operation is profitable at all.

What is route-to-market, and why is it harder in Belgium than in neighbouring markets? Route-to-market is the path a product takes from the company to the end customer, including the intermediaries, channels and logistics involved. It is harder in Belgium because the country is effectively three regional markets with regionally rooted intermediaries, so a single route rarely achieves national reach. A distributor that dominates Flanders may be almost absent in Wallonia, which means an entrant frequently needs more than one route to cover a market that looks, on paper, small enough to serve with one.

When does a Belgian subsidiary need revenue or sales transformation rather than simply more sales effort? The signal is structural rather than seasonal. When a subsidiary is growing slowly or losing money despite a competitive product, the cause is usually a commercial model designed for a different market, whether through excessive direct coverage, central decision-making that cannot react to regional shifts, or concentration of relationships in a few individuals. In those cases more sales effort raises cost without changing the economics, and the remedy is a revenue transformation that rebuilds coverage, channel mix and pricing discipline so that the unit economics work at Belgian cost levels.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.