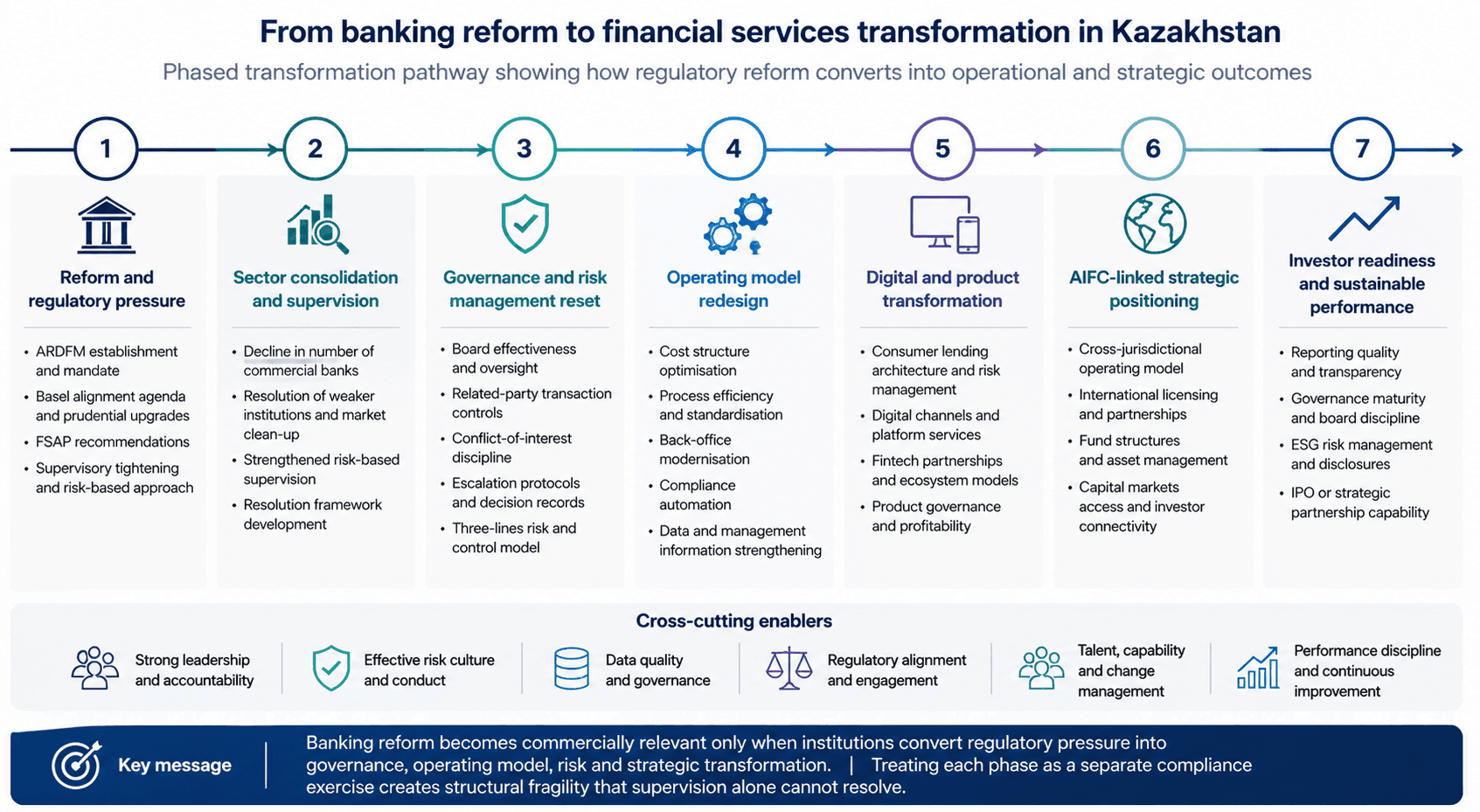

Banking Reform in Kazakhstan and Financial Services Transformation

The financial sector in Kazakhstan looks more disciplined and better supervised than it did a decade ago. The number of commercial banks has fallen from 28 to 21 through mergers and liquidations of weaker institutions. Regulatory authority has been concentrated under the ARDFM. Capital adequacy and asset quality metrics have improved. But none of this answers the question that matters most to financial services executives, boards and investors: whether individual banks and financial institutions are actually prepared for what comes next. Banking reform in Kazakhstan has moved the sector past the crisis and consolidation phase, yet the next challenge is more operational than regulatory. It is a question of whether institutions can translate tighter supervision, digital competition, governance expectations and shifting customer economics into a functioning transformation agenda that connects compliance with commercial performance.

Why banking reform in Kazakhstan matters beyond regulation

The Kazakhstani financial system has undergone significant changes in recent years, driven largely by digitalization, with financial assets shifting towards consumer loans and mortgages. Dollarization has declined but remains relatively high on the funding side. The state's footprint in the financial sector has grown considerably along with market concentration. Several bank defaults occurred, often addressed through government bailouts. Since 2020 a new supervisory authority with resolution powers, the ARDFM, has been in place, while in 2018 the Astana International Financial Centre was launched with a separate legal and regulatory framework.

The financial system remains bank dominated, with assets representing slightly more than 60 percent of GDP. Kazakhstan had 21 commercial banks as of January 2025. The five largest held assets of approximately $79.4 billion, accounting for 67.5 percent of total banking sector assets. The largest three banks account for about 53 percent of banking sector assets, with concentration particularly high in some markets such as mortgages and consumer loans.

This concentration creates a structural dynamic that goes well beyond regulatory compliance. When a small number of institutions hold the overwhelming majority of sector assets, every governance weakness, every unresolved risk management gap and every deferred operating model decision carries amplified systemic weight. In 2019 the responsibility to supervise the financial sector was assigned to the newly established ARDFM. While ARDFM has introduced a risk-based approach and Supervisory Examination and Review Process, asset quality and related-party transactions remain a source of concern, even if improving. Its present approach does not yet comply with international standards for consolidated supervision and it should continue with its plans to align key prudential standards with the Basel framework.

For financial services executives these findings are not abstract regulatory observations. They are direct signals about the quality of internal risk architecture, the reliability of management information and the readiness of governance structures to absorb the next wave of supervisory expectations. How Kazakhstan is transforming its banking sector is no longer a story about closing weak banks. It is a question of whether surviving institutions can build the internal infrastructure that reform demands.

Where financial institutions misread the transformation challenge

The most common mistake among banks operating in Kazakhstan is treating reform as something that has already happened. Consolidation reduced the number of players. Supervision was strengthened. Capital ratios improved. From a distance the sector appears stable. The reality beneath this surface is more complicated.

The banking sector remains resilient amid continued rapid consumer credit growth. The IMF has noted that the banking sector remains sound but flagged risks related in particular to rapid consumer credit growth. It encouraged continuing to implement key 2023 FSAP recommendations and urged priority for enacting the new Banking Law, establishing the capacity to operationalize the new bank resolution framework and regulating activities in the digital asset space. Ensuring prudential measures are well targeted will help mitigate potential financial stability risks from household over-indebtedness.

Consumer lending has grown significantly in Kazakhstan, more than doubling between 2019 and 2023. While in 2014 the ratio of corporate loans to consumer loans was 2:1, that had completely reversed by mid-2023 with consumer loans accounting for about two thirds of total commercial lending. This reversal is not merely a product mix shift. It changes the risk profile, the cost structure, the compliance burden and the operating model requirements of every institution that participates in consumer finance. A bank that appears digitally advanced while its back-office processing, control architecture and risk reporting remain fragmented is not transforming. It is adding commercial complexity on top of operational weakness.

In all banks that were liquidated in recent years, de facto exposure to related parties was significantly above what was officially reported and was the main source of non-performing loans and reason for liquidation. The ARDFM should perform more intrusive oversight of related-party transactions including onsite reviews, and the authorities should take more stringent corrective measures against gaps in banks' related-party framework and practices.

This finding from the IMF and World Bank FSAP assessment is among the most important for anyone evaluating banking transformation in Kazakhstan. It means that governance failure, not market conditions, was the primary driver of bank failures. Institutions that have not embedded genuine board challenge, independent risk oversight, escalation protocols and conflict-of-interest controls into their operating rhythm remain exposed regardless of how strong their capital ratios appear. This is precisely where board advisory and governance support for financial institutions becomes not a compliance layer but a survival mechanism.

The AIFC dimension in Kazakhstan's financial services sector

The Astana International Financial Centre was launched in 2018 with the objective of establishing a leading international centre for financial services in Astana, attracting foreign investment and supporting the growth and development of Kazakhstan and the region. Drawing from a model adopted in the Gulf region, the AIFC was established as a distinct and separate jurisdiction operating under its own legal structure, governance arrangements and regulatory framework based on the common law framework applied in England and Wales. The AIFC has established its own dedicated Court, Arbitration Centre and regulatory authority. Introduction of a legal and regulatory approach familiar to international financiers aims to attract foreign intermediaries and capital to the Centre.

The AIFC positions itself as the leading financial centre in Central Asia and Eastern Europe, offering businesses investment opportunities, innovative solutions and international regulatory standards. As of 2024 the AIFC has attracted more than $16.9 billion to the Kazakh economy. The scope covers banking, asset management, capital markets, insurance, Islamic finance and fintech.

For international financial companies evaluating AIFC in Kazakhstan as an entry route, the legal framework is attractive but insufficient as a standalone strategy. There are multiple interconnections between the AIFC and the domestic financial system that may impact financial stability. Policy challenges arise when financial services may be provided under distinct legal and regulatory arrangements from both a domestic jurisdiction and a jurisdictionally separated international financial centre. The IMF technical note on AIFC and the Kazakhstan financial system specifically recommends development of a Financial Stability Protocol to ensure effective cooperation between ARDFM, NBK and AFSA.

Financial services advisory in Kazakhstan that addresses AIFC opportunities must therefore go beyond licensing mechanics. The practical questions are about product positioning, operating model for cross-jurisdictional activity, governance alignment between AIFC and domestic operations, regulatory reporting obligations and the commercial logic for choosing AIFC as a platform rather than simply as a registration address. For international financial companies, market entry and business expansion support should include a clear assessment of whether the AIFC framework delivers operational advantage or creates governance complexity that the entrant has not planned for.

Advisory opportunities in banking transformation and governance

The cumulative effect of sector consolidation, supervisory strengthening, consumer lending growth, digital competition and AIFC development creates a dense transformation agenda for financial institutions. Banking operational transformation in Kazakhstan cannot be limited to front-end digitalization. It must reach into process architecture, cost-to-income management, risk reporting, product governance, compliance infrastructure and the operating connection between technology investment and control effectiveness.

The ARDFM developed regulatory recommendations on the disclosure of information about the degree of exposure to ESG-related risks, as well as the procedure for identifying, assessing and managing such risks in accordance with international standards. This introduces a new layer of reporting and governance expectation. The AIIB-supported Fiscal Governance and Financial Sector Reforms Program confirmed that the programme supports reforms in areas of fiscal sustainability, transparency and governance as well as banking and capital market development.

Governance advisory for financial institutions in Kazakhstan addresses a fundamental gap: the distance between what supervisors now expect and what most institutions actually deliver in terms of board effectiveness, committee discipline, escalation protocols, independent challenge and decision documentation. The ratio of non-performing loans overdue by more than 90 days fell from 8.6 percent in April 2019 to 3.1 percent by January 2025. This improvement is real. But asset quality metrics alone do not reveal whether the institution has the management information systems, risk culture and governance architecture to sustain that performance through a credit cycle downturn or a shift in macroprudential policy.

Operating model transformation for banks in Kazakhstan requires connecting several workstreams that are typically managed in isolation: cost structure and process efficiency, digital migration beyond the customer interface, compliance automation, risk management integration and product economics. For institutions considering international investment, strategic partnership or IPO readiness, the additional requirement is that governance, reporting quality and operating discipline must withstand external scrutiny. Tretiakov Consulting works with financial institutions and investors where reform pressure, operating model strain, governance gaps and strategic repositioning require business transformation and operating model redesign support that produces practical change rather than documentation.

Practical advisory framework for financial services transformation in Kazakhstan

The following framework outlines the advisory architecture that financial institutions in Kazakhstan should consider when converting reform and regulatory pressure into a structured transformation response.

Advisory area | What must be assessed | Why it matters in Kazakhstan |

|---|---|---|

Banking operating model | Process efficiency, branch model, digital migration, back-office structure and cost base | Reform pressure creates a need for institutions that are not only compliant but operationally efficient |

Risk and compliance architecture | Credit risk, consumer lending exposure, AML/CFT, regulatory reporting and control functions | Stronger supervision requires better internal discipline and more reliable management information |

Governance and board oversight | Board effectiveness, committee structure, escalation, independent challenge and decision records | Financial institutions need governance that can actively manage reform, transformation and investor expectations |

AIFC strategy | Licensing logic, product positioning, legal structure, partnerships and operating connection with Kazakhstan | AIFC can support international activity but only when linked to a clear business and execution model |

Digital and product transformation | Customer channels, fintech partnerships, product economics, platform models and technology dependencies | Digital growth can increase complexity if product governance and control architecture do not keep pace |

Investor and IPO readiness | Reporting quality, governance maturity, strategy narrative, risk controls and operating discipline | International capital requires transparency, credible governance and performance that can withstand scrutiny |

Conclusion

Financial institutions and investors assessing banking reform in Kazakhstan should not approach it as a completed regulatory chapter. The sector has stabilised, supervision has strengthened and the weakest institutions have been removed. But the practical question remains: whether each institution can convert reform pressure into stronger governance, better risk management, a more efficient operating model and a clearer strategic position in a financial services market that is growing more demanding with each regulatory cycle. The advisory opportunities in Kazakhstan's financial services sector are significant for those who understand that financial services and banking reform in Kazakhstan is not about compliance alone. It is about building institutions capable of sustained performance under conditions that will only become more rigorous.

If your institution or investment mandate requires structured advisory support across banking transformation, governance and operating model change, explore our financial services and banking advisory for regulated institutions or begin a focused discussion about a financial services or banking mandate.

Related Insights

Explore the latest from Source® — product updates, thought pieces, and ideas driving the future of intelligent systems.